Introduction

European property is attracting more American capital than ever — but the financing process works nothing like it does at home. Misunderstanding it is one of the most expensive mistakes foreign buyers make.

Americans are accustomed to 20% down payments and predictable mortgage processes. European lenders typically require 25–40% deposits from non-resident buyers, scrutinize foreign income more closely, and operate under unfamiliar underwriting frameworks. Layer in language barriers, different legal systems, and currency risk, and even experienced investors can face costly delays and deal failures.

This guide covers what you need to know before committing capital:

- The main financing routes available to American buyers

- How European mortgages work in practice

- What each major market requires from foreign applicants

- Hidden costs that frequently catch buyers off guard

- How to build the right advisory team from the start

TLDR: Key Takeaways

- Americans have four financing paths: European bank mortgage, US/international loan, US asset leverage, or cash purchase

- European lenders require 25–40% down payments from non-residents — nearly double typical US requirements

- Borrowing in euros eliminates exchange-rate risk on payments, but dollar earners face exposure on asset value fluctuations

- Portugal, Spain, France, and Germany offer the most accessible paths for Americans, each with distinct documentation and rate structures

- Expat-specialized brokers, local legal counsel, and vetted investment partners improve approval odds and protect long-term returns

Why American Investors Are Financing European Property Right Now

Three macroeconomic forces are driving US capital toward European real estate: dollar strength relative to the euro, historically attractive European property valuations compared to inflated US coastal markets, and portfolio diversification away from US-concentrated risk.

According to recent data from the National Association of Realtors, American foreign property investment has grown steadily, with international real estate representing an increasingly important diversification tool for high-net-worth investors seeking exposure beyond domestic markets.

European property offers dual appeal for internationally minded investors: it serves as a long-term wealth-building asset while providing lifestyle and residency flexibility. Portugal, for example, offers investment-based residency pathways that add strategic value beyond financial returns — though these programs have evolved significantly, with property purchases no longer qualifying for the Portugal Golden Visa as of 2023.

That opportunity comes with real friction. European financing is not the standardized process American buyers are used to — and several barriers catch first-time investors off guard:

- Unfamiliar legal systems and country-specific regulations

- Mandatory local tax IDs and translated documentation requirements

- Stricter lender criteria for foreign nationals

- FATCA reporting obligations that make some European banks reluctant to work with US citizens at all

- Currency complexity adding exchange rate risk to every transaction

Navigating these obstacles requires knowing which lenders actively work with Americans, which documents to prepare before approaching a bank, and how each country's legal framework affects your ownership structure. The sections below cover exactly that.

Your Four Financing Options Explained

Option 1: Mortgage from a European Bank

The most common route for Americans buying in Europe. European banks offer competitive interest rates and local expertise, and borrowing in euros eliminates exchange-rate risk on monthly payments.

What works in your favor:

- Lower rates than US or international lenders (typically 3–4% fixed in markets like Portugal and Spain)

- Local currency borrowing removes EUR/USD payment volatility

- Lenders understand local property markets, title systems, and valuation methods

What to watch for:

- Requires extensive documentation (often translated and notarized)

- Higher down payments (25–40% vs. 20% in the US)

- Longer approval timelines due to foreign buyer scrutiny

- Some banks avoid American clients due to FATCA compliance burdens

If European banks aren't accessible, US institutions offer an alternative — with trade-offs worth understanding.

Option 2: Mortgage from a US or International Bank

Some US banks and international institutions with US ties offer foreign property loans, letting you use your existing banking relationship and US credit history.

The upside:

- Familiar banking relationship and US-based customer service

- Payments in dollars, not euros

- US credit history recognized in underwriting

The catch:

- Higher interest rates (often 1–2% above European equivalents)

- Limited lender availability — most US banks don't finance foreign collateral

- More restrictive loan-to-value ratios on international properties

- Still requires property appraisal and legal verification in the target country

For buyers who want to sidestep foreign lenders entirely, US-based assets offer a third path.

Option 3: Leveraging US-Based Assets

Using equity in a US property, securities, or retirement accounts as collateral to fund a European purchase avoids the foreign lender approval process altogether.

