Introduction

American interest in European property has surged — from Lisbon apartments to Algarve villas — but the path from interest to closed deal looks nothing like buying at home. Each market runs on its own legal framework, tax structure, and transaction process, often with few English-language guardrails.

The challenges are consistent: choosing the right market, managing currency exposure, understanding foreign legal requirements, and knowing what to ask before signing anything.

With the right professional team, clean documentation, and a fundamentals-driven market approach, American buyers can close European property deals cleanly and avoid the costly mistakes that catch underprepared investors off guard.

TLDR: Key Takeaways

- Choose markets based on macroeconomic fundamentals and structural demand, not lifestyle appeal or trending headlines

- Get your tax identification number before making offers — it's required to complete any transaction

- Ownership legally transfers after notarized deed registration — the European notary system handles what title insurance does in the US

- Assemble your professional team before you search, not after you find a property

- Factor in Schengen stay limits, US tax reporting (FBAR/FATCA), and currency volatility before committing

Choose Your European Market Based on Fundamentals, Not Hype

Avoid Viral Listicles — Focus on Data

Choosing a market based solely on viral listicles or a single vacation experience is a costly mistake. Sound investment decisions require examining macroeconomic indicators, demographic trends, supply-demand dynamics, and regulatory frameworks — the same criteria that separate durable returns from speculative ones.

Practical Market Evaluation Checklist:

- GDP growth trajectory and economic stability

- Population migration patterns (inbound vs. outbound)

- Tourism infrastructure and international visitor trends

- Rental yield potential relative to entry price

- Long-term capital appreciation history

- Ease of exit and resale liquidity

- Regulatory environment and foreign ownership restrictions

Popular Markets vs. Emerging Opportunities

Some of the most popular "expat favorite" cities — Lisbon's historic center, Barcelona — have seen aggressive price appreciation and regulatory changes that compress returns for late entrants. For example, Portugal's 2023 Mais Habitação reform removed residential real estate from Golden Visa eligibility, reshaping the investment landscape. Under-the-radar or emerging markets often present more compelling opportunities for investors willing to look beyond headlines.

Lifestyle vs. Investment Asset Distinction

Clarify your goal upfront: Are you buying for lifestyle use or as an investment asset? This distinction drives market and property type selection, including whether short-term rental income or long-term capital growth is the primary return mechanism.

The two goals pull in different directions:

- Lifestyle buyers prioritize location appeal, climate, cultural amenities, and proximity to expat communities

- Investment buyers prioritize rental yields, capital appreciation potential, currency stability, and exit liquidity

Many American buyers conflate the two — treating a lifestyle purchase as an investment asset — and discover too late that the property underperforms financially.

Getting this distinction right early is where local market expertise pays off. Alori International Holdings applies a selective, high-conviction approach — focusing on vetted markets like Portugal and Georgia where data, fundamentals, and local networks support decisions built for the long term, not speculative short-term plays.

Navigate the Legal and Administrative Process Step by Step

Step 1: Obtain Your Local Tax Identification Number

You need a local tax identification number before any formal contract is signed — without it, the transaction cannot proceed.

Country-Specific Examples:

- Portugal's NIF (Número de Identificação Fiscal): Obtainable via a Finanças office or fiscal representative with a valid passport

- Spain's NIE (Número de Identidad de Extranjero): Form EX-15 at a Spanish consulate or police station

- Italy's Codice Fiscale: Issued by the Agenzia delle Entrate

Pro tip: Initiate this step months in advance — processing times vary, and delays here can stall the entire transaction.

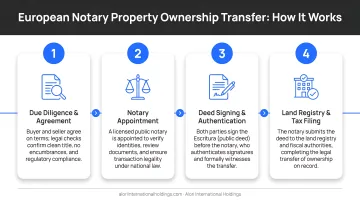

Step 2: Understand the European Notary System

Once your tax ID is in hand, the next unfamiliar piece of the process is the notary system. Unlike in the U.S., the notary here is a state-appointed neutral official — not your advocate. Their role is to:

- Verify legal ownership of the property

- Check for outstanding liens or unresolved building permit issues

- Authenticate the deed of sale

- Register the transfer in the Land Register

Ownership does not legally transfer until that registration is complete. Title insurance is uncommon in Europe precisely because the notarized system provides the legal certainty that makes it unnecessary.

