Two critical decisions define success: navigating foreign legal and financial systems that work fundamentally differently from US protocols, and identifying markets where fundamentals—not hype—support long-term capital growth.

This guide covers why Americans are drawn to overseas property, the five critical factors you must evaluate before committing capital, US tax and legal obligations that apply regardless of location, and how to choose a market with conviction rather than speculation.

Key Takeaways

- US citizens can legally purchase property in most countries, but ownership restrictions vary significantly by jurisdiction

- Five factors determine success: ownership laws, market stability, financing structure, legal due diligence, and exit strategy

- American buyers carry ongoing IRS obligations: rental income reporting, capital gains tax on sale, and FBAR filing for foreign accounts over $10,000

- Plan to work with both a local attorney and a US-based tax advisor — skipping either creates real exposure

- Markets with underlying structural demand — population growth, housing shortfall, economic diversification — consistently outperform tourism-driven speculation

Why Americans Are Buying Property Overseas

American buyers are looking beyond US borders for four distinct reasons:

- Retirement lifestyle — lower cost of living, favorable climate, and a slower pace

- Portfolio diversification — hard assets outside US markets that hold value through inflation

- Rental income — passive cash flow in markets with stronger yield potential

- Lifestyle migration — the freedom to relocate that remote work has made genuinely possible

The economic context makes this trend concrete. US house prices rose 1.8% year-over-year in Q4 2025, driving 16% of US realtors to report clients seeking foreign property—up from 9% the previous year, according to the National Association of Realtors. Remote work permanence reinforces this shift: 75% of employed adults with remote-capable jobs work remotely at least some of the time, creating location flexibility that didn't exist five years ago.

That location flexibility also translates into real purchasing power. Dollar strength amplifies what American buyers can afford abroad: the USD/EUR exchange rate stood at 1.15 in April 2026, while the Georgian Lari traded at 2.69 to the dollar. For buyers in the $150,000–$600,000 range, markets like Portugal and Georgia offer entry points that simply don't exist domestically.

Lifestyle versus investment purchases require different criteria. A retirement home prioritizes climate, healthcare access, and community. A pure investment property demands rental yield analysis, resale liquidity, and an honest look at currency risk. The due diligence process looks different depending on which goal you're pursuing — and conflating the two is one of the most common mistakes first-time international buyers make.

Key Factors to Consider Before Buying Property Overseas

Buying property overseas involves five interconnected decisions — legal standing, financing structure, market fundamentals, ownership form, and exit strategy — each of which directly affects returns and risk exposure.

Foreign Ownership Restrictions and Residency Rules

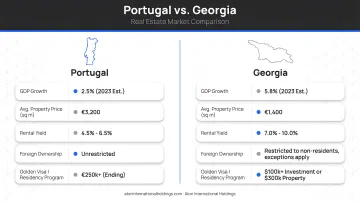

Not all countries grant US citizens the same ownership rights. Portugal offers unrestricted freehold ownership to foreigners for residential property without restrictions. Mexico requires a 50-year fideicomiso (bank trust) for coastal properties within 50km of the ocean or 100km of borders, according to the Mexican Consulate. The Philippines caps foreign ownership at 40% of any condominium project, with foreigners