What works in your favor:

- No foreign lender approval required

- Dollar-denominated payments with familiar US loan structures

- Faster access to capital compared to European mortgage timelines

What to watch for:

- Puts domestic assets at risk if the European investment underperforms

- Currency exposure remains — property value in dollars fluctuates with EUR/USD rates

- May trigger tax events if liquidating securities or accessing retirement funds

Cash buyers skip all of this — but the trade-offs run in a different direction.

Option 4: All-Cash Purchase

Paying cash eliminates lender requirements, provides negotiating leverage with sellers, and avoids interest costs entirely.

The upside:

- No lender approval, documentation, or underwriting delays

- Stronger negotiating position — sellers prefer cash buyers

- No interest costs or monthly payment obligations

The catch:

- Large capital lock-up reduces liquidity

- Opportunity cost of capital not deployed elsewhere

- Requires legal due diligence before transferring funds internationally

- HSBC research emphasizes budgeting for transfer fees, legal fees, and ongoing costs beyond purchase price

Decision Framework: Which Option Suits You?

The four options serve different financial profiles. Here's how to match your situation to the right approach:

| Financing Option | Best For | Key Trade-off |

|---|---|---|

| European bank mortgage | Long-term holders wanting the lowest rates | More documentation, longer timelines |

| US/international bank loan | Buyers prioritizing familiar service and dollar payments | Rates 1–2% higher than European equivalents |

| US asset leverage | Investors with strong domestic equity needing faster access | Domestic assets at risk; currency exposure remains |

| All-cash purchase | High-net-worth buyers prioritizing simplicity and negotiating power | Large capital lock-up; full legal due diligence required |

Your income currency, target country, and timeline will likely point you toward one option quickly — but in markets like Portugal and Spain, where European bank rates remain competitive and foreign buyer programs are well-established, the local mortgage route rewards buyers who plan ahead and prepare their documentation early.

Getting a Mortgage from a European Bank: What Americans Need to Know

Documentation Requirements for Foreign Borrowers

European banks apply strict documentation standards to non-resident foreign buyers. Expect to provide:

- Valid passport

- Proof of legal residence (if applicable)

- At least 12 months of income statements or employment contracts

- Business records for self-employed buyers (typically 2-3 years)

- Several months of bank statements (usually 3-6 months)

- Local tax identification number (NIF in Portugal, NIE in Spain)

- Property appraisal or signed purchase agreement

- Proof of deposit funds and their source

US-sourced income documents often need to be translated, notarized, and sometimes apostilled (certified for international legal use) before submission.

The FATCA consideration: The Foreign Account Tax Compliance Act creates reporting obligations for foreign financial institutions that serve US citizens. Some European banks are reluctant to work with American clients due to this compliance burden. Seek lenders or specialist brokers experienced with American expat borrowers before starting the application process.

Deposits, LTV Ratios, and Eligibility

Non-residents typically face higher loan-to-value (LTV) restrictions than local buyers. In most EU countries, foreign non-resident buyers can borrow 60–75% of the property value at best, requiring a 25–40% down payment. In some countries like Italy and the Netherlands, deposits can reach 40–50%.

Several factors drive these tighter requirements:

- Foreign borrowers carry higher perceived risk due to income currency mismatch

- Legal recourse is limited if a buyer defaults from abroad

- Enforcing claims across borders adds jurisdictional complexity

Lenders assess creditworthiness based on debt-to-income ratios, stable verifiable income, and property value — similar to US underwriting. The key difference is currency risk: earning in dollars while holding a euro-denominated mortgage introduces an exposure most US underwriters never consider.

Fixed vs. Variable Rate Mortgages

Most American buyers choose between two structures:

- Fixed-rate mortgages lock in payments for the full loan term (typically 10–30 years), eliminating interest rate risk — the preferred choice for buyers managing cross-border financial complexity

- Variable-rate mortgages are often tied to Euribor and can offer lower initial costs, but introduce payment volatility; given recent European rate cycles, this carries real risk for buyers earning in dollars

The European Standardised Information Sheet (ESIS): EU law requires lenders to provide this mandatory document before finalizing any mortgage offer. The ESIS contains:

- Loan amount and duration

- Interest type (fixed/variable)

- APRC (Annual Percentage Rate of Charge)

- All costs and fees

- Early repayment conditions

Always request the ESIS from every lender you're considering. It's the only standardized document that lets you compare offers on equal terms across different banks and countries.

