Introduction

American investors face mounting pressures: domestic property prices have climbed to historically high multiples, inflation continues eroding purchasing power, and concentrated exposure to a single market means economic shocks or currency weakness can destabilize an entire portfolio.

Allocating capital to international property markets is a strategic response to these challenges — not a speculative bet. International markets offer independent economic drivers, currencies that buffer dollar weakness, and growth trajectories shaped by urbanization, tourism, and demographic shifts rather than Federal Reserve policy alone.

This article covers the four core institutional strategy types and how they apply internationally, the most effective execution approaches from buy-to-let to off-plan development, and a framework for market selection, legal structuring, and risk management.

TLDR:

- Global real estate reduces correlation with US markets and hedges inflation through independent economic drivers

- Four institutional strategies apply internationally — each matching a distinct risk tolerance and return profile

- Practical approaches include buy-to-let, capital appreciation plays, REITs, and off-plan development

- High-conviction markets combine GDP momentum, clear foreign ownership laws, and proven exit liquidity

- Legal due diligence, currency risk management, and defined exit strategies are non-negotiable

Why Global Real Estate Belongs in a Modern Wealth Strategy

Diversification Beyond Domestic Correlation

Unlike domestic real estate, international property exhibits lower correlation with US equity markets and home values. A downturn in US housing or stocks doesn't automatically erode the value of a Lisbon apartment or a Tbilisi development—these markets respond to regional employment trends, tourism flows, and local supply-demand dynamics. For investors concentrated in US assets, that regional independence is the point.

Demand for international property among American investors has grown sharply. Industry surveys consistently show high-net-worth buyers planning overseas purchases within 1–5 years, driven by recognition that single-market concentration carries real risks:

- Economic cycle exposure when domestic markets contract simultaneously

- Regulatory shifts that affect multiple US-based asset classes at once

- Market saturation in high-demand domestic metros limiting future appreciation

Inflation Hedging Through Independent Demand Drivers

International markets with younger housing stock, growing middle classes, or tourism-driven demand tend to appreciate independently of US inflation cycles. In countries like Portugal, where tourism exports exceeded €4.3 billion monthly with sustained year-over-year growth, property values rise on structural demand rather than US consumer price index movements. Over 7–10 year horizons, these markets frequently outpace domestic appreciation because they're tied to urbanization trends, infrastructure investment, and rising international visitor demand—not Federal Reserve rate decisions.

Currency and Capital Diversification

Holding hard assets in foreign currencies provides a buffer against dollar weakness. Purchasing property in euros (Portugal) or in markets with USD-denominated assets (Georgia) means rental income and eventual sale proceeds don't depend solely on USD purchasing power. If the dollar depreciates against the euro over a decade, euro-denominated rents and sale proceeds translate to higher USD returns. For investors with meaningful USD exposure elsewhere in their portfolio, that translation effect adds a layer of protection that purely domestic assets can't provide.

Lifestyle Migration and Dual-Purpose Assets

A growing segment of American investors purchase international properties that serve both as long-term investments and potential relocation or retirement options. A coastal villa in the Algarve or a Batumi beachfront apartment becomes emotionally and financially valuable—it generates rental income today while providing optionality for future lifestyle use. Even in a scenario where investment returns underperform expectations, the property retains utility — and that built-in floor changes the risk calculus for many buyers.

Due Diligence Requirements Are Higher

Global diversification requires different due diligence than domestic investing. Regulatory frameworks, property rights enforcement, currency controls, and market liquidity vary significantly by country. Portugal operates under established European Union legal standards with transparent land registries; Georgia offers rapid digital property registration but is still developing its enforcement systems.

Before committing capital internationally, investors should verify:

- Title clarity: Confirmed ownership history with no encumbrances

- Exit liquidity: Realistic resale market depth for the property type and location

- Currency controls: Restrictions on repatriating sale proceeds or rental income

- Legal framework: Whether property rights align with EU-standard protections or carry higher enforcement risk

Domestic legal assumptions don't travel. Vetting these factors before signing is non-negotiable.

