Introduction

Brexit fundamentally rewrote the retirement calculus for UK nationals. Since January 2021, British citizens can no longer live indefinitely anywhere in the EU under freedom of movement — they now face the same visa and residency requirements as any non-EU citizen.

Americans are reassessing the same landscape. Dollar strength and rising US living costs have pushed European retirement up the agenda, with 40% of high-net-worth Americans reportedly planning to purchase property abroad within the next year.

That means both groups now confront the same reality: a patchwork of national visas, income thresholds, and residency permits that vary country by country. Automatic healthcare access is gone. Indefinite stays require formal applications, documented income, and ongoing compliance.

This guide covers five European destinations that hold up under that scrutiny — what makes each one practical, what the residency path actually looks like, and which factors should carry the most weight in your decision.

Key Takeaways

- Brexit ended EU freedom of movement for UK citizens in 2021—British and American retirees now need formal visas to stay beyond 90 days

- Portugal ranks top due to its D7 visa (€870/month income threshold), low costs, warm climate, and five-year path to citizenship

- Spain, Italy, Greece, and France each have their own visa structures, with income thresholds ranging from €870 to €3,500 monthly

- Healthcare access, property ownership rules, and tax treaties vary significantly by country — verify each before committing

- Purchasing property can anchor residency rights and serve as both lifestyle asset and investment

What Brexit Changed for Anyone Retiring to Europe

Before January 2021, UK citizens could live, work, and retire anywhere in the EU without restriction. Today, they're treated as third-country nationals subject to Schengen's 90-day-in-180-day rule—exactly like US citizens.

That same reality applies to any non-EU retiree, regardless of nationality. Each country runs its own retirement or passive income visa program, typically requiring proof of income (often €1,000–€2,500/month depending on the country), private health insurance, and confirmed accommodation. Without formal residency, you're capped on legal stay time and cut off from public services entirely.

That said, a number of EU countries have actively expanded their retirement visa programs since Brexit to attract financially independent foreign residents. Portugal's D7 visa applications from non-EU nationals surged by over 30% between 2021 and 2023—a clear signal that the market for internationally mobile retirees is growing, not shrinking.

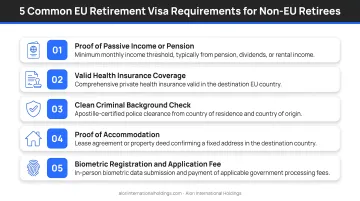

Key requirements most EU retirement visas share:

- Proof of passive income or savings meeting the country's minimum threshold

- Private health insurance valid in the host country

- Confirmed accommodation (rental contract or property ownership)

- Clean criminal record from your home country

- Registration with local municipal authorities within a set timeframe

Best Places to Retire in Europe After Brexit

Choosing where to retire in Europe comes down to a short list of practical factors: visa pathways you can actually qualify for, healthcare you can rely on, and a cost of living that makes sense for your income. Each destination below was evaluated on those grounds — accessible visa routes, cost of living relative to lifestyle quality, healthcare access, expat community size, and property market entry.

Criteria used in this comparison:

- Visa accessibility — income thresholds, permit durations, and renewal complexity

- Cost of living — relative to Western European and US baselines

- Healthcare — public access eligibility and private insurance requirements

- Expat infrastructure — English-language services, community size, integration ease

- Property market — purchase restrictions, mortgage access for non-residents

Portugal

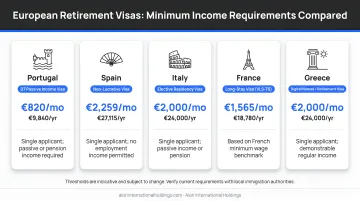

Portugal consistently leads retirement destination rankings for non-EU citizens. The D7 Passive Income Visa requires a modest monthly income threshold of approximately €870 for a single applicant (roughly $950 USD), offers a clear pathway to permanent residency after five years, and combines seamlessly with straightforward property purchase.

Key differentiators for post-Brexit retirees:

- Large, well-established anglophone expat communities in Lisbon, Porto, and the Algarve

- Cost of living significantly below Western European averages

- High-quality public healthcare accessible once residency is established

- Favorable tax treatment for foreign pension income (the Non-Habitual Resident regime was replaced in 2024 with a modified framework offering reduced rates for new residents)

| Visa Criteria | Details |

|---|---|

| Visa Type | D7 Passive Income Visa |

| Minimum Monthly Income | €870 for single applicant; €1,305 for couples (€870 + €435 for spouse) |

| Path to Residency/Citizenship | Permanent residency after five years; citizenship eligibility after five years |

Spain

Spain delivers a Mediterranean climate, world-class healthcare, vibrant expat communities along the Costa del Sol, Valencia, and Barcelona, and a Non-Lucrative Visa designed specifically for financially independent non-working residents.

