Introduction

Cross-border property ownership comes with layered tax obligations on both sides of the equation. Whether you're an American building a portfolio in Lisbon or a foreign national acquiring a New York condo, the rules are strict and the stakes are high.

The IRS expects full transparency on foreign income, and buyers of US property from foreign sellers face withholding requirements at closing that can reach 15% of the sale price — sometimes refundable, sometimes not.

This article addresses the dual reality of international real estate taxation: (1) how the US taxes Americans on their foreign property holdings, and (2) how foreign investors in US real estate are taxed under FIRPTA and related rules. By the end, you'll know what triggers a US tax event, which forms to file, and how to legally reduce your exposure.

Key Takeaways

- Owning foreign real estate alone does not trigger US tax liability—rental income, capital gains, and certain foreign financial accounts do

- Americans must report worldwide income, including foreign property profits, converted to USD at IRS-accepted exchange rates

- Foreign investors selling US real estate face 15% FIRPTA withholding at closing (10% for qualifying personal residences under $1 million)

- Key forms include Schedule E (rental income), Schedule D/Form 8949 (sales), Form 1116 (Foreign Tax Credit), and FBAR/Form 8938 when thresholds apply

- Holding periods, cost basis tracking, treaty benefits, and market selection can meaningfully reduce your total tax burden

How the US Taxes Americans Who Own Foreign Property

The US operates on citizenship-based taxation, meaning US citizens and permanent residents owe federal income tax on worldwide income regardless of where they live or earn income. The US shares this system only with Eritrea—most countries tax based on residency, not citizenship.

Purchasing or owning foreign real estate is not itself a taxable event. Tax liability arises only when the property generates income (rent) or produces a gain (sale). Related financial accounts, however, may trigger reporting obligations even without income.

The Currency Conversion Rule

All US tax calculations must be performed in US dollars, regardless of the currency of the transaction. This means the same transaction can show a loss in local currency but a taxable gain in USD — or the reverse — depending on exchange rate movement.

How conversion works:

- Purchase price is converted at the exchange rate on the date of purchase

- Improvements are converted on the date they were made

- Sale proceeds are converted on the date of sale

The IRS does not publish official exchange rates but accepts any consistently used posted exchange rate from banks, US Embassies, or the IRS "Yearly Average Currency Exchange Rates" page.

Example scenario: An investor buys a property in Portugal for €300,000 when the USD/EUR rate is 1.10 (cost basis = $330,000). Five years later, they sell for €320,000 when the rate is 1.05 (sale proceeds = $336,000). Despite only a €20,000 gain in euros, the taxable gain is $6,000—currency fluctuation added to the taxable event. Maintaining dated records of every transaction is essential.

The Primary Residence Exclusion and the Foreign Tax Credit

Section 121 Primary Residence Exclusion applies to foreign homes just as it does to US homes. Qualifying taxpayers can exclude up to $250,000 in capital gains ($500,000 for married couples filing jointly) on the sale of a principal residence, provided:

- The taxpayer owned the property for at least 2 of the 5 years before the sale

- The taxpayer used it as their primary residence for at least 2 of the 5 years before the sale

- The 24 months do not need to be consecutive

Even with the Section 121 exclusion, gains above the threshold — or properties that don't qualify — remain taxable. That's where the Foreign Tax Credit becomes relevant.

Foreign Tax Credit (Form 1116): When a taxpayer has already paid capital gains or income tax to a foreign government on the same income, they can claim a dollar-for-dollar credit against their US tax liability, preventing double taxation. Excess credits can be carried back 1 year and carried forward up to 10 years to offset future foreign-source income.

FIRPTA: What Foreign Investors in US Property Need to Know

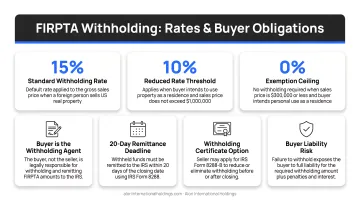

The Foreign Investment in Real Property Tax Act (FIRPTA) was enacted in 1980 to establish parity between foreign and domestic investors in US real estate. Before FIRPTA, foreign investors could sell US assets without paying US capital gains tax. FIRPTA changed this by making the buyer responsible for withholding a portion of the proceeds and remitting it to the IRS as a proxy tax.

How FIRPTA withholding works:

- The buyer (transferee) is generally required to withhold 15% of the total sale price (not just the gain) at closing

- The withheld amount is remitted to the IRS using Forms 8288 and 8288-A

- A reduced 10% rate applies when the property is sold for $1 million or less and the buyer intends to use it as a personal residence

The withheld amount is a prepayment. The foreign seller must file a US tax return (Form 1040-NR) to claim credit for the withholding and request a refund if the withheld amount exceeds their actual tax liability.

