Introduction

More Americans are buying property in Europe than at any point in the past decade — drawn by favorable exchange rates, stable legal frameworks, and markets where $200,000 still buys meaningful real estate. Most European countries allow US citizens to purchase property outright, with no citizenship or residency requirement.

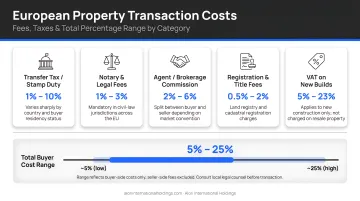

The legal right to buy, though, is only the starting point. Transaction costs alone typically run 8–12% of the purchase price — a figure many buyers discover too late. Inadequate legal counsel leads to title defects and zoning problems that surface only after closing.

Cross-border tax reporting, FATCA compliance, and local financing constraints add another layer of complexity. Understanding these obligations before you search protects your investment and your timeline.

Key Takeaways

- Americans can legally purchase property in most European countries without citizenship or residency

- The buying process takes 3–6 months and requires local professionals, a foreign tax ID, and notary completion

- Financing options include European bank mortgages, US-based international loans, or cash — non-residents typically put down 25–40%

- Property ownership does not grant residency; Americans remain subject to the 90/180-day Schengen rule

- Expect US tax reporting obligations — FBAR and FATCA apply no matter where in Europe you buy

Where Americans Can Buy Property in Europe

There is no single EU-wide rule governing foreign property purchases. Each country sets its own regulations, and most allow Americans to buy freely with minimal restrictions. The most accessible and investment-relevant markets for US buyers include Portugal, Spain, Italy, France, Greece, and Ireland—each offering distinct advantages depending on your investment objective and risk tolerance.

Most Accessible Markets for American Buyers

Portugal stands out for American investors looking to combine strong fundamentals with accessible entry points. Lisbon and Porto command €3,000–€5,000 per square meter in central districts, while the Algarve ranges from €2,500–€4,500 per sqm depending on proximity to the coast. There are no buyer restrictions for US citizens.

Portugal consistently draws long-term foreign capital through tourism revenue reaching €4.3 billion monthly, a growing expat community, and a well-established digital nomad visa pathway. Alori International Holdings focuses specifically on Portugal, identifying curated entry points backed by in-country legal vetting and defined exit strategies.

Spain runs on tourism-driven rental demand, with Barcelona and Madrid averaging €3,500–€5,500 per sqm in prime areas and Costa del Sol coastal properties coming in at €2,000–€4,000 per sqm. Short-term rental zones produce consistent yields, though local regulations on vacation rentals vary by municipality.

Italy offers the widest price spread of any major European market. Rome and Milan average €3,000–€6,000 per sqm in central districts; rural Tuscan properties can start under €1,500 per sqm. Buyers should budget carefully for renovation costs on historic properties and account for Italy's layered property tax structure.

France is the premium end of the spectrum. Paris averages €9,000–€12,000 per sqm in central arrondissements, while Provence and Côte d'Azur come in at €3,500–€7,000 per sqm. The trade-off for higher entry costs is long-term price stability in well-established markets with deep rental demand.

Greece offers the most affordable entry points in Western Europe. Athens averages €1,800–€3,000 per sqm in desirable neighborhoods, with island properties ranging from €1,500–€4,000 per sqm. The Golden Visa program—requiring a €250,000 minimum investment—adds a residency pathway for buyers thinking beyond pure yield.

Ireland is the only English-speaking market on this list, with Dublin averaging €3,500–€5,000 per sqm centrally. A persistent housing shortage drives strong rental yields—but transaction costs are among the highest in Europe, so buyers should model those into their returns.

The table below summarizes key data across all six markets at a glance:

| Market | Price Range (€/sqm) | US Buyer Restrictions | Key Consideration |

|---|---|---|---|

| Portugal | €2,500–€5,000 | None | Tourism growth, digital nomad visa |

| Spain | €2,000–€5,500 | None | Short-term rental regulation varies locally |

| Italy | €1,500–€6,000 | None | Renovation costs, complex tax structure |

| France | €3,500–€12,000 | None | High entry cost, stable long-term appreciation |

| Greece | €1,500–€3,000 | None | Golden Visa at €250K minimum |

| Ireland | €3,500–€5,000 | None | High transaction costs |

Markets Requiring Additional Scrutiny

Hungary, Poland, and Denmark impose more complex foreign buyer rules. Government approval may be required before purchase, adding 3–6 months to the transaction timeline and introducing uncertainty. Malta similarly requires government consent for non-EU buyers in certain property categories.

