Introduction

Lisbon ranks 11th on PwC's 2026 European investment city list — yet it's priced far below London, Paris, or Madrid. For American investors seeking European exposure without European premium pricing, Lisbon represents an uncommon structural opportunity: strong institutional recognition paired with relative affordability.

This guide covers what makes Lisbon fundamentally attractive, how to execute a transaction as a foreigner, which neighborhoods merit attention, and what risks demand honest assessment before committing capital.

Key Takeaways

- Lisbon ranks among Europe's top real estate investment cities (PwC 2026), with prices still below other Western European capitals despite a decade of appreciation

- American buyers face no ownership restrictions but must obtain a Portuguese tax number (NIF) before purchasing

- Budget 6–10% above purchase price for transaction costs: property transfer tax (IMT), stamp duty (0.8%), notary fees, and registration

- Gross rental yields run 3–5%+ depending on neighborhood; short-term rental licenses are restricted in several historic districts

- The Golden Visa real estate route is closed to new applicants — D7 and D2 visas remain the primary residency pathways

Why Lisbon Appeals to International Investors Right Now

Portugal's economy continues to expand, supported by EU recovery fund infrastructure investments across Lisbon's metro area. The European Commission forecasts moderate growth through 2026, underpinned by tourism, technology, and foreign direct investment inflows. Each of these sectors feeds directly into Lisbon's property market.

Together, these conditions translate into four concrete factors worth examining before committing capital.

Short-Term and Long-Term Rental Demand: Lisbon welcomed approximately 8.5 million visitors in 2024, creating sustained demand for both short-term rentals in eligible zones and long-term housing from digital nomads and relocating professionals. This split between short-term visitors and longer-term residents reduces reliance on any single demand source.

Price Growth Since 2014: House prices in Lisbon rose roughly 176% between 2014 and 2024. Current average prices in the Lisbon metro sit around €6,000–€8,000/sqm, depending on neighborhood — still 30–50% below comparable districts in Paris or London. This gap represents either a value opportunity or a ceiling risk, depending on your time horizon.

Gross Rental Yields: Typical gross yields range from 3.8% in premium districts to 5%+ in residential neighborhoods. The variation reflects location, property type, and rental strategy (long-term vs. short-term). These yields compare favorably to sub-3% yields common in other Western European capitals.

Institutional Capital Signal: PwC's Emerging Trends report identifies Lisbon as an emerging hub for logistics, data centers, and energy infrastructure investment — signaling that institutional capital views Lisbon as structurally sound, not purely speculative.

Best Neighborhoods in Lisbon for Property Investment

Choosing a neighborhood in Lisbon is both a financial decision and a regulatory one. Short-term rental (AL) licensing restrictions in historic zones mean location dictates strategy as much as return potential. Choosing a neighborhood in Lisbon is both a financial decision and a regulatory one. Short-term rental (AL) licensing restrictions in historic zones mean location dictates strategy as much as return potential.

The four neighborhoods below cover the full spectrum — from premium appreciation plays to income-focused long-term rentals. Here's how they compare at a glance:

| Neighborhood | Price (€/sqm) | Approx. Yield | Primary Strategy | AL Licensing |

|---|---|---|---|---|

| Príncipe Real / Chiado | €7,725–€8,000 | ~3% | Capital appreciation | Restricted |

| Graça / Alfama | €6,400–€7,300 | ~5% | Long-term rental | Restricted |

| Estrela / Lapa | €7,250–€7,337 | 5%+ | Income / long-term | Lower risk |

| Parque das Nações | ~€6,053 | Varies | Turnkey / appreciation | Available |

Príncipe Real and Chiado

These represent Lisbon's premium residential corridor. Chiado averages approximately €7,725/sqm; Príncipe Real runs around €8,000/sqm for apartments. Yields are lower (approximately 3%), but these areas attract affluent long-term tenants and show consistent capital appreciation.

These neighborhoods suit investors prioritizing appreciation over income — capital preservation with steady, low-friction tenancy.

Graça and Alfama

Historic hilltop districts offering higher long-term rental yields (Graça approximately 5%) but restricted from issuing new short-term rental (AL) licenses due to oversaturation. Entry prices around €6,400–€7,300/sqm remain attractive.