Foreign Rental Income: 30% Withholding vs. Net Election

Default rule: US-source rental income paid to nonresident aliens is subject to a 30% withholding tax on gross rental income with no deductions allowed.

IRC Section 871(d) net election: Nonresident aliens can elect to treat rental income as effectively connected with a US trade or business. This allows them to deduct expenses (mortgage interest, depreciation, property taxes, repairs, insurance) and pay graduated income tax rates on net income instead of 30% on gross.

Two forms drive this process: Form W-8 ECI is provided to the withholding agent to stop the 30% default withholding, and Form 1040-NR is filed annually to report income and claim deductions.

Foreign investors also pay the same local property taxes as domestic owners. All 50 states impose real estate taxes, with rates varying widely by jurisdiction — not FIRPTA-related, but a real ongoing ownership cost to budget for.

Understanding FIRPTA and withholding rules is essential groundwork — but tax structure is only one dimension of cross-border property investment. The legal and transactional framework of the market you're entering shapes your compliance exposure just as much.

Reporting Requirements: FBAR, FATCA, and Key IRS Forms

FBAR (FinCEN Form 114)

Required when the combined total value of all foreign financial accounts exceeds $10,000 at any point during the year. This includes bank accounts opened to purchase foreign property or collect rental income.

Key details:

- Deadline: April 15 with an automatic extension to October 15

- Foreign property itself is NOT reportable—only the financial accounts used to manage it

- Penalties: Civil penalties for non-willful violations up to $16,536 per report; willful violations carry penalties up to the greater of $165,353 or 50% of the account balance

FATCA (Form 8938)

FBAR covers financial accounts; FATCA goes further, targeting foreign financial assets above defined thresholds:

Living abroad:

- Single/Married Filing Separately: >$200,000 on the last day of the tax year or >$300,000 at any time

- Married Filing Jointly: >$400,000 on the last day or >$600,000 at any time

US residents:

- Single/Married Filing Separately: >$50,000 on the last day or >$75,000 at any time

- Married Filing Jointly: >$100,000 on the last day or >$150,000 at any time

Foreign real estate held directly in the investor's name is generally not a reportable asset under Form 8938. However, property held through a foreign corporation or trust may trigger reporting.

Penalty: $10,000 failure-to-file penalty, with additional continuation penalties up to $50,000.

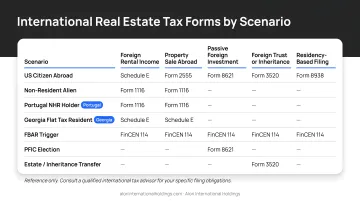

Key IRS Forms by Scenario

| Activity | Form(s) Required |

|---|---|

| Rental income and expenses | Schedule E (Form 1040) |

| Capital gains/losses from property sales | Schedule D (Form 1040), Form 8949 |

| Foreign Tax Credit | Form 1116 |

| Nonresident alien filing US return | Form 1040-NR |

| Foreign financial accounts over $10,000 | FBAR (FinCEN Form 114) |

| Foreign assets over threshold | Form 8938 |

The IRS Streamlined Filing Compliance Procedures offer a path to catch up with reduced or no penalties for investors who missed filings without willful intent.

Capital Gains Tax on Foreign Property Sales

Property held for more than one year qualifies for preferential long-term capital gains rates. Property held for one year or less is taxed as ordinary income at rates up to 37%.

2025 Long-Term Capital Gains Tax Rates

| Filing Status | 0% Rate | 15% Rate | 20% Rate |

|---|---|---|---|

| Single | $0 to $48,350 | $48,351 to $533,400 | Over $533,400 |

| Married Filing Jointly | $0 to $96,700 | $96,701 to $600,050 | Over $600,050 |

Source: IRS Rev. Proc. 2024-40

Depreciation Recapture and the NIIT Surcharge

Depreciation recapture: If the investor claimed depreciation deductions while renting the property, that portion of the gain is recaptured and taxed at a 25% rate.

3.8% Net Investment Income Tax (NIIT): Applies to high earners whose modified adjusted gross income exceeds $200,000 (single) or $250,000 (married filing jointly). These statutory thresholds are NOT adjusted for inflation.