The 4 Core Real Estate Investment Strategy Types

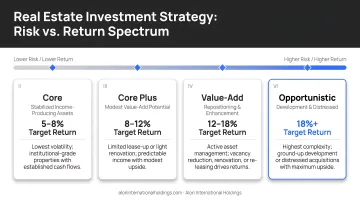

Institutional investors categorize properties by risk and return profile using four strategy types: Core, Core-Plus, Value-Add, and Opportunistic. This framework, widely used by professional allocators, applies equally well to international markets and helps investors match assets to their risk tolerance and time horizon.

Core Investments

Core investments are high-quality, well-located properties in established markets with stable long-term tenants, minimal management requirements, and predictable cash flow. Internationally, examples include fully-leased residential units in prime Lisbon neighborhoods or completed commercial properties in gateway cities.

Characteristics:

- Stabilized occupancy and lease terms

- Institutional-quality construction and location

- Low volatility and low vacancy risk

- Predictable income with modest appreciation potential

Core assets suit investors prioritizing capital preservation and steady income over high returns. The trade-off is real: returns typically run 5–7% annually, competition is intense, and premium pricing compresses entry yields. There's limited room to force appreciation — you're buying stability, not upside.

Core-Plus Investments

Core-plus assets are stable properties with minor value-enhancement potential — slightly shorter lease terms, modest deferred maintenance, or secondary-market locations with above-average growth prospects. These properties offer a balance between stability and upside.

Internationally, core-plus might be a well-maintained apartment in an emerging tourism city requiring light renovation to command higher rents. The property already generates income; tactical improvements increase cash flow or market positioning without requiring a full repositioning effort.

Characteristics:

- Stable base income with tactical enhancement opportunities

- Moderate property improvements needed (cosmetic upgrades, lease restructuring)

- Slightly higher risk than core but substantially lower than value-add

Returns typically run 7–10% annually. The existing cash flow provides a floor while improvements drive incremental upside — a useful combination for investors who want more than core delivers without taking on full renovation risk.

Value-Add Investments

Value-add properties require significant renovation, re-leasing, or operational improvement before reaching their income potential. These assets are typically underperforming due to deferred maintenance, poor management, or market repositioning opportunities.

Characteristics:

- Substantial capital improvement required

- Active management and execution risk

- Higher return potential (10–15%+ annually) through forced appreciation

- Longer hold periods to realize improvements

Executing value-add internationally adds a layer of complexity that's easy to underestimate. Success depends on reliable local contractors, project management oversight, and the ability to accurately estimate renovation costs. Capital is locked up longer, income is interrupted during construction, and legal and language barriers amplify every execution risk.

This strategy suits experienced investors who've managed renovation timelines, contractor performance, and re-leasing in domestic markets — and who understand those same challenges get harder, not easier, across languages and legal systems. Contractor delays, cost overruns, and regulatory hurdles are the norm, not the exception.

Opportunistic Investments

Opportunistic investments represent the highest risk/reward category: ground-up development, distressed acquisitions, or turnaround projects in emerging or recovering markets. Internationally, this could involve early-stage development in a market with strong demographic tailwinds — where the upside is real but entirely contingent on execution and timing.

Characteristics:

- No current income; returns depend entirely on execution and market timing

- Highest risk (capital loss possible) and highest return potential (20%+ annually)

- Extensive local expertise, networks, and market insight required

- Longer capital lock-up with no guaranteed income during development

Examples internationally:

- Off-plan purchases in pre-construction phase

- Distressed property acquisitions in recovering markets

- Ground-up development in frontier cities with rapid urbanization

This category is built for sophisticated investors with local networks, patient capital, and tolerance for all-or-nothing results. Developer failure, regulatory shifts, and market downturns during construction are live risks — and exits become especially difficult when development stalls in markets where legal recourse is still developing. The upside is real, but so is the possibility of losing the entire position.

Top Investment Approaches for Global Real Estate

The four strategy types above define the risk/return profile. The following approaches describe the practical vehicles and methods investors use to execute global real estate investments, ranging from passive to highly active. Start with whichever approach matches your capital availability, risk tolerance, and desired level of involvement.

