Introduction

Cross-border investment into European real estate surpassed €270 billion in 2024 — and 2025 is tracking higher. For American investors, the timing is notable: the dollar has held strength against the euro, ECB rate cuts are lowering financing costs, and structural housing undersupply in key cities is compressing available inventory.

Europe's markets don't move together, though. Some cities are still working through post-2022 price corrections; others have already hit new highs. Rental yields reflect that divergence — roughly 3% in prime Western capitals, climbing past 8% in select Central and Eastern European markets.

Knowing which cities sit in which category — and why — is where the real decision-making starts. This guide breaks down the top European markets by rental yield, price trajectory, liquidity, and foreign buyer accessibility.

Key Takeaways

- Lisbon tops the list for American investors: strong YoY price appreciation, lifestyle appeal, and Portugal's established Golden Visa framework

- Warsaw and Riga lead on gross rental yields (8%+) — the right markets if income generation drives your strategy

- Madrid's deep liquidity and GDP growth above the Euro area average make it the lowest-volatility pick in this group

- Bucharest's upside is real but early-stage — Romania's 2024 Schengen entry is shifting institutional attention toward the market

- Headline yields don't tell the whole story; legal structure, tax treaties, and exit liquidity determine actual returns

Why European Real Estate Is Attracting Global Capital in 2025

The European residential real estate market represents massive scale and durable structural momentum. According to Mordor Intelligence, the market is supported through 2030 by fundamental supply-demand imbalances across urban centers.

Three macro tailwinds are driving 2025 investment activity:

- ECB rate cuts are easing borrowing costs and restoring transaction volume after the 2022-2023 slowdown

- Chronic undersupply in Southern and Central European cities is driving persistent rent and price pressure, with decades of underbuilding compounded by accelerating urbanization

- Rising rental demand from cross-border migration, urbanization, and digital nomad activity is keeping vacancy rates low — and this demand is structural, not cyclical

The 2022-2023 price correction in Germany, Sweden, and Austria has created reset entry points in previously expensive markets. Meanwhile, Portugal, Spain, and Poland never corrected and are now posting multi-year highs. This divergence is central to city selection in 2025.

Best European Cities for Real Estate Investment in 2025

Cities were evaluated on five criteria: rental yield, YoY price growth, legal accessibility for foreign buyers, market liquidity, and structural demand drivers.

Lisbon, Portugal

Lisbon recovered from a near-20% price decline between 2010–2013 to nearly triple in value since its trough — a trajectory few European capitals can match. Demand is driven by digital nomads, retirees, tech sector migration, and short-term rental tourism.

For American investors, three structural advantages stand out:

- Portugal's tax environment has historically favored foreign residents

- Foreign ownership is legally straightforward with no purchasing restrictions

- Exit liquidity is verifiable through both sale and rental channels

Alori International Holdings works with investors entering Lisbon through off-market inventory and guided transaction support — particularly relevant given the city's competitive prime neighborhoods.

| Metric | Figure | Source Context |

|---|---|---|

| Entry Price Range | €4,000–€5,500/sqm (city average) | Premium neighborhoods like Chiado and Alfama command higher rates; emerging areas offer better value |

| Gross Rental Yield | 5–6% (long-term), 8–10% (short-term) | Short-term rentals in tourist-heavy districts significantly outperform traditional leases |

| YoY Price Growth | ~17% (Q1 2025) | Among the highest in the EU, per Eurostat data |

At ~17% YoY price growth and gross short-term yields approaching 10%, Lisbon is one of the few European markets delivering meaningful returns across both income and appreciation tracks simultaneously.

Madrid, Spain

Madrid is Western Europe's most liquid mid-to-large investment market in 2025. Spain's GDP growth is forecast well above the Euro area average, and a deep pool of domestic and foreign buyers keeps vacancy rates consistently low. Demand drivers — expats, students, corporate relocations — are structural, not cyclical.

What differentiates Madrid: lower entry prices than Paris or Amsterdam, solid rental yields anchored by high demand, and a regulatory environment that still welcomes international buyers without restrictions. Premium neighborhoods like Salamanca attract established investors, while emerging areas like Tetuán offer compelling entry points at lower price ranges.

| Metric | Figure | Source Context |

|---|---|---|

| Entry Price Range | €3,500–€4,500/sqm (city average) | Central districts command premiums; outer neighborhoods offer affordability |

| Gross Rental Yield | 6–6.5% | Supported by strong tenant demand and low vacancy rates |

| Economic Indicator | 2.5% GDP growth (2025 forecast) | Well above Euro area average; unemployment trending downward |

For investors prioritizing capital security alongside income, Madrid's combination of GDP-backed demand and low vacancy makes it one of the more defensible positions in European real estate right now.

