Introduction

After two years of price corrections and frozen credit markets, European residential real estate is recovering — but unevenly. The European Central Bank's rate cuts have brought the deposit facility rate to 2.00% by mid-2025, reopening buyer access that had been suppressed since 2022.

Falling rates, however, don't resolve the continent's structural supply deficit. That tension — between improving affordability and chronic undersupply — defines the current market. Diverging national conditions mean the difference between markets gaining real momentum and those still working through excess.

Drawing on data from Eurostat, CBRE, and AEW Research, this article maps the key price and demand trends across European housing markets, identifies where the structural investment case is strongest, and highlights which markets warrant attention in 2025.

Key Takeaways

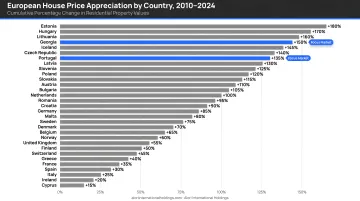

- EU house prices rose 55.4% between 2010 and Q4 2024, with a modest recovery underway after a brief 2023 dip

- Europe faces a housing shortage of approximately 9.6 million homes — roughly 3.5% of current stock — with permit levels still falling short

- ECB rate cuts have lowered the Eurozone average mortgage rate to approximately 3.35%, stimulating demand unevenly across countries

- Prime residential rents are projected to grow 3.2% per year through 2025–29 — outpacing expected 2.0% inflation and strengthening the case for income-focused property investing

- Transaction volumes are rising in Portugal, Spain, the Netherlands, and Belgium; Ireland, Finland, and Hungary are seeing declines

What's Driving the European Residential Market in 2025?

ECB Rate Cuts Reopen Buyer Access to Credit

The primary demand catalyst for 2025 is monetary easing. The ECB began a significant rate-cutting cycle in June 2024, lowering the deposit facility rate to 2.00% by June 2025 — a substantial reversal from the tightening that defined 2022–2023.

These cuts have made borrowing cheaper, with the Eurozone average mortgage rate declining to approximately 3.35% by end-2024. For buyers locked out during the high-rate period, this represents a genuine reopening of credit access.

Uneven Transmission Across Europe

Rate cuts affect markets differently depending on local mortgage structures:

- Eurozone markets with long-term fixed-rate mortgages experience slower transmission of rate cuts to borrowers

- UK and variable-rate markets see faster benefits from policy easing

- Supply constraints and regulatory differences further moderate the response — cheaper credit does not automatically translate into price surges when inventory remains scarce

House Price Recovery Underway

EU-wide house prices dipped slightly in 2023 but returned to growth in 2024. According to Eurostat, prices rose in Q4 2024, signalling the correction has ended. Forecasts project roughly 3.5% per annum price appreciation in the Eurozone through 2025–29, a sustainable pace supported by structural demand rather than speculative momentum.

Government Schemes Stimulate First-Time Buyers

Several markets have introduced schemes to boost first-time buyer activity. Portugal's Public Guarantee program for under-35s is a clear example — it expands access to mortgages but also triggers seller price increases as more buyers compete for limited stock.

This dual effect is common across Europe: government support increases demand without addressing supply, often pushing prices higher.

Broader Macro Tailwinds

Several structural factors support the recovery:

- Wage growth is offsetting rent increases, maintaining affordability for employed households

- Improving investor sentiment as yields stabilise and debt costs fall

- Residential now accounts for approximately **21% of total European property investment volumes**, up sharply from just 8% in 2008

That 13-percentage-point shift is not incidental — it reflects a structural reallocation of capital toward an asset class that has consistently delivered inflation-linked income through multiple rate cycles.

Europe's Supply Crisis: Too Few Homes, Too Much Demand

The Core Structural Problem

Europe's housing shortage sits at roughly 9.6 million homes — roughly 3.5% of existing stock as of 2024. Current construction output is projected to reach only around 64% of desired levels in 2025, meaning the shortage is expected to worsen before it improves. This supply-demand imbalance is the primary structural force keeping prices and rents elevated across the continent.