Once you understand what lenders are looking for, you can take concrete steps to strengthen your position before applying.

Steps to Improve Mortgage Approval Odds

Strengthen your application with these practical steps:

- Open a local bank account in the target country before applying

- Obtain the required local tax ID (NIF in Portugal, NIE in Spain) early in the process

- Prepare 12+ months of clean income documentation in the required format

- Work with a mortgage broker who has specific expat and cross-border experience and knows which lenders accept US clients

- Budget visibly for all ownership costs — taxes, notary fees, insurance — so the lender can see you understand the full financial picture

- Keep bank statements clean, with no large unexplained deposits or transfers in the months before you apply

Country-by-Country Financing Snapshot

Portugal (Alori's Key Market)

Typical mortgage conditions for non-resident Americans:

- LTV: 60–70%

- Down payment: 30–40%

- Fixed 10-year interest rates: 3–4% range

- Required documentation: Portuguese NIF tax number, local bank account, proof of income, property insurance

Portugal offers relative accessibility for non-residents with a stable, investor-friendly real estate market backed by strong tourism fundamentals. Portugal recorded €4.3 billion in monthly tourism revenue, demonstrating sustained demand that supports rental yields and capital appreciation.

Tax considerations for American buyers:

- IMI (local property tax): typically 0.3–0.45% of cadastral value annually

- Stamp duty: 0.8% on purchase price, plus 0.6% on mortgage amount if financing

- Capital gains tax and rental income taxation apply to non-residents — consult with cross-border tax advisors

Alori International Holdings works with local legal and tax professionals across Portugal's key markets. That on-the-ground network matters here — municipal regulations, rental licensing rules, and tax obligations vary by region and directly affect returns.

Beyond Portugal, financing conditions across the three other major European markets differ significantly in structure and accessibility for American buyers.

Spain, France, and Germany at a Glance

| Country | LTV | Down Payment | Avg. Rates | Key Requirements |

|---|---|---|---|---|

| Spain | 60–70% | 30–40% | 3–4.5% | NIE tax number, local account, translated income docs |

| France | 60–75% | 25–40% | 2.5–3.5% | French bank account, proof of income, property insurance |

| Germany | 60–80% | 20–40% | 2.0–3.0% | Local account, mandatory life insurance, extensive documentation |

Important notes:

- Conditions vary significantly not just by country but by individual lender and property type

- A specialist broker's role is to match your profile to the most suitable lender in each market

- France historically offers the most favorable LTV ratios for non-residents

- Germany offers the lowest rates but strictest documentation requirements

Hidden Costs and Key Risks to Budget For

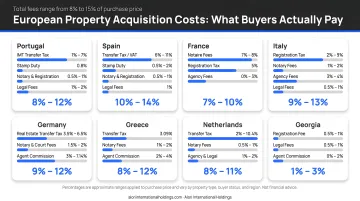

Transaction Costs That Surprise First-Time Buyers

European property acquisition costs typically add 8–12% on top of the purchase price, though regional variations can push this to 15% in markets like Spain.

Breakdown by cost category:

- Notary fees: 1–2% of purchase price

- Legal fees: 0.5–2% (critical: hire independent counsel, not the seller's lawyer)

- Property transfer taxes: Varies dramatically by country

- Portugal: 1–8% progressive (IMT)

- Spain: 6–11% regional (ITP)

- France: 5.8–6.3% (TPF, recently increased in 2025)

- Germany: 3.5–6.5% (Grunderwerbsteuer)

- VAT on new builds: 20% in France, included in purchase price

- Property valuation fees: €300–€1,000

- Stamp duties: 0.8–1.5% in Portugal and Spain

- Ongoing costs: Local property taxes (IMI in Portugal), insurance, community fees

According to Notaires de France, buyers should budget a 15% cash buffer above the purchase price to avoid shortfalls at closing.

Currency Risk: The Primary Ongoing Financial Risk

For US dollar earners holding euro-denominated property, currency risk operates on two levels:

Payment risk: Borrowing in euros fixes your monthly mortgage payment in euros, removing exchange-rate volatility from debt service entirely.

