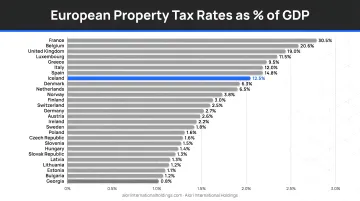

Europe has no unified property tax system. Rates, calculation methods, and exemptions vary dramatically from country to country, and sometimes from municipality to municipality within the same nation. A property in the UK can carry an annual tax burden more than 25 times higher than a comparable asset in Hungary or Czech Republic, even after adjusting for market value.

This guide covers how European property taxes work, which countries impose the heaviest and lightest burdens, which jurisdictions have eliminated annual property taxes entirely, and what all of this means for international real estate investors evaluating markets for capital preservation, rental income, and long-term appreciation.

Key Takeaways

- Europe has no single property tax system—rates range from 0% in Malta, Liechtenstein, and Cyprus to over 2.5% of private capital stock in the UK

- Property taxes generally include two categories: recurrent annual taxes on ownership and one-time transfer taxes on transactions

- Northwestern European countries (UK, France, Belgium) carry the highest property tax burdens; Eastern European and Baltic countries carry the lowest

- Annual property tax directly affects net rental yield and long-term holding costs

- Portugal's municipal property tax (IMI) runs 0.3%–0.45% for urban properties—lower than most Western European peers

How European Property Taxes Work: Key Concepts

European property taxes don't work like the US system — and for American investors, that gap matters. There are two main categories to understand: recurrent annual taxes on property ownership, and non-recurrent transfer taxes triggered when buying or selling. Most European discussions of "property tax" refer to the annual recurrent levy.

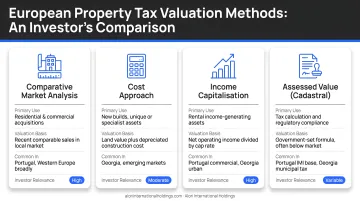

Valuation Methods

European countries use different valuation methods to calculate the tax base:

- Capital/Market Value — Used in the Netherlands (WOZ value), where tax is calculated on assessed open market value

- Rental/Imputed Rental Value — Used in France (valeur locative cadastrale), based on theoretical annual rental income

- Area-Based/Unit Approach — Common in Central and Eastern Europe (Czech Republic, Poland, Slovakia), where tax liability is based on property size rather than value

- Cadastral Value Systems — Used in Portugal (Valor Patrimonial Tributário) and Spain (valor catastral), generally set below market value

Outdated cadastral values—a common issue in Central and Eastern Europe—can make effective tax rates lower than statutory rates suggest. This creates a disconnect between nominal tax percentages and actual fiscal burden, though several countries are actively reforming their cadastral systems.

Municipal Administration

How a property is valued is only half the picture — who sets the rate matters just as much. In most European countries, property taxes are levied at the municipal level, meaning rates can differ significantly even within the same country. Local governments typically set effective rates within national bands.

In France, local assemblies vote on the rate applied to the cadastral base. In Portugal, each municipality sets its own IMI rate within the 0.3%–0.45% range for urban properties — a detail that directly affects net returns for property investors.

Approximately 20 of 27 European countries that levy property taxes allow businesses to deduct property or land taxes from corporate income tax, which has implications for investors holding assets through a legal entity.

Property Tax Rates Across Europe: A Regional Snapshot

Property tax as a share of GDP and total taxation varies dramatically across Europe. The EU average sits near 1.9% of GDP, but individual countries diverge sharply from this benchmark.

Property Tax by Country (2023 Data):

| Country | Property Tax as % of GDP | Property Tax as % of Private Capital Stock |

|---|---|---|

| United Kingdom | 3.7% | 2.570% |

| France | 3.5% | 1.134% |

| Greece | 2.5% | 1.164% |

| Germany | 0.9% | 0.233% |

| Estonia | 0.2% | 0.112% |

| Czechia | 0.2% | 0.004% |

| Hungary | 0.7% | 0.001% |

The spread between top and bottom is striking — the UK collects over 2,500 times more property tax as a share of private capital stock than Hungary, reflecting fundamentally different approaches to property as a revenue base.

Regional Patterns

These divergences reflect deeper structural differences across Europe's regions:

- Northwestern Europe (UK, France, Belgium, Netherlands) collects the highest revenues — the UK alone raised £99.7 billion in 2023 through Council Tax on residential properties and Business Rates on commercial ones.

- Southern Europe generally sits above the EU average, with Greece, Spain, and Portugal each exceeding 1.5% of GDP. Greece's ENFIA system applies a basic and supplementary component at progressive rates.

- Central and Eastern Europe, including the Baltics, typically falls well below the EU average. Area-based (rather than value-based) assessment systems and outdated cadastral values keep effective rates low. Estonia is the structural outlier — its land-only tax model removes improvements from the tax base entirely, keeping residential burdens minimal while still incentivizing productive land use.