Introduction

Portugal consistently draws American investors seeking European exposure, stable markets, and quality-of-life advantages — but the tax landscape is what most buyers underestimate before signing. Many arrive focused on purchase price and location, only to discover later that the actual cost of ownership includes multiple tax layers they never modeled into their returns. This is the "hidden math" behind every Portugal property deal.

The full tax picture spans four distinct stages of ownership:

- At purchase: IMT (property transfer tax) and stamp duty

- Every year you hold: IMI (annual property tax) and potentially AIMI for higher-value portfolios

- When you sell or rent: capital gains tax and rental income tax

- As a foreign national: specific obligations that apply regardless of residency status

This guide covers each layer in plain language — with current rates, worked examples, and the considerations that matter most for American investors buying in Portugal.

TLDR: Portugal Property Tax Quick Reference

- IMT — One-time, progressive tax ranging from 0% to 8% of property value, paid before signing the deed — typically the largest upfront tax cost at closing

- IMI — Urban properties taxed between 0.3% and 0.45% of assessed value annually; rural properties at 0.8%

- Stamp Duty — 0.8% of purchase price paid at deed signing; also applies to mortgages (0.5%–0.6% depending on loan term)

- AIMI — Applies only to properties valued above €600,000 — rates range from 0.7% to 1.5% depending on value tier

- Capital gains tax — Non-residents are taxed on 50% of gains at progressive rates under current rules

- Rental income tax — A 10% rate applies to moderate rents; otherwise the standard 25% rate applies to non-residents

One-Time Taxes When Buying Property in Portugal

The IMT (Imposto Municipal sobre as Transmissões Onerosas de Imóveis) is Portugal's property transfer tax, paid by the buyer before the deed is signed. It's calculated against whichever is higher: the declared deed value or the government's assessed taxable value (VPT).

Undervaluing a property in the deed won't reduce your IMT — you'll still owe tax on the government's higher VPT figure.

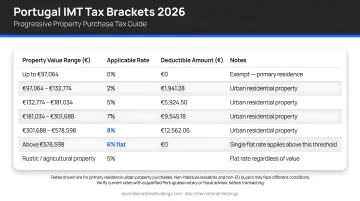

IMT Rates for Primary Residence (Urban Properties, Mainland Portugal)

For primary residences in mainland Portugal, the 2026 progressive IMT brackets are:

| Property Value (€) | Marginal Rate | Deductible Amount (€) |

|---|---|---|

| Up to 106,346 | 0% | 0.00 |

| 106,346.01 to 145,470 | 2% | 2,126.92 |

| 145,470.01 to 198,347 | 5% | 6,491.02 |

| 198,347.01 to 330,539 | 7% | 10,457.96 |

| 330,539.01 to 660,982 | 8% | 13,763.35 |

| 660,982.01 to 1,150,853 | 6% (Flat Rate) | N/A |

| Above 1,150,853 | 7.5% (Flat Rate) | N/A |

To calculate your exact IMT, multiply the property value by the marginal rate and subtract the deductible amount. For example, a €250,000 property falls in the 7% bracket: (€250,000 × 0.07) − €10,457.96 = €6,042.04 IMT owed.

Non-Standard Property Types

Not all properties use the progressive tables. Flat rates apply to:

- Rural/agricultural land: 5%

- Commercial properties and building plots: 6.5%

- Tax haven entities: 10% (punitive rate when purchasing through a company incorporated in a jurisdiction Portugal classifies as a tax haven)

Investor buyers structuring purchases through holding companies should verify their jurisdiction against Portugal's tax haven list before proceeding.

Stamp Duty (Imposto de Selo)

Stamp duty is the second one-time tax at purchase: 0.8% on the property deed paid to the notary at signing. If you're financing with a mortgage, additional stamp duty applies to the loan itself — 0.6% for loan terms over 5 years, 0.5% for shorter terms. Corporate purchasers are exempt from stamp duty on property transactions.

Stamp duty also applies in inheritance and gift scenarios: immediate family (spouse, children, parents) pay 0.8%; non-family recipients pay an additional 10% stamp duty, totalling 10.8%. There is no separate inheritance or gift tax in Portugal — this stamp duty is the only tax triggered.