What sets Spain apart:

The income threshold is higher than Portugal's—€2,400 per month for a single applicant (based on 400% of Spain's IPREM benchmark)—but the lifestyle return is exceptional. Beaches, cuisine, low-cost domestic travel, and English widely spoken in coastal and tourist areas make it one of the most popular choices for British and American retirees.

Citizenship eligibility requires ten years — longer than Portugal, though achievable for long-term residents committed to the country.

| Visa Criteria | Details |

|---|---|

| Visa Type | Non-Lucrative Visa (residence without right to work) |

| Minimum Monthly Income | €2,400 for single applicant; €3,000 for couples (€2,400 + €600 per dependent) |

| Path to Residency/Citizenship | Temporary residency renewed annually; citizenship eligibility after ten years |

Italy

Italy appeals to retirees drawn to culture, cuisine, and high quality of life at a lower cost than its reputation suggests. The south and rural regions—Sicily, Calabria, Puglia, Abruzzo—offer sharply lower living costs than northern cities, and the Elective Residency Visa is a well-established route for non-EU nationals with sufficient passive income.

Key considerations:

The income requirement is higher than Portugal or Spain — approximately €31,000 per year for a single applicant. Private health insurance is required as a visa condition; Italy does not extend public health system access to Elective Residency Visa holders. Coverage must be comprehensive and in place before the visa is approved. Italy's private healthcare market is high quality and relatively affordable compared to US out-of-pocket costs.

| Visa Criteria | Details |

|---|---|

| Visa Type | Elective Residency Visa |

| Minimum Annual Income | €31,000 for single applicant; approximately €38,000 for couples |

| Path to Residency/Citizenship | Renewable residency permit; citizenship eligibility after ten years |

Greece

Greece stands out as the affordability option among Mediterranean retirement destinations. A three-bedroom apartment in a city center costs a fraction of equivalent accommodation in Lisbon or Barcelona, and overall cost of living is among the lowest in Western Europe.

The Financially Independent Person (FIP) visa offers a three-year residency permit with an income threshold of approximately €3,500 per month — higher than France or Portugal, but offset by significantly lower day-to-day living costs.

For retirees who intend to purchase property, the Greece Golden Visa offers a second path. It grants residency through qualifying real estate investment rather than income proof:

- Minimum investment: €250,000 in most areas

- Higher thresholds (€400,000–€800,000) apply in prime zones like central Athens and popular islands

- Residency obtained faster, without monthly income requirements

- Combines lifestyle migration with a tangible investment asset

| Visa Criteria | Details |

|---|---|

| Visa Type | FIP (Financially Independent Person) Visa or Golden Visa (investment route) |

| Income/Investment Requirement | FIP: €3,500/month; Golden Visa: €250,000–€800,000 property investment depending on location |

| Path to Residency/Citizenship | FIP grants three-year permit; citizenship eligibility after seven years |

France

France appeals to retirees who prioritize cultural richness, gastronomic lifestyle, and access to a world-class public healthcare system. The Long-Stay Visitor Visa (VLS-TS) is the primary route for non-EU retirees, requiring proof of income roughly equal to the French minimum wage — approximately €1,400 per month as of 2025.

France also has one of the largest British expat populations in Europe, with a well-embedded anglophone community concentrated in the southwest and Provence regions.

Practical realities:

Once residency is established, access to France's national health insurance system (L'Assurance Maladie) becomes available — one of the most comprehensive public coverage arrangements in Europe. Cost of living varies considerably by region; rural Brittany or the Dordogne runs far more affordable than Paris.

Property can be purchased without restrictions for non-EU buyers. Obtaining a French mortgage as a non-resident is more complex, and lenders typically require a larger deposit than they would from French nationals.

| Visa Criteria | Details |

|---|---|

| Visa Type | Long-Stay Visitor Visa (VLS-TS) |

| Minimum Monthly Income | Approximately €1,400 (equivalent to French minimum wage) |

| Path to Residency/Citizenship | Residency permit after visa validation; citizenship eligibility after five years |

What to Consider Before You Choose Your Destination

Cost of Living and Income Threshold Alignment

The single most common mistake retirees make is choosing a destination based on lifestyle appeal without stress-testing their income against the visa minimum and actual monthly costs. Calculate whether your pension, Social Security, investment income, or savings can comfortably clear the visa threshold with enough left over to live well.