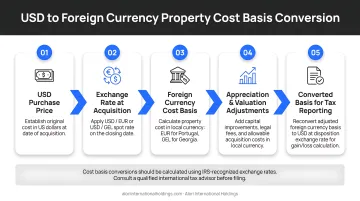

Calculating Cost Basis for Foreign Property

Once you know which rates apply, the next step is calculating the gain itself.

Formula:

Purchase price + transaction costs + capital improvements (all converted to USD at the exchange rate on the date each cost was incurred) = adjusted cost basis

Taxable gain:

Sale price (in USD at date of sale) - adjusted cost basis = taxable gain

Keep dated records of every improvement and transaction — accurate documentation is the difference between a defensible cost basis and an overpaid tax bill.

Rental Income from Foreign Property

Rental income from foreign property must be reported on Schedule E (Form 1040), just like US rental properties. The Foreign Earned Income Exclusion does NOT apply to rental income because it is passive income, not earned income—this is a common source of confusion.

Deductible Expenses

- Mortgage interest

- Property taxes paid to the foreign government

- Depreciation (foreign residential rental property is depreciated over 30 years if placed in service after December 31, 2017)

- Property management fees

- Maintenance and repairs

- Insurance

- Utilities

Beyond deductions, there's another mechanism that reduces your overall tax burden. You can apply the Foreign Tax Credit to offset US taxes owed on foreign rental income with taxes already paid to the foreign government, which prevents double taxation on the same income.

Tips to Reduce Your Tax Burden on International Property

A few targeted moves—made before you sell, not after—can meaningfully reduce what you owe on international property.

Hold for at least 12 months before selling to access long-term capital gains rates. Document all capital improvements meticulously: every renovation, upgrade, or addition increases your cost basis and directly reduces the taxable gain at sale.

Plan around the Section 121 exclusion: If the property qualifies as a primary residence, ensure the 2-year ownership and use requirements within the 5-year lookback window are met before selling. The 24 months do not need to be consecutive.

Consider the tax treaty landscape when selecting investment markets. The US has income tax treaties with several countries that reduce or eliminate withholding on certain income categories. Market selection matters here: Portugal has an active income tax treaty with the US, covering real property income and capital gains. Georgia operates under a legacy 1973 treaty with the USSR/CIS and lacks a modern bilateral agreement with the US, which can affect how income is taxed at the source.

Understanding each market's treaty status before committing capital helps avoid unexpected withholding—and shapes the overall return on a deal. Alori International Holdings focuses specifically on Portugal and Georgia, building investment structures around each country's legal and regulatory framework so the tax implications are understood from the outset.

Coordinate timing: Align foreign tax payments and US filing to maximize the Foreign Tax Credit in the same tax year. Unused credits can be carried forward for up to 10 years to offset future foreign-source income.

Frequently Asked Questions

What is the Foreign Investment in Real Property Tax Act (FIRPTA)?

FIRPTA is a 1980 US law requiring buyers of US real property from foreign persons to withhold 15% of the sale price and remit it to the IRS, ensuring foreign investors pay US capital gains tax on dispositions of US real estate.

Does the IRS impose a 50% tax on foreigners who sell U.S. real estate?

No—this is a myth. The standard FIRPTA withholding is 15% of the gross sale price, not a final 50% tax. The withheld amount is a prepayment against the seller's actual US tax liability, and any excess is refundable.

What is the capital gains tax rate for foreigners selling U.S. property?

Foreign individuals are taxed at the same long-term capital gains rates as US taxpayers taxed at the same long-term capital gains rates as US taxpayers (0%, 15%, or 20% depending on income). Foreign corporations pay the 21% federal corporate rate, plus potentially a 30% branch profits tax unless reduced by treaty.

How can I reduce U.S. capital gains tax on foreign property?

Several strategies can lower your liability:

- Hold the property more than one year to qualify for preferential long-term rates

- Maximize your cost basis by documenting all capital improvements

- Apply the Foreign Tax Credit for taxes already paid abroad

- Meet Section 121 requirements to exclude gains on a primary residence

Is foreign rental income taxable in the U.S.?

Yes—US citizens must report all foreign rental income on Schedule E. Deductible expenses—mortgage interest, depreciation, property taxes, and maintenance—significantly reduce the taxable amount. The Foreign Tax Credit then offsets any remaining US tax with foreign taxes already paid.

Do I have to report or declare foreign property or real estate to the IRS?

Foreign real estate itself does not need to be reported directly to the IRS. However, foreign financial accounts used to purchase or manage it may trigger FBAR (FinCEN Form 114) and/or FATCA (Form 8938) reporting requirements if account values exceed applicable thresholds.