Annual Property Taxes in Portugal: IMI and AIMI

IMI (Imposto Municipal sobre Imóveis) is Portugal's annual property tax — the equivalent of what American buyers know as property tax. Each municipality sets its own rate within a legally permitted range, and the tax is owed by whoever holds the property on 31 December of the tax year.

Understanding the Taxable Value (VPT):

IMI is calculated against the Valor Patrimonial Tributário (VPT), a government-assessed figure that often runs below market price. The tax you pay is based on the VPT, not what you paid for the property.

How IMI is calculated:

If a buyer holds an urban apartment with a VPT of €200,000 in a municipality that sets the IMI rate at 0.35%, the annual IMI owed is €700 (€200,000 × 0.0035).

The applicable rate depends on when your property was last assessed:

- Re-evaluated after 2004: IMI rate of 0.3%–0.45%

- Not re-evaluated since before 2004: Rate up to 0.8%

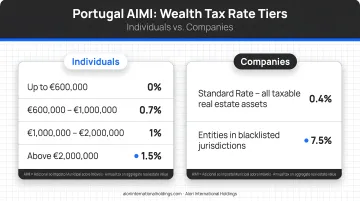

AIMI (Wealth Tax)

AIMI (Adicional Imposto Municipal sobre Imóveis) is Portugal's wealth tax on property holdings. It triggers only when an individual's total Portuguese property value exceeds €600,000.

Rate tiers:

- €600K to €1M: 0.7%

- €1M to €2M: 1%

- Above €2M: 1.5%

Companies pay a flat 0.4% on total Portuguese holdings above €600K, with no exemption threshold.

For married couples, the picture is different. Filing jointly raises the combined threshold to €1.2M before AIMI applies — making joint ownership more tax-efficient for portfolios under that €1.2M mark.

Regional Tax Advantage: Madeira and Azores

The autonomous regions of Madeira and the Azores apply a standard reduction to IMI rates — roughly 20% below the equivalent mainland rate. For investors comparing mainland and island locations, this reduction is a material factor. The after-tax annual holding cost on an island property can be meaningfully lower than the headline rate suggests, which affects long-term return calculations on comparable assets.

IMI Payment Schedule

The Portuguese tax authority (AT) sends payment notices by 30 April each year, either by mail or through the digital finance portal. Payment is structured by total amount owed:

- ≤ €100: Single instalment (31 May)

- €100.01 to €500: Two instalments (31 May and 30 November)

- > €500: Three instalments (31 May, 31 August, and 30 November)

Capital Gains and Rental Income Taxes in Portugal

Capital gains tax in Portugal is triggered when you sell a Portuguese property at a profit. As of 2026, non-residents are now taxed on only 50% of their capital gain, with that half added to their overall income and taxed at progressive rates. This aligns with the treatment for tax residents and replaces the previous flat 28% rate.

Primary Residence Rollover Exemption:

Two exemptions apply for tax residents:

- Main home reinvestment: Selling your primary residence and reinvesting proceeds into another primary residence — between 24 months before the sale and 36 months after — exempts the gain from capital gains tax entirely.

- Retiree/over-65 option: Residents aged 65+ or retirees who invest sale proceeds into qualifying pension or insurance products within 6 months of the sale also qualify for exemption.

Rental Income Taxation

Rental income taxation is a key concern for investors in the €150K–€600K range who intend to generate yield. The 2026 State Budget introduced a reduced 10% rate for residential rental income if the rent is considered "moderate" (typically up to €2,300 per month, depending on municipality and typology). Otherwise, the standard flat rate of 25% applies to gross rental income.

Deductible expenses (with receipts) include:

- Maintenance and repairs

- Utilities, condominium fees, and rent insurance

- IMI and AIMI property taxes

Mortgage interest and depreciation are not deductible. Residents are taxed on rental income at progressive income tax rates rather than the flat rates above.

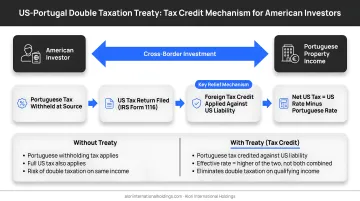

US-Portugal Tax Treaty Considerations

The US taxes worldwide income, meaning American investors must report Portuguese rental income and capital gains on their US federal returns even while also paying Portuguese tax. The US-Portugal double taxation treaty provides mechanisms (tax credits) to prevent Americans from being taxed twice on the same income — understanding this treaty before purchasing can meaningfully affect your net return calculation.