Account for currency exchange risk. If your income is denominated in GBP or USD, fluctuations can erode purchasing power. For example, Valencia is roughly 13-14% cheaper than Barcelona excluding rent, while Malaga offers a strong balance of affordability and amenities along the Costa del Sol.

Healthcare and Insurance Planning

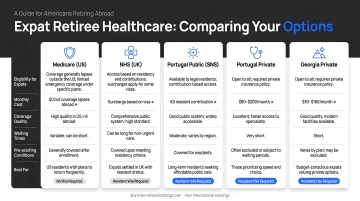

Medicare does not cover care outside the US, and post-Brexit British retirees no longer benefit from EHIC reciprocal arrangements in EU countries. Every destination on this list either requires private health insurance as a visa condition or requires a waiting period before public system access is available.

Budget considerations:

- Private expat health insurance for a retiree aged 60+ typically ranges from €1,200 to €3,000 annually depending on coverage level and country

- Spain strictly requires comprehensive private health insurance with no copayments and no waiting periods from an insurer authorized in Spain

- UK state pensioners can obtain an S1 form, which grants access to the Spanish state healthcare system, bypassing the private insurance requirement

Investigate whether your chosen country offers eventual access to public healthcare once residency is established.

Property Ownership as a Residency and Investment Strategy

For retirees with capital to deploy, purchasing property in your destination country can serve dual purposes: anchoring residency rights (via Golden Visa routes in Greece, Portugal, and others) and building a tangible asset in a market with durable demand.

What you need to know:

- Non-EU buyers can purchase freely in all five countries on this list

- Transaction processes, taxes, and legal requirements differ significantly

- Local expert guidance is essential to reduce transaction risk and provide clarity on exit and rental strategies from day one

For Portugal specifically, Alori International Holdings focuses on vetted property opportunities across the Algarve, Porto, and Lisbon — with local legal and market expertise to guide buyers through the Golden Visa process, accurate pricing, and defined exit strategies.

Conclusion

Brexit ended automatic EU retirement rights for UK citizens, and the reality is that retiring in Europe — whether you are British or American — requires deliberate planning, the right visa pathway, and a clear-eyed view of costs, healthcare, and legal residency requirements. The five destinations on this list represent the strongest balance of accessibility, lifestyle quality, and financial practicality for non-EU retirees today.

Anchor your decision in fundamentals — income alignment, healthcare coverage, and legal clarity — not just lifestyle appeal. Resist choosing a country based solely on climate or culture without fully understanding the residency mechanics and ongoing compliance requirements.

If purchasing property is part of your retirement plan, Alori International Holdings focuses specifically on curated real estate opportunities in Portugal and Georgia — two markets covered in this guide — with vetted legal structures, verified pricing, and defined exit strategies.

Reach out at info@aloriinternationalholdings.com to explore property options aligned with your retirement and investment goals.

Frequently Asked Questions

What is the $1000 a month rule for retirees?

The "$1,000 a month rule" is an informal benchmark for retiring comfortably in affordable countries — but it falls short in Western Europe. Visa income requirements and living costs here typically range from €870 to €3,500+ per month, depending on the country and your lifestyle.

Can I retire in Europe as a US citizen?

Yes — but as a non-EU national, you'll need a formal visa or residency permit in each country. Most offer a passive income or retirement visa (such as Portugal's D7 or Spain's Non-Lucrative Visa) requiring proof of sufficient income, private health insurance, and a clean criminal record.

What is the easiest European country to retire to?

Portugal stands out as the most accessible option for non-EU retirees. Its D7 visa has a low income threshold (€870/month), a straightforward application process, a large English-speaking expat community, and a five-year path to permanent residency.

Do I need a visa to retire in Europe after Brexit?

Yes, UK citizens are now subject to the Schengen 90-day-in-180-day rule and must obtain a formal national residency visa to stay longer in any EU country. Each country has its own program—you should apply in your home country at the relevant consulate before relocating.

Can I buy property in Europe as a British or American citizen?

Non-EU nationals—including British and American citizens—can purchase property freely in all five countries covered in this article. In some countries (such as Greece and Portugal), a property investment can be the basis for a Golden Visa residency application. Hire local legal counsel to navigate transfer taxes and documentation requirements.

Does Medicare or NHS coverage apply if I retire in Europe?

No. US Medicare doesn't cover care outside the United States, and post-Brexit UK nationals can no longer use EHIC arrangements in EU countries. You'll need private international health insurance until you establish formal legal residency and qualify for the local public health system.