Asset value risk: The property's dollar value still moves with EUR/USD. A $500,000 purchase at EUR/USD = 1.10 could show as $450,000 on your balance sheet if the rate falls to 1.00 — even if the euro value hasn't changed.

This affects both paper wealth and realized returns upon sale. Maintaining euro-denominated reserves or holding income-producing European assets alongside the property can limit your dollar-side exposure without requiring complex hedging instruments.

Legal and Structural Risks Unique to Foreign Buyers

Title and ownership risks:

- Unclear title in some markets (particularly in countries with less digitized land registries)

- Off-plan purchase risk (developer insolvency before project completion)

- Restrictions on foreign ownership in specific property types or zones

Mitigation strategy: Independent legal counsel — separate from the developer's or seller's lawyer — should conduct full title searches and verify legal structure before any funds change hands. Foreign buyers have limited recourse once a transaction closes, so title gaps and structural defects are far cheaper to catch before signing than to litigate afterward.

Working with the Right Team to Finance European Property

The Three Essential Professionals

1. Expat mortgage broker — Identifies lenders willing to work with US citizens, navigates FATCA-related hesitancy, and advises on currency risk exposure for foreign buyers.

2. Independent local property lawyer — Not affiliated with the seller or developer. Conducts title searches, reviews purchase agreements, verifies legal structure, and represents your interests alone.

3. Cross-border financial advisor — Places the purchase within your broader US tax obligations, estate plan, and investment strategy. Essential for FATCA reporting, foreign tax credit implications, and multi-jurisdictional estate planning.

Structured, Guided Entry into European Real Estate

For investors who want professional structure around the entire process, working with a firm that integrates global investment strategy with in-country execution reduces legal risk, improves pricing accuracy, and opens access to vetted opportunities with defined exit strategies.

Alori International Holdings does this in select European markets, including Portugal. The firm combines data-driven market analysis with on-the-ground professional networks to source off-market opportunities, verify legal structures, and deliver investments with clear rental and exit strategies — built around a long-term capital mindset rather than short-term momentum plays.

Update Your Estate Plan

Acquiring European property also triggers an immediate estate planning obligation. Cross-border inheritance rules differ significantly from US law, and many countries require a locally valid will to avoid probate complications and ensure your wishes are honored.

Frequently Asked Questions

How to finance a house in Europe?

Americans have four main options:

- European bank mortgage — most common, lowest rates, higher documentation requirements

- US or international bank mortgage — simpler paperwork, typically higher rates

- US asset leverage — using home equity or other domestic assets

- Cash purchase — fastest and simplest, but ties up capital

European bank mortgages offer the best rates but require higher down payments.

What are the 2% and 7% rules in real estate?

The 2% rule (monthly rent ≥ 2% of purchase price) and 7% rule (annual gross yield benchmark) are US-originated investment filters. European markets rarely meet the 2% threshold, but capital appreciation, legal stability, and portfolio diversification often justify a different return framework.

Can Americans get a mortgage in Europe?

Yes — Americans can obtain mortgages from European banks, though they face stricter requirements and higher down payments (25–40% vs. 20% in the US). FATCA compliance makes some lenders hesitant, so working with a specialist broker experienced in expat transactions is essential.

How much deposit do you need for a European property?

Non-resident foreign buyers typically need 25–40% down in most EU countries, with some markets like Italy requiring up to 40–50%. This is well above the 20% US standard — lenders price in cross-border risk.

What is the ESIS and why does it matter?

The European Standardised Information Sheet is a mandatory document EU lenders must provide before finalizing a mortgage offer. It contains all key loan terms — including the APRC, costs, and early repayment conditions — making it the primary comparison tool when evaluating competing mortgage offers.

What are the biggest financial risks of buying property in Europe as an American?

The four main risks are:

- Currency exposure — EUR/USD swings directly affect your asset's dollar value

- FATCA hesitancy — some European lenders restrict financing for US citizens

- Higher acquisition costs — expect 8–15% upfront vs. 2–5% in the US

- Legal due diligence gaps — incomplete title or compliance checks create long-term liability

All four are manageable with the right professional team in place.