Step 3: Satisfy EU Anti-Money Laundering (AML) Requirements

Under the EU's 5th and 6th Anti-Money Laundering Directives, all foreign buyers must satisfy rigorous documentation standards. Expect to provide:

- Valid passport

- Documented source of funds for the purchase

- Beneficial ownership disclosure if buying through a company

- Intended use of the property

FATF guidance confirms that real estate is a known vehicle for money laundering — which is why documentation requirements are strict and non-negotiable. Delays in providing paperwork can stall or kill a transaction entirely.

Step 4: Research Country-Specific Restrictions

Restrictions to verify before making any offer:

- Portugal: Golden Visa program no longer accepts direct residential real estate purchases after the October 2023 Mais Habitação reform (alternative routes via €500,000 investment funds still exist)

- Denmark: Restricts holiday home purchases by non-residents without special Ministry of Justice permission

- Agricultural land: Some EU countries restrict purchases by non-EU citizens

Verify current restrictions for your target country with a local lawyer before making offers.

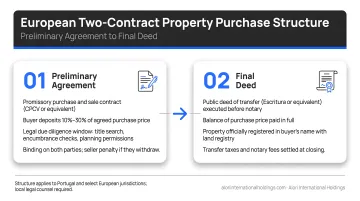

Step 5: Navigate the Two-Contract Structure

With restrictions confirmed and due diligence underway, you'll encounter one more structural difference from the U.S. process: most European transactions use a two-contract structure:

- Preliminary agreement (promissory contract): Locks in price and requires a deposit (typically 10%)

- Final notarized deed of sale: Executed weeks or months later

Pulling out after signing the preliminary contract typically means forfeiting the deposit. Due diligence must be complete before this stage — not after.

Assemble Your Professional Team Before You Start Searching

The Costly Mistake: Hiring Professionals After Falling in Love

The single most costly mistake expat buyers make is engaging professionals after they fall in love with a property — when they're emotionally committed and more likely to overlook red flags. The right team should be in place before the search begins.

Core Professionals You Need

1. Local Real Estate Lawyer (Independent from Seller's Agent)

- Specializes in transactions involving foreign buyers

- Budget roughly 1–2% of purchase price

- Reviews contracts, verifies clean title, confirms no outstanding debts or planning violations

- Represents your interests at closing

2. Local Tax Advisor

- Familiar with both local property tax law and U.S. expat reporting requirements — foreign asset disclosure, tax credits, and cross-border income rules

- Structures ownership optimally (individual vs. entity)

- Plans for ongoing tax compliance

3. Notary

- While the notary is legally neutral, having your own lawyer review notarial documents before signing is essential

- The notary authenticates the transaction but doesn't advocate for your interests

Buyer's Representative vs. Listing Agent

Once your core legal and tax advisors are engaged, consider who is actually representing your interests in the search itself. Listing agents in Europe are legally the seller's representative. A buyer-side representative with in-market access provides:

- Pricing transparency and negotiating leverage

- Access to off-market inventory

- Vetted opportunities that never hit public portals

Alori International Holdings, for example, pairs global investment analysis with in-country professionals in Portugal and Georgia who handle local due diligence, navigate regulatory requirements, and structure transactions with clear legal frameworks and defined exit strategies.

Professional Property Survey

With your team assembled, don't skip one final step before committing: a professional property survey or structural inspection, even where it isn't legally required. European resale properties frequently have undisclosed issues:

- Damp and structural settlement

- Illegal extensions or unpermitted modifications

- Building code violations

In rural or historic markets especially, that €500–€2,000 survey cost looks very small against the renovation bills that surface after closing.

Manage Financing and Currency Risk

European Mortgage Reality for Americans

Financing European property as an American is more complex than domestic purchases. Most European banks require non-resident buyers to:

- Have a local bank account

- Provide proof of income in a recognized format

- Put down 30–40% as a deposit

Typical loan-to-value ratios for non-residents in popular markets (Spain, Portugal, France) range from 60–70%. Some buyers use home equity or U.S.-based financing to avoid European mortgage complexity entirely.

Currency Risk Strategies

However you structure your financing, the currency exposure is a separate risk entirely. American buyers purchasing in euros face real volatility — a 5% swing in EUR/USD can materially change the total USD cost of your property.

Primary Currency Hedging Tools:

- Use forward contracts to lock in today's exchange rate for a future transaction date, removing USD cost uncertainty before you close

- Set limit orders to execute automatically when your target rate is reached, avoiding constant market monitoring

- Work with specialist FX brokers rather than your bank — they typically offer better rates and significantly lower transfer fees

For off-plan purchases with staged payments spread over 12–24 months, a forward contract covering each payment tranche is worth serious consideration. Rate moves of even 3–5% across a multi-payment schedule can add thousands to your final cost.