Buy-to-Let: Long-Term Rental Income Abroad

Buy-to-let involves purchasing a residential or commercial property in an international market and leasing it to long-term tenants. In markets like Portugal, strong rental demand from digital nomads, students, expats, and corporate executives creates a consistent tenant base.

Key considerations:

- Research gross rental yields in your target market — many Portuguese and Georgian markets deliver 5–10% annually

- Map seasonal demand patterns and typical vacancy rates before projecting income

- Review landlord-tenant laws, since lease terms, eviction procedures, and tenant protections vary significantly by country

- Budget for local property management, which handles maintenance, tenant screening, and regulatory compliance remotely

Price range: Typically the most accessible entry point for American investors, with quality properties available in the $150K–$400K range in Portugal and $100K–$250K in Georgia.

For investors prioritizing growth over yield, the next approach trades near-term income for long-term value capture.

Direct Property Purchase for Capital Appreciation

This strategy prioritizes capital appreciation over near-term yield. Investors purchase property in a high-growth market and hold for 5–10 years to capture value expansion driven by urbanization, infrastructure investment, and rising international demand.

Signals that make a market attractive:

- Population shifting from rural areas to cities, compressing urban housing supply

- New airports, highways, rail connections, or port expansions unlocking previously underserved areas

- Rising international visitor arrivals and tourism revenue signaling demand growth

- Growing foreign buyer activity indicating that outside capital has validated the market

Georgia offers an example: entry prices remain comparatively low relative to long-term growth potential, with consistent above-regional GDP growth, expanding infrastructure, and rising international capital inflows.

Strategy: Purchase in emerging neighborhoods or secondary cities ahead of major infrastructure completion. Hold through appreciation cycles and exit when the market matures.

Where direct ownership requires active market selection and long hold periods, REITs and funds offer a more passive path in — explored next.

International REITs and Real Estate Funds

Investors can gain exposure to international real estate through globally-traded Real Estate Investment Trusts (REITs) or international real estate funds without directly owning property.

Advantages:

- Exit positions easily since REITs trade on public exchanges like stocks

- Spread risk across multiple geographies and property types within a single fund

- Delegate all operational decisions to experienced fund managers

Trade-offs:

- No control over which assets are selected, when to enter, or when to exit

- Fund fees and broad diversification trim the outperformance you'd capture through direct ownership in a well-chosen market

- REITs tend to move with equity markets more than physical property does, reducing the diversification benefit

Suited for: Investors seeking international real estate exposure without operational responsibilities or those testing a market before committing to direct ownership.

For investors willing to accept more risk in exchange for maximum price advantage, off-plan purchases take the approach one step further.

Off-Plan and Pre-Development Property

Off-plan investment means purchasing a unit during the planning or construction phase at below-market pricing in exchange for accepting delivery risk and a longer time to income.

Structure:

- Entry prices typically run 15–30% below completed market value

- Staged payment plans spread capital outlay over 12–48 months

- Some developers offer guaranteed buyback options or rental guarantees as added incentives

Markets: Select international markets where developers offer structured payment plans and project financing. Portugal (Algarve, Lisbon coast) and Georgia (Batumi, Tbilisi) have active off-plan pipelines.

Due diligence essentials:

- Audit the developer's past completions, delivery timelines, and financial stability before committing

- Verify land ownership, permits, and zoning approvals — legal title must be clean before any capital moves

- Check on-time completion rates across prior projects, not just marketing claims

- Confirm that payments are held in escrow and released only when construction milestones are met

Risks: Developer failure, construction delays, cost overruns, and market downturns during development. Markets with maturing property rights enforcement amplify these risks — legal recourse is slower and less predictable. Skipping developer due diligence is where most off-plan losses originate.

How to Identify High-Conviction International Markets

High-conviction markets are distinguished by durable macroeconomic fundamentals and structural demand drivers—not short-term momentum or speculative hype.

Key indicators:

- GDP growth trajectory: Consistent above-regional growth signals economic health

- Demographic trends: Young or growing populations create housing demand

- Tourism and migration inflows: Rising international visitors and expat communities drive rental demand and property values

- Infrastructure investment pipelines: New airports, highways, and urban development projects unlock value

- Property rights stability: Clear legal frameworks for foreign buyers and enforceable contracts

These indicators become even more meaningful when paired with capital flow analysis. Markets where foreign direct investment is growing, currency stability supports long-term planning, and exit liquidity exists—meaning a functioning secondary market for resale—are fundamentally different from frontier markets where entry is easy but exit is uncertain.