Critical note: Verify AL licensing status before purchase if short-term rental income is part of your strategy.

Stable expat and professional tenant demand makes these districts a solid fit for long-term rental income strategies.

Estrela and Lapa

Residential neighborhoods popular with families and professionals, offering yields often exceeding 5%. Pricing has risen sharply (approximately €7,250–€7,337/sqm) but still delivers favorable income profiles relative to tourist-saturated zones.

For income-focused buyers, the combination of lower regulatory exposure and reliable tenant demand makes this one of Lisbon's more straightforward investment cases.

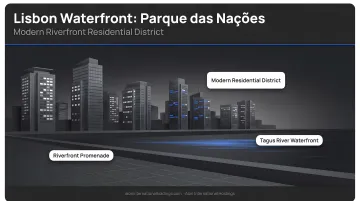

Parque das Nações and Emerging Areas

A modern waterfront district with newer construction, lower renovation risk, and strong demand from tech workers and expats. Current pricing around €6,053/sqm per recent INE data. Alcântara represents an emerging riverside area with lower entry points and an active bar and gallery scene driving foot traffic and tenant interest.

Buyers seeking turnkey properties with professional tenant demand — and room for appreciation as these zones mature — will find the strongest case here.

How to Buy Property in Lisbon as a Foreign Investor

The Portuguese property acquisition process follows a clear sequence. For American buyers specifically, skipping steps or relying on incomplete advice can mean lost deposits, unexpected tax liabilities, and delayed closings.

Step 1 — Obtain a Portuguese Tax Number (NIF)

This is non-negotiable. No property transaction in Portugal proceeds without a NIF. American buyers can obtain one through:

- A Portuguese consulate in the US

- A local tax office (Finanças) in Portugal

- A legal representative (required for non-EU residents)

Critical requirement for US citizens: You must appoint a Portuguese fiscal representative who accepts legal responsibility for tax correspondence. This can be a lawyer, accountant, or firm like Alori International Holdings with local networks established to handle this step efficiently.

Step 2 — Open a Portuguese Bank Account and Establish Proof of Funds

Most Portuguese banks require non-residents to open a local account for property transactions. You'll also need to prepare source-of-funds documentation as part of anti-money laundering compliance.

Banks differ significantly in their requirements for non-residents. Common documentation typically includes:

- Passport and NIF

- Proof of address (apostilled if issued in the US)

- Recent bank statements (typically 3–6 months)

- Source-of-funds explanation letter

Working with in-market professionals who know specific bank requirements can prevent the back-and-forth that commonly delays this step by weeks.

Step 3 — Property Search and Due Diligence

Properties are listed on portals like Idealista and Imovirtual, but off-market inventory typically requires local agent or investment firm relationships.

Due diligence in Portugal must verify:

- Debts attached to the property title itself — not the seller personally — which transfer to the buyer on completion (known as subrogated property debt)

- Clear title and ownership history

- Valid planning permissions and building licenses

- No unauthorized construction or planning irregularities

Inheritance law complication: Fragmented ownership due to Portuguese inheritance laws can delay closings if multiple heirs must consent to the sale.

Always commission independent legal due diligence. A selling agent's representations are not a substitute — your lawyer will review the land registry (Registo Predial), the tax register (Caderneta Predial), and building permits that the agent has no obligation to scrutinize on your behalf.

Step 4 — Promissory Contract (CPCV) and Deposit

Once an offer is accepted, a Contrato-Promessa de Compra e Venda (CPCV) formalizes the agreement before the final deed. This is a legally binding contract — not a letter of intent.

Key terms to understand before signing:

- Deposit: Typically 10–30% of the purchase price, paid at CPCV signing

- Buyer default: If you withdraw, you forfeit the deposit in full

- Seller default: If the seller withdraws, they must return double the deposit

- Completion timeline: Usually 30–90 days after CPCV, though this is negotiable

Have your independent lawyer review the CPCV before signing. Terms around completion deadlines, penalty clauses, and any conditions precedent (such as mortgage approval) should be negotiated at this stage, not after.