Warsaw, Poland

Central Europe's high-yield story in 2025 is Warsaw. Annual price growth has been consistently in double digits, and rental demand from a growing tech and business sector keeps vacancies low. Poland's EU membership, improving infrastructure, and demographic urbanization underpin that demand at a structural level.

Why Warsaw offers compelling risk-adjusted returns: entry prices remain relatively affordable compared to Western Europe, gross rental yields are among the EU's highest, and the city's housing market is supported by both domestic demand and a new wave of foreign workers and investors.

| Metric | Figure | Source Context |

|---|---|---|

| Entry Price Range | €4,300/sqm (city average, late 2024) | Significantly lower than comparable Western European capitals |

| Gross Rental Yield | ~8% | Among the highest in the EU for established capital cities |

| YoY Price Growth | 12–14% (2024) | Double-digit appreciation supported by strong fundamentals |

At ~8% gross yield and 12–14% YoY appreciation, Warsaw is producing the kind of total return profile that's genuinely difficult to find in more mature European markets.

Riga, Latvia

Riga delivers Europe's highest-yield residential market on a gross rental basis. This Baltic capital is consistently undervalued relative to its economic maturity as an EU and NATO member state. Foreign buyers face no purchasing restrictions in Latvia, and the city's rental market benefits from strong demand from the Baltic business community, students, and a growing expat population.

Riga's case is primarily yield-driven. According to the Global Property Guide, the city-wide average gross rental yield stood at 8.61% as of Q2 2025, with Vecriga (Old Town) reaching 9.81%. Entry prices are significantly lower than most EU capitals, making cash-on-cash returns attractive for income-focused investors.

Market liquidity is lower than Western European cities, and transaction volumes are smaller. Investors should plan for medium-to-long holding periods (5–10 years) to ride out short-term liquidity fluctuations while collecting high annual yields.

| Metric | Figure | Source Context |

|---|---|---|

| Entry Price Range | €863/sqm (standard estates) to €3,000+/sqm (premium city center) | Extreme price bifurcation; focus on premium new builds for rental stability |

| Gross Rental Yield | 8.61% (city average), 9.81% (Vecriga) | Highest in Europe among capital cities with established legal frameworks |

| Market Liquidity | Growing but limited | Premium segment hit €250M in H1 2025 (+28% YoY), but overall volumes remain smaller than Western capitals |

Riga's low transaction costs (approximately 4.5% total, including a 1.5% Land Register fee) improve first-year ROI significantly compared to markets like Spain.

Critical Risk Warning: A June 2025 amendment to Latvia's Apartment Ownership Law makes new owners responsible for prior utility and reserve fund debts tied to the property. Strict legal due diligence is essential before finalizing any transaction.

Bucharest, Romania

Bucharest is 2025's highest-upside emerging market in the EU. Property prices remain among the most affordable per square meter of any European capital.

Three structural demand drivers are accelerating that upside: Romania's full Schengen membership (effective January 1, 2025), GDP growth exceeding the EU average, and a rapidly expanding tech and outsourcing sector.

The investment thesis: buyers today are entering at historically low valuations relative to comparable EU capital cities, with meaningful appreciation runway as Romania integrates further into European financial and mobility systems. Legal due diligence is especially important in Bucharest given the market's relative opacity. Working with vetted local partners is essential for title verification.

| Metric | Figure | Source Context |

|---|---|---|

| Entry Price Range | ~€1,500/sqm (city average) | Among the lowest in EU capital cities, creating significant appreciation potential |

| Gross Rental Yield | 6–7% | Supported by growing expat and business communities |

| Key 2025 Catalyst | Romania's Schengen accession | Expected to drive cross-border investor demand and property value appreciation |

At ~€1,500/sqm with 6–7% gross yields, Bucharest is priced for where it is today — not where it's likely to be in five years. Investors willing to accept frontier market opacity in exchange for early-entry pricing will find the risk-reward here difficult to replicate elsewhere in the EU.

How We Selected These Cities

City selection was based on five quantifiable criteria:

- Gross rental yield — actual income return on purchase price

- Year-over-year price growth — capital appreciation trajectory

- Affordability of entry — price per sqm relative to income and yield

- Ease of purchase for foreign buyers — legal restrictions and transaction costs

- Structural demand durability — population growth, employment trends, and tourism or digital nomad activity

Understanding Net vs. Gross Yield

Many investors overlook a critical distinction: gross yield and net yield can differ sharply once local income taxes on rent, property management costs, vacancy rates, and transaction fees are factored in.

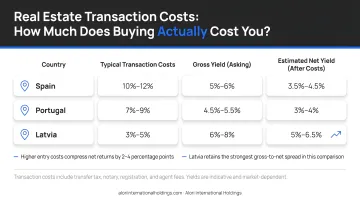

Transaction costs vary significantly across EU countries:

- Spain: ~10% at closing (transfer tax, notary, registration)

- Portugal: 6-8% (lower IMT transfer tax than Spain)

- Latvia: ~4.5% (highly competitive, with 1.5% Land Register fee)

Headline yield figures require adjustment for these local realities. A property advertising 8% gross yield in a market with 10% transaction costs and 2% annual property tax delivers a very different net return than one in a 4.5% transaction cost jurisdiction with no annual property tax.