Spreading capital thinly across many geographies dilutes expertise and increases execution risk. Alori International Holdings applies a concentrated approach, focusing exclusively on select high-conviction markets such as Portugal and Georgia. That concentration enables access to off-market opportunities, verified legal structures, and the in-country professional networks that generalist investors rarely replicate on their own.

Legal and Structural Considerations for Cross-Border Investing

Foreign Ownership and Transaction Procedures

American investors must navigate distinct ownership rules and closing procedures in each market.

Portugal:

- Ownership rights: Foreigners may purchase residential and commercial property directly

- NIF requirement: A Portuguese Tax Identification Number must be obtained before purchase

- Notary role: Mandatory. Final deed (Escritura Pública de Compra e Venda) executed before a notary who verifies transaction legality

- Habitation License: Sellers must present a Licença de Utilização to prove legal compliance

- Registry timeframe: Registration requested within 30 days; processing typically 5–10 working days

Georgia:

- Ownership rights: Foreigners enjoy unrestricted rights to buy residential and commercial property

- Agricultural land restriction: Foreigners are strictly prohibited from purchasing agricultural land

- Registration timeframe: Ownership registered rapidly, typically 1–4 days through National Agency of Public Registry

- Notary role: Optional unless language barriers require certified translation

- Registration tax: 157 GEL for secondary housing, 308 GEL for new builds

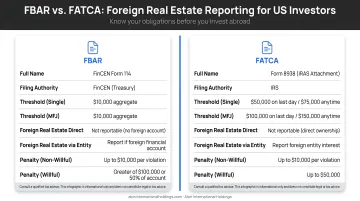

US Tax Obligations: FBAR and FATCA

Once the transaction closes, US investors face a separate layer of compliance. FinCEN and IRS reporting requirements apply regardless of where the property is held.

Critical distinction: Direct real estate held by US individuals is NOT reportable on FinCEN Form 114 (FBAR) or IRS Form 8938 (FATCA). However, if real estate is held through a foreign entity, the entity itself becomes a specified foreign financial asset and must be reported.

Foreign bank accounts used to collect rental income ARE reportable under FBAR if the aggregate value exceeds $10,000 at any time during the calendar year.

Form 8938 (FATCA) thresholds vary by residency:

- Unmarried in US: >$50,000 at year-end or >$75,000 anytime

- Married abroad: >$400,000 at year-end or >$600,000 anytime

Tax Treaties and Double Taxation

Tax treaties determine which country has primary taxing rights on real estate income and capital gains.

- Portugal: The US-Portugal income tax treaty grants Portugal primary taxing rights on rental income and capital gains. The US allows a foreign tax credit for taxes paid to Portugal to prevent double taxation.

- Georgia: The US does not currently maintain an active income tax treaty with Georgia. Investors rely on standard foreign tax credit provisions under domestic law to offset Georgian taxes.

IRS Treatment of Foreign Rental Income

Foreign rental income is reported on Schedule E (Form 1040), Part I alongside domestic rental income. Key filing details:

- Deductions: Property management fees, maintenance, mortgage interest, and depreciation are all allowable

- Depreciation: Calculated on Form 4562 and entered on line 18 of Schedule E

Given the complexity of Portugal's treaty provisions and Georgia's no-treaty status, work with a cross-border tax advisor alongside local legal professionals — the structuring decisions made at purchase directly affect your long-term tax exposure.

Key Risks of Global Real Estate Investing and How to Manage Them

Currency Risk

The value of rental income and eventual sale proceeds in USD terms depends on exchange rate movements over the hold period. If you purchase a €300,000 property in Portugal and the euro weakens 20% against the dollar over five years, your USD-denominated return suffers even if the property appreciates in euro terms.