Transaction Costs Beyond Purchase Price

Budget 7–12% on top of the purchase price for all transaction costs in most Western European markets:

| Cost Category | Typical Range | Notes |

|---|---|---|

| Transfer tax | 2–10% | Varies by country and region |

| Notary fees | 1–2.5% | Regulated by law |

| Legal fees | 1–2% | Independent lawyer |

| Agent commission | 0–5% | Sometimes seller-paid, sometimes shared |

| Registration fees | 0.5–1% | Land register filing |

Know Your Residency Rights and Ongoing Ownership Costs

Schengen Area 90/180-Day Rule

Critical for American buyers: You can spend a maximum of 90 days in any 180-day period across the entire Schengen Area combined — not per country. Owning property does not grant extended stay rights.

Visa Pathways for Longer Stays:

- Portugal's D7 Passive Income Visa: For retirees and remote workers earning income from pensions, dividends, or remote employment abroad

- Spain's Non-Lucrative Visa: For those with sufficient savings or investment income — employment in Spain is not permitted

- France's Long Stay Visitor Visa: France's Long Stay Visitor Visa: For those who can demonstrate self-sufficient income and do not intend to work in France

- Portugal's Golden Visa: €500,000 investment in qualifying venture capital funds, not residential real estate (post-2023)

Ongoing Annual Ownership Costs

Property Taxes (examples):

- Portugal: IMI (Imposto Municipal sobre Imóveis) — typically 0.3–0.8% of tax value

- Spain: IBI (Impuesto sobre Bienes Inmuebles) — typically 0.4–1.1% of cadastral value

- Italy: IMU (Imposta Municipale Unica) — varies by municipality

Other Annual Costs:

- Condominium or community fees for apartments

- Building insurance

- Non-resident income tax on rental income

- Mandatory annual declarations

FBAR and FATCA Compliance for Americans

The costs above are the European side of the equation. American buyers also carry US reporting obligations that run parallel to local taxes. Foreign property-related accounts and rental income must be reported on FBAR and FATCA forms (FinCEN 114, Form 8938). Non-compliance penalties are severe — up to $10,000 per violation for non-willful failures, and higher for willful violations. Engage a U.S.-qualified expat tax advisor to ensure compliance.

Energy Performance Certificate (EPC) Requirements

EU law requires sellers to provide an Energy Performance Certificate (rated A–G) when listing a property. Factor the rating into your renovation budget and resale projections — the EU's Energy Performance of Buildings Directive mandates progressive efficiency upgrades, meaning low-rated properties could face mandatory improvement costs in the years ahead.

Frequently Asked Questions

What is the easiest European country to buy property?

Portugal and France are commonly cited as the most straightforward for non-EU buyers, with clear legal frameworks and accessible foreign ownership rights. That said, success in either market depends on having qualified local legal counsel to handle documentation, language barriers, and procedural requirements.

What is the best country in Europe to buy property?

For lifestyle and rental income, Portugal (Lisbon, Porto, Algarve), Spain, and Greece consistently rank among the top choices for expat buyers. For capital growth and lower entry points, emerging markets like Georgia offer strong fundamentals for value-focused investors.

Where in Europe is the cheapest place to buy property?

Eastern Europe and the Balkans offer some of the lowest entry prices in the region — Bulgaria, Georgia, and Bosnia all have basic apartments available for under $50,000. Even within popular markets like Italy and Portugal, secondary cities and inland areas cost significantly less than coastal or capital hotspots.

Can Americans buy property in Europe without residency?

Yes, in most European countries Americans can purchase property as non-residents. However, you're subject to the Schengen 90/180-day rule for stays, and must satisfy local tax identification and anti-money laundering requirements to complete a transaction. Ownership doesn't grant residency rights automatically.

What are the typical buying costs when purchasing property in Europe?

Budget 7–12% above the purchase price for transfer taxes, notary fees, legal fees, and registration costs. Spain and Portugal typically land around 10–12%; France falls closer to 7–8%. Exact figures vary by country and transaction structure.

Do I need a local bank account to buy property in Europe?

Most European countries require or strongly recommend a local bank account to pay taxes, transfer funds, and connect utilities. Opening one typically requires your local tax identification number, a valid passport, and proof of address.

Ready to explore curated property opportunities in Portugal or Georgia? Alori International Holdings specializes in vetted, high-conviction international real estate investments backed by local expertise and data-driven analysis. Contact us at info@aloriinternationalholdings.com to discuss your next investment.