Introduction

European commercial real estate closed Q4 2025 with clear momentum. After years of institutional caution, Europe's largest property markets are drawing serious capital again — transaction volumes rose sharply year-over-year, and pricing remains attractive relative to underlying fundamentals across most asset classes.

Throughout 2025, investors navigated mixed signals: uneven Eurozone growth, geopolitical friction, and residual caution from the 2023 correction. By Q4, the picture had clarified. Investment volumes surged, portfolio deals returned at their highest frequency since 2015, and cross-border capital flows resumed at scale.

This post covers what the data actually shows:

- Headline Q4 and full-year transaction volumes

- Which sectors led and which lagged

- Markets that outperformed — and why

- Where valuations stand relative to history

- What the 2026 setup means for investors weighing European exposure

TLDR: Q4 2025 European Real Estate at a Glance

- European CRE investment volumes reached €244.5bn for the full year (+17% YoY in Q4), confirming a sustained recovery across the continent

- Living sectors (multifamily, PBSA, senior housing, care) held the largest allocation share for the second consecutive year

- Retail staged a major comeback; logistics dipped on asset scarcity; offices showed selective recovery in prime locations

- Southern Europe led growth—Portugal, Spain, and Italy posted the strongest annual volume gains in the region

- 78% of tracked European markets remain underpriced relative to fundamentals, with prime yields edging inward

Q4 2025 Investment Volumes: The Headline Numbers

European CRE investment reached €88.3bn in Q4 2025, up 17% year-over-year, according to CBRE's Q4 2025 data. Full-year 2025 totals hit €244.5bn — the highest quarterly level since 2022.

Savills' preliminary estimate placed Q4 volumes at approximately €77bn, with full-year totals around €215bn. The gap reflects differences in market coverage scope and closing-date recording — both figures confirm meaningful year-over-year growth.

Portfolio transactions represented approximately ~40% of total deal volume — the highest share since 2015 — signalling that large institutional buyers have re-entered with conviction, executing sizeable multi-asset strategies.

Two transactions illustrate the scale of activity:

- Blackstone's ~€700M acquisition of the Centre d'Affaires Paris Trocadéro office building from Union Investment

- REICO's ~€682M two-property Czech Republic portfolio purchase, including Prague's Palladium shopping centre

These deals also reflect a broader geographic shift. Cross-border capital held a 45% share of total activity, with British, French, and Swedish buyers expanding outside their home markets — and notable new contributions from Australian and Japanese institutional investors.

Where This Sits in the Cycle

2023 was the trough — volumes at multi-year lows. 2024 was transitional. By 2025, genuine re-engagement is underway: institutions are deploying capital, debt markets are stabilizing, and pricing is firming across core markets.

Sector Performance: Who Led and Who Lagged

Four sectors shaped Q4 2025's investment landscape — each telling a different story about where capital is moving and why.

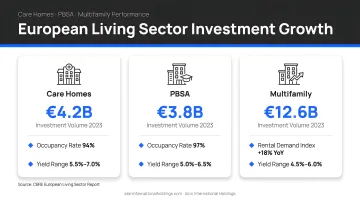

Living Sectors Dominated

Living sectors — multifamily, PBSA, senior housing, and care homes — collectively represented the largest share of total investment for the second year running. Two structural forces are driving this: persistent housing undersupply across major European cities and ESG alignment that makes these assets a natural fit for institutional allocators.

Within Living, standout sub-sectors included:

- Care home investment surged +182% YoY (comparing against a very weak prior period)

- PBSA grew +71%, reaching a record 6% share of total investment, driven by Europe's student population forecast to grow by 2.2 million by 2029/30

- Aging populations and household formation trends continue to support mid- to long-term structural demand across the category

Retail's Comeback

Retail recorded €25.3bn invested across Europe (+18.5% YoY), returning retail's investment share to levels last seen in 2016. Retail warehouses and shopping malls led the recovery, supported by rising rents, record-low vacancy in some markets, and a rebound in tourism-driven consumer spending.

Offices: Selective Recovery

Prime CBD offices in major capitals are seeing rent growth of 5–14% YoY in cities like Paris, London, and Munich. Return-to-office trends are supporting leasing in top-tier buildings, but secondary and non-ESG-compliant stock continues to face pressure. The bifurcation is widening, with ESG-compliant, well-located assets commanding premiums that secondary stock cannot match.

Logistics: Asset Scarcity, Not Weak Demand

Logistics was the only major sector to record a YoY decline in investment volume (down ~2.6%), but this reflects asset scarcity and competitive underwriting rather than weakening structural demand. Long-term fundamentals remain intact, including onshoring, reshoring, and defense-related supply chain activity that continues to drive occupier demand across core European markets.

Geographic Spotlight: Where the Growth Was Concentrated

The UK, Germany, and France continued to dominate by absolute volume, together exceeding half of total European investment. Momentum within these markets was uneven, though: Germany recorded strong logistics demand in major urban centers despite broader economic caution, while France saw Paris office vacancy pressures offset by solid luxury retail performance boosted by tourism. That unevenness is precisely what made Southern Europe's consistency notable.

Southern Europe was the standout regional story. Italy, Spain, and Portugal combined for over €27.4bn in investment (+19% YoY), according to Cushman & Wakefield data:

- Italy surged ~23% YoY, driven by retail, hospitality, and logistics

- Spain posted its strongest quarterly performance since 2022, closing the year with over €18.45bn

- Portugal was among the markets forecast to record over 20% annual growth, driven by hospitality, residential demand, and growing cross-border institutional interest

Portugal merits particular attention for American investors. Savills analysts named it among the top European markets expected to outperform in 2025–2026 — a call supported by its combination of hospitality-driven demand, favorable residency frameworks, and sustained cross-border capital inflows. Alori International Holdings focuses specifically on this market, sourcing off-plan and coastal residential opportunities for US-based investors with defined legal structures and exit strategies in place.

Emerging and mid-tier markets—Czech Republic, Finland, Denmark, Belgium, Sweden, Hungary, Norway—each recorded annual growth above 20%. Capital is moving beyond the traditional Big 3, and the spread is wide enough to suggest a structural shift rather than a one-quarter anomaly.

Pricing and Yields: A Rare Valuation Window

Cushman & Wakefield's Fair Value Index found that approximately 78% of tracked European real estate markets remain underpriced, with no markets classified as fully priced. Current pricing has not yet caught up with improving fundamentals—which may represent a buy-in window before broader repricing takes hold.

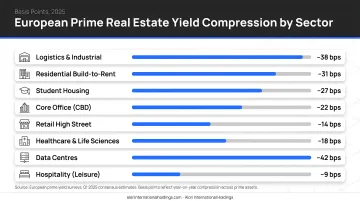

Yield compression in 2025 was more modest than markets expected:

- Luxury high-street retail: -17 bps

- PBSA: -10 bps

- Multifamily: -9 bps

- Most other sectors: ≤5 bps

That restrained compression reflects structural friction: limited forced sales, cautious debt markets, and persistent buyer-seller spread disagreements held pricing in check. For disciplined buyers who can move decisively, that friction is an advantage rather than a barrier.

The ECB cut rates from 4% to 2% over the course of the prior year. The full benefit hasn't yet reached borrowers, but the direction is clear. As of December 2025, the 3-month EURIBOR rate stood at 2.060%—a level that meaningfully reduces all-in financing costs compared to the peak, and improves deal economics for buyers entering now rather than waiting for further yield compression.

What the 2026 Outlook Means for International Investors

Savills forecasts investment volumes to grow ~18% in 2026 as pricing firms, macroeconomic conditions stabilize, and institutional capital returns more consistently. A further ~15% increase is projected for 2027, suggesting a multi-year recovery runway.

Top picks emerging from analyst research:

- Core/Core+: Prime CBD offices and hotels in key tourist gateways (Portugal, Spain, Italy, France, UK, Greece)

- Value-add: Logistics with rental reversion potential and manage-to-green office repositioning

- Opportunistic: Change-of-use and secondary office redevelopment

For American investors specifically, US policy uncertainty and a weaker dollar are cited by researchers as factors redirecting global capital toward Europe, where regulatory clarity and stable legal frameworks offer more predictable risk-adjusted returns.

For investors looking to act on this window, execution matters as much as timing. Alori's approach integrates global investment strategy with in-country expertise in markets like Portugal, providing access to off-market opportunities, vetted local partners, and transaction structures with defined entry and exit terms.

Frequently Asked Questions

Is real estate in Europe a good investment?

European real estate offers diversification, inflation-resistant income, and structural demand from housing undersupply and tourism growth. With 78% of tracked markets still underpriced and a multi-year recovery underway, entry timing is broadly favorable—though market selection and pricing discipline determine outcomes.

What was the total European real estate investment volume in 2025?

CBRE reported full-year 2025 volumes of €244.5bn; Savills estimated ~€215bn. The gap reflects differences in market coverage and closing timelines, but both figures confirm strong YoY growth and a sustained recovery from the 2023 trough.

Which European countries are best for real estate investment right now?

Portugal, Spain, Czech Republic, Finland, and Sweden recorded 20%+ annual growth in 2025. Southern Europe broadly is attracting significant cross-border capital, driven by hospitality demand, residential undersupply, and lifestyle migration trends among international buyers.

What sectors are leading European real estate investment?

Living sectors (multifamily, PBSA, senior housing) represented the largest share for the second consecutive year, followed by offices and retail's strong comeback. Logistics declined slightly due to asset scarcity rather than weak demand, with long-term fundamentals remaining intact.

Are European property yields still attractive?

Prime yields compressed only modestly in 2025 (most sectors moved ≤5 bps), meaning entry pricing remains relatively attractive compared to historical norms. Cushman & Wakefield confirms the majority of European markets are still underpriced relative to fundamentals.

How are ECB rate cuts affecting European real estate investment?

ECB rate cuts from 4% to 2% have steadily improved financing conditions, with debt-financed deals recovering faster than equity-driven ones. The 3-month EURIBOR now sits at 2.060%, making 2025–2026 a more favorable window for new market entries.