Management strategies:

- Diversify currency exposure across multiple markets

- Consider USD-denominated assets in markets like Georgia

- Underwrite scenarios with currency depreciation to stress-test returns

- Accept currency risk as part of international diversification rather than attempting to hedge small positions

Legal and Title Risk

Property rights enforcement and transparency vary widely. In Portugal, established EU legal standards and transparent land registries provide strong protection. In Georgia, rapid digital registration improves transparency, but enforcement mechanisms are still maturing compared to Western European standards.

Management strategies:

- Engage local attorneys to verify title and ownership rights before closing

- Review land registry records and confirm no liens or encumbrances exist

- Understand local legal recourse procedures if disputes arise

- Work with firms that maintain vetted legal networks in target markets

Liquidity Risk

In smaller or less mature markets, selling property quickly at fair value can be difficult, especially during economic downturns. Exit liquidity (the ability to find a buyer and close within a reasonable timeframe) varies significantly by market and property type.

Management strategies:

- Focus on markets with active secondary markets and foreign buyer demand

- Avoid highly illiquid markets or property types with limited buyer pools

- Underwrite longer hold periods (7–10 years) to reduce forced sale risk

- Define clear exit strategies before entry (resale to local buyer, resale to foreign investor, conversion to short-term rental)

Operational and Management Risk

Managing a rental property from thousands of miles away without a trusted local property manager exposes investors to tenant issues, maintenance neglect, and regulatory non-compliance.

Management strategies:

- Engage professional property management before purchase

- Verify manager credentials, tenant screening processes, and maintenance protocols

- Establish clear reporting cadences and performance metrics

- Build relationships with in-country professionals who understand local regulations, cultural norms, and transaction processes

In-country professionals are not a convenience — they are structural to protecting returns. Local expertise closes the gap between signing a contract and actually managing an asset across borders.

Exit Strategy Definition

Risk management doesn't end once you've mitigated currency, legal, and operational exposure. The final layer is planning how you get out. Each acquisition should include at least two viable exit paths, validated before you commit capital.

Example exit paths:

- Resale to local buyer in active secondary market

- Resale to foreign investor through international networks

- Conversion to short-term rental if long-term rental demand weakens

- Redevelopment or repositioning if market conditions change

Markets that lack active secondary demand or foreign buyer interest should trigger serious scrutiny before you invest — not after.

Frequently Asked Questions

What are the 4 strategies for real estate investment?

The four institutional real estate strategies are Core, Core-Plus, Value-Add, and Opportunistic. Core investments prioritize stability and predictable income in established markets. Core-Plus adds modest value-enhancement opportunities while maintaining base cash flow. Value-Add requires significant renovation or repositioning for higher returns. Opportunistic investments involve ground-up development or distressed acquisitions with the highest risk and return potential.

What is the best country to invest in real estate internationally?

There is no universal "best" country—the right market depends on your goals, budget, and risk tolerance. Stable markets with transparent legal frameworks, foreign ownership rights, and clear exit liquidity consistently attract long-term capital. Portugal offers established EU legal protections and strong tourism demand; Georgia provides lower entry pricing and frontier growth potential.

How do Americans buy property abroad?

The core steps are: engage a local attorney to verify title, structure ownership through a direct purchase or local LLC, and meet US tax reporting requirements (FBAR, FATCA). Closing procedures, documentation, and registry processes vary significantly by country, making local legal expertise essential at every stage.

What are the biggest risks of investing in international real estate?

The primary risks are currency fluctuation eroding USD returns, title uncertainty in less mature legal systems, operational complexity of remote property management, and thin exit liquidity in smaller markets. Thorough legal due diligence and validating resale demand before entry are the most effective ways to manage these exposures.

How much money do I need to start investing in international real estate?

Entry points vary by market. Georgia offers well-located properties in the $100K–$200K range, while Portugal typically starts higher given its EU standing and demand profile. The $150K–$600K range covers a broad spectrum of quality international opportunities across both markets.

Is international real estate a good hedge against inflation?

International real estate can hedge inflation effectively when the market has structural demand drivers—urbanization, tourism growth, demographic expansion—and the asset generates rental income that rises with local price levels. The key caveat: currency risk must be managed, since exchange rate movements can offset inflation-hedging benefits if the local currency weakens against the dollar.