City-Level vs. Country-Level Data

We cross-referenced market-level data against city-level figures because country averages often obscure neighborhood-level opportunities. For example, select districts in Riga outperform the national average by several percentage points, and Lisbon's Alfama vs. Parque das Nações show very different yield and appreciation profiles.

Liquidity and Exit Strategy

A 9% yield means little if you can't sell. Markets with thin transaction volume or complex ownership restrictions can lock up capital for years — which is why liquidity was a core filter, not an afterthought. Every city in this list offers verifiable exit channels through established buyer pools and transparent legal frameworks.

What Was Intentionally Excluded

Several otherwise attractive markets were deliberately left out:

- Amsterdam and Barcelona — active policy restrictions on foreign short-term rentals undermine yield sustainability

- Speculative run-up markets — cities where recent price growth isn't supported by underlying yield fundamentals

- Restricted-ownership jurisdictions — markets with uncertain or evolving regulatory environments for foreign buyers

What American Investors Should Know Before Buying

Buying property in Europe carries real transactional complexity that catches many American investors off guard — unexpected legal steps, unfamiliar closing structures, and residency requirements that vary by country. Going in unprepared means slower closings, higher risk, and costly mistakes.

Most EU countries permit US citizens to purchase freely, but the transaction process differs significantly from US closings and typically requires a local legal representative (advogado in Portugal, notario in Spain, sworn notary in Latvia).

Tax Obligations

American investors remain subject to US tax obligations on global income — including foreign rental income — regardless of where the property sits. Before closing, work with a US tax advisor experienced in international real estate who can navigate relevant US-EU tax treaties and FBAR/FATCA reporting requirements for foreign accounts.

Currency and Financing Considerations

Nearly all European transactions close in euros, which introduces several practical considerations for US-based buyers:

- Exchange rate risk: Dollar/euro movements directly affect your total return — a 5-10% currency shift can offset months of rental income

- Local mortgages: Non-resident financing is available but typically requires 30-40% down, with stricter income documentation than US lenders require

- Cash purchases: Most American buyers in the $150,000-$600,000 range pay cash, which streamlines the process — but makes proper legal structuring and title verification even more important

Conclusion

The best European cities for real estate investment in 2025 span a spectrum—from established, liquid markets like Lisbon and Madrid that reward patient capital with steady appreciation, to high-yield emerging markets like Warsaw, Riga, and Bucharest that offer stronger income returns at lower entry price points. The right choice depends on your time horizon, return objective, and risk appetite.

Market selection is only part of the equation. Execution quality determines actual outcomes: understanding local legal structures, sourcing deals through verified channels, and defining an exit strategy before capital is deployed. These factors separate investors who build durable international portfolios from those who encounter costly delays or illiquid exits.

For investors specifically considering Portugal or Georgia, Alori International Holdings focuses on exactly that kind of execution. The firm curates a small number of rigorously vetted property opportunities in each market—projects with verified legal structures, clear pricing rationale, and defined exit strategies built in from the start. Their model is built for American investors who want meaningful international exposure without navigating unfamiliar legal and transactional terrain alone.

Ready to explore European real estate investment opportunities? Contact Alori International Holdings at info@aloriinternationalholdings.com to learn which markets align with your investment objectives and what current opportunities look like on the ground.

Frequently Asked Questions

Where is the best real estate market in Europe?

The answer depends on investment objective. Lisbon and Madrid lead for capital appreciation and lifestyle value, Warsaw and Riga lead for rental yield, and Bucharest offers the highest upside potential as an emerging EU market. No single market is "best" for all investor profiles.

Which country is best to invest in real estate in Europe?

Portugal and Spain offer stability and foreign buyer accessibility, while Poland delivers strong yield and price growth. Always drill down to city-level data — national averages often obscure where the real opportunity sits.

Which European city has a growing real estate market?

Lisbon, Warsaw, and Bucharest show the strongest sustained price growth trajectories in 2025, each backed by rising foreign investment, housing undersupply, and improving economic fundamentals.

What rental yields can investors typically expect in European cities?

Gross yields range from roughly 3–4% in premium Western European markets like Paris and Berlin, up to 7–9% in Central and Eastern European cities like Riga and Warsaw. Net yields drop meaningfully once taxes, management fees, and vacancy are factored in.

Can US citizens buy property in Europe without restrictions?

US citizens can generally purchase residential property freely across EU member states without residency requirements. However, transaction processes, legal requirements, and closing costs vary significantly by country, making local legal counsel essential.