Capital gains liability shifts meaningfully based on your residency status, holding structure, and whether proceeds are reinvested — each variable should be modeled into your return projections before committing to a purchase price.

Tax Exemptions and Ways to Reduce Your Bill

Portugal offers several exemptions and incentives that can significantly reduce your tax burden if you qualify.

3-Year Temporary IMI Exemption

Buyers who purchase a property as a permanent primary residence — or rent it out — may qualify for a 3-year IMI exemption. To be eligible:

- The property must be an urban property with a VPT at or below €125,000

- The buyer's taxable income in the prior year must fall below €153,300

- The exemption requires a proactive application to Finanças — it is not granted automatically.

Permanent IMI Exemption

Lower-income households may qualify for a permanent IMI exemption if annual taxable household income falls below a threshold set and adjusted by the government each year. Confirm the current figure directly with Finanças, as it can change.

Other IMT Exemptions

- Properties acquired for urban rehabilitation are exempt from IMT, provided works begin within three years of purchase

- Purchases by real estate investment funds designated for residential letting qualify for exemption

- Properties classified as being of national or municipal interest are also exempt from IMT

Properties in Madeira and the Azores carry built-in tax advantages — lower IMI rates and more favorable IMT brackets — making them natural targets for investors seeking regional incentives alongside long-term returns.

Practical Tax Compliance: What Foreign Buyers Need to Do

The NIF (Número de Identificação Fiscal) is the Portuguese tax identification number every foreign property owner must obtain before completing any transaction — opening a bank account, signing a deed, or paying taxes. Non-EU citizens, including Americans, are legally required to obtain their NIF through a licensed fiscal representative: a Portuguese resident (lawyer, accountant, or trusted individual) who assumes legal responsibility for the buyer's tax compliance.

One important distinction: having a NIF does not make you a tax resident. It simply registers you in the Portuguese tax system.

Paying Your Taxes

Property taxes are paid through the Portuguese Finance Portal (Portal das Finanças), where foreign owners can view obligations, payment schedules, and submit payments online. Additional payment options include:

- ATMs (Multibanco network)

- Homebanking through a Portuguese bank

- In person at a tax office (Finanças)

- CTT post office branches

Foreign owners who miss payment deadlines face interest charges and potential enforcement action, so having a local fiscal representative or property manager monitor these obligations is essential.

Where Alori Adds Value

Knowing the tax framework matters — but running the actual numbers on a specific deal requires in-market precision. Purchase taxes, annual holding costs, rental yield after tax, and exit-stage capital gains all affect real returns. Alori International Holdings works with investors on curated Portuguese real estate opportunities that include verified legal structures and defined exit strategies from the outset. Buyers enter with a clear picture of their full cost and return profile, not just the asking price.

Frequently Asked Questions

How much is property tax in Portugal?

The main ongoing tax is IMI (0.3%–0.45% for urban properties annually). AIMI applies additionally only for properties above €600,000. One-time purchase taxes (IMT and stamp duty) are separate costs paid at acquisition.

What fees are there when buying a house in Portugal?

Main acquisition costs include IMT (progressive, 0%–8%), stamp duty (0.8% on the deed), notary fees, and legal/fiscal representation costs. Buyers — not sellers — are responsible for these taxes.

How much tax do you pay when selling a house in Portugal?

Capital gains tax applies on the profit from the sale. As of 2026, both residents and non-residents are taxed on 50% of the gain at progressive rates — aligning treatment that previously differed. Residents who reinvest proceeds into another primary residence within 36 months may qualify for an exemption.

How often do you pay property tax in Portugal?

IMI is an annual tax. Payment notices are issued by 30 April, with payments structured in one, two, or three instalments across May–November depending on the total amount owed.

Does owning property in Portugal make you a tax resident?

No. Property ownership alone does not create tax residency. Tax residency is triggered by spending 183 or more days per year in Portugal, or by establishing it as a permanent habitual residence.

What are the property taxes in Portugal for foreigners?

Foreigners pay the same property taxes as Portuguese nationals — IMT, stamp duty, IMI, and AIMI where applicable. Prior to 2026, non-residents faced less favorable flat rates on capital gains, but recent reforms have aligned that treatment. American buyers should also factor in US obligations on worldwide income, as Portugal property gains must be reported to the IRS.