How to Buy Property in Europe as an American: Step by Step

Step 1: Define Your Investment or Lifestyle Objective

The right market, property type, and deal structure depend entirely on your purpose. A primary or vacation residence requires different considerations than a long-term capital appreciation play or rental income generator. Vacation homes in coastal areas may appreciate slowly but deliver lifestyle value, while urban apartments in high-demand cities offer stronger rental yields (5–10% annually) but require active management. Define your hold period, target return, and exit conditions before searching.

Step 2: Secure Financing and Set a Realistic Budget

Three main financing routes exist:

Borrow from a European bank — Most cost-effective, but non-residents face 25–40% down payments, 12 months of tax returns and bank statements, and proof of employment or business ownership. Current non-resident mortgage rates average 3.5–5.0% in Portugal, 3.0–4.5% in Spain, 3.5–5.5% in Italy, and 3.0–4.5% in France.

**Use a US bank or international lender** — Credit verification is simpler, but expect higher rates (5–7%) and loan-to-value (LTV) ratios capped at 50–70%.

Tap US assets or home equity — A HELOC or cash-out refinance sidesteps EU banking requirements, but introduces currency risk and puts domestic property on the line.

Beyond the purchase price, budget 8–12% in transaction costs covering notary fees (1–2%), transfer taxes (2–10% depending on country), agent commissions (3–6%), legal fees (1–2%), and registration costs (0.5–1%).

Step 3: Obtain a Local Tax Identification Number

Every European country requires a local tax ID before foreigners can legally buy property. Each country uses a different ID:

- Portugal: NIF (Número de Identificação Fiscal)

- Spain: NIE (Número de Identidad de Extranjero)

- Italy: Codice Fiscale

Complete this before any property search begins. Most consulates in the US can process the application, or a local lawyer can handle it when you arrive. Expect 1–4 weeks.

Step 4: Engage Local Professionals and Search for Property

Hire an independent local lawyer (separate from the notary), an English-speaking licensed real estate agent familiar with foreign buyers, and a tax advisor with cross-border US-EU expertise. Unlike the US, many European agents represent both buyer and seller, creating potential conflicts of interest — an independent lawyer protects your interests.

Property Search Options:

- Local listing portals: Immobiliare.it (Italy), Idealista (Spain/Portugal), Casa Sapo (Portugal), SeLoger (France), Spitogatos (Greece)

- International investment firms that provide access to off-market and pre-vetted opportunities, such as Alori International Holdings for Portugal-focused investments

Step 5: Sign the Preliminary Contract and Complete Due Diligence

European purchases involve two key stages: a preliminary contract (binding, typically requiring a 10–20% deposit) and the final deed signed before a notary. Due diligence must happen between these two stages and should cover:

- Title verification and ownership history

- Outstanding liens or encumbrances

- Planning permissions and zoning compliance

- Boundary surveys

- Structural inspections

- Municipal tax verification

Skipping or rushing due diligence is one of the most common — and costly — mistakes foreign buyers make. You typically lose that deposit if you withdraw after signing, even when due diligence surfaces problems.

Step 6: Complete the Sale and Register Ownership

The final deed is signed before a notary — note that the notary represents the state, not you as the buyer. Transfer remaining funds by international wire, allowing 3–5 business days for processing. Monitor exchange rates closely: USD/EUR swings can shift your final cost by thousands of dollars.

After closing, register ownership with local land authorities and set up:

- Property tax registration

- Utility accounts (water, electricity, internet)

- Rental licenses or notifications (if applicable)

- Property insurance

- Local bank account for ongoing costs

What You Need Before Buying European Property

Getting your documents, finances, and compliance obligations in order before the search begins separates smooth transactions from costly delays.

Documentation Readiness

European lenders and notaries require from US buyers:

- Valid passport

- Proof of income (minimum 12 months of tax returns and bank statements)

- Employment contract or business documentation

- Credit history report

- Proof of funds for deposit

FATCA compliance has made some European banks cautious about working with US citizens. Some UK and European banks have opted not to offer banking facilities to US citizens at all, citing the compliance burden. An experienced mortgage broker or international investment advisor can help navigate this.

Financial Readiness

Realistic capital requirements include:

- 25–40% down payment for non-residents

- 8–12% in transaction costs

- Ongoing annual costs: property taxes (0.3–1.5% of property value), maintenance (1–3% annually), property management if non-resident (8–15% of rental income)

In Portugal and Spain, opening a local bank account before applying for a mortgage typically improves approval odds. It signals financial commitment to local lenders and makes fund transfers more straightforward.

Legal and Compliance Readiness

Beyond the financials, Americans carry US tax and reporting obligations that don't disappear when buying abroad:

- Foreign property ownership itself doesn't trigger US tax

- Rental income must be reported on US tax returns (Schedule E)

- Foreign bank accounts over $10,000 require FBAR filing (FinCEN Form 114)

- Foreign assets above certain thresholds require FATCA reporting (Form 8938): $100,000 for married couples living in the US, $400,000 for couples living abroad