Construction Permit Collapse

EU-27 residential building permits peaked near 2 million in 2021, then fell sharply. Permits have dropped approximately 27% from that peak and now run near post-Global Financial Crisis lows. What is suppressing new development?

- High build costs driven by materials and labour inflation

- Elevated land prices in desirable locations

- Financing costs that remain high despite recent ECB cuts

- Regulatory uncertainty around sustainability requirements and planning approvals

National Construction Shortfalls

The supply gap looks different market to market:

- Germany: Delivered around 251,900 apartments in 2024, down 14.4% from 2023 and far below the government target of 400,000 annually. For 2025, industry associations expect only 225,000–230,000 units

- Netherlands: Added 82,000 homes to stock in 2024 (69,000 new builds), missing the government target of 100,000 homes per year

The gap between policy targets and actual delivery is consistent enough to be structural, not cyclical.

The Shrinking Rental Stock Problem

In several markets — including the UK, Netherlands, and France — fiscal and regulatory changes have made buy-to-let less attractive to private landlords, shrinking the available rental pool. Two forces are compounding the problem:

- Landlord exit: Higher taxes and tighter regulations are pushing private owners to sell rather than rent

- Platform competition: Short-term letting platforms like Airbnb continue drawing stock away from long-term rental supply

This directly feeds rental price pressure even where overall housing demand is not unusually high.

Why a Rapid Fix Is Unlikely

Even under optimistic construction scenarios, resolving the shortage would take more than four years of sustained output above current levels, independent of ongoing household growth. For investors, that timeline matters: rental income and capital values across much of Europe have structural support that demand-side shocks alone cannot unwind.

House Prices and Rents: What the Data Shows

Long-Run Price Appreciation

EU house prices rose 55.4% between 2010 and Q4 2024, with the largest national gains observed in Hungary (+234%), Estonia (+228%), and Lithuania (+187%). This compares to cumulative inflation of approximately 39% over the same period, meaning real house price gains were substantial across most of Europe. Portugal has been a standout performer within this trend, recording approximately +40.6% in real terms from Q2 2020 to Q2 2025 — one of the strongest performances in the EU.

Transaction Volume Picture for 2025

Rising prices haven't dampened buyer activity. EU home sales posted approximately 10% year-on-year growth in Q2 2025. Markets with rising volumes:

- Luxembourg, Slovenia, Lithuania, Belgium, Portugal, and the Netherlands (all showing rising volumes)

- France led in absolute volume with approximately 244,750 sales in a single quarter

Markets with declining volumes:

- Ireland (-10%)

- Malta (-6.2%)

- Hungary (-5.7%)

- Finland (-5.6%)

Rental Market Trajectory

Prime European residential rents grew approximately 4.7% in 2024, in line with the 2020–24 average. Forward projections point to approximately 3.2% per annum rental growth through 2025–29, ahead of expected inflation of around 2.0% per annum.

Cities expected to outperform include Madrid, Amsterdam, Berlin, and London — all facing acute supply shortages and strong tenant demand.

Affordability Pressure Constrains Rent Growth

EU households spent an average of 19% of disposable income on housing in 2024. In cities, nearly 10% of the population carries a severe housing cost burden, spending more than 40% of disposable income on housing. This tension between supply-driven rental growth and tenant affordability is the central regulatory pressure point shaping how governments respond — and the primary driver of rent control legislation now advancing in several EU capitals.

Investment Activity and the Yield Outlook

Recovery in Investment Volumes

European residential investment totaled approximately €40 billion in 2024, a 25% increase from 2023, though still approximately 25% below the 10-year average. This recovery was driven primarily by activity in the Nordics, Spain, and the Netherlands. Transaction pipelines in France and the UK should push 2025 volumes higher.

Yield Outlook and Return Drivers

Prime European residential yields peaked at approximately 4.1% in 2024 and have begun compressing again, having moved in by roughly 10 basis points from that peak. Forecasts indicate an average of 30 basis points of further compression through 2029, partially reversing the 130 basis points of widening seen in 2022–23.

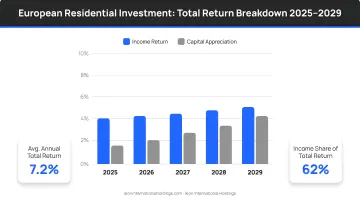

In the near term, total returns are projected to come from two primary sources:

| Return Driver | Projected Contribution |

|---|---|

| Income | ~4.0% per annum |

| Rental-growth-linked capital appreciation | ~3.1% per annum |

Yield compression will contribute modestly rather than dominate.

This income-focused return profile suits investors seeking stable, inflation-protected cash flows. That said, not every European market delivers on that profile equally — regulatory constraints can meaningfully reduce net returns in ways headline yields don't reflect.

Regulatory Risk and Return Expectations

Rent control regimes in Germany, the Netherlands, Ireland, Scotland, and Catalonia introduce uncertainty for investors. Markets with tighter regulation may see muted returns relative to headline yield figures. Investors should factor regulatory risk into entry price underwriting. The better opportunities tend to be in markets where supply constraints drive value, rather than those dependent on rent growth that legislation could cap.

Which European Markets Are Worth Watching in 2025?

Standout Opportunities

Institutional research identifies Germany and the UK as markets where rebased yields and improving mortgage conditions offer compelling entry points. Amsterdam, Madrid, Stockholm, and Copenhagen also screen well for risk-adjusted returns:

- Germany & UK — rebased yields and improving mortgage conditions

- Amsterdam — tight supply supporting price resilience

- Madrid & Barcelona — sustained demand from domestic and international buyers

- Stockholm & Copenhagen — yield normalization creating better entry conditions

Spain has been a notable exception to the European downturn — with prices rising approximately 6% per annum on average between 2002 and 2024. However, constrained supply in coastal and island regions limits transaction volumes.

Portugal: A Case Study in Structural Demand

Portugal recorded among the highest real house price appreciation in the EU since 2020, supported by:

- International buyer demand from Western Europe and the Americas

- The under-35 government mortgage guarantee scheme expanding first-time buyer access

- Strong tourism-driven rental yields

- Growing foreign investment interest

Transaction volumes rose in Q2 2025, confirming renewed momentum. For investors looking to act on that momentum, execution matters as much as market selection.

Alori International Holdings works specifically in this space — providing vetted project access, legal clarity, and defined exit strategies for investors in the $150,000–$600,000 range. The focus is on opportunities where the underlying demand is structural, not speculative.

Markets to Approach With Caution

- Ireland: Affordability constraints and persistent low supply are depressing transactions rather than prices

- Finland and Hungary: Both seeing volume declines

- Poland: Market has softened following the end of a government-subsidised mortgage scheme with no replacement yet announced

These markets aren't necessarily value traps — but without a catalyst to unlock supply or restore buyer confidence, capital deployed there faces a longer wait for return.

Frequently Asked Questions

What is the European residential real estate market outlook for 2026?

Expect continued modest price growth of around 3.5% per annum, gradual yield compression of approximately 30 basis points, and ongoing rental growth above inflation. Supply constraints will remain the dominant structural force, and investor volumes should accelerate as debt costs fall and yields stabilise.

Which European country is best to buy a house in?

Portugal, Spain (select markets), and Germany consistently rank highly for structural demand, price growth trajectory, and investment yield potential. The right choice depends on your budget, timeline, and tolerance for regulatory risk — each market carries different entry costs, rental frameworks, and foreign ownership conditions worth evaluating before committing.

How much has the European housing market risen since 2020?

EU-wide house prices rose approximately 55.4% between 2010 and 2024. Real price increases since 2020 have been particularly strong in Portugal (approximately +40.6% in real terms), Estonia, and Lithuania, driven by post-pandemic demand and supply shortfalls that continue to constrain inventory.

What happened to the European housing market in 2020?

The initial COVID-19 shock caused a brief pause — EU building permits dropped approximately 5% in 2020. The market then surged sharply in 2021, as low interest rates, increased household savings, and demand for more space drove a pan-European price acceleration that peaked in 2022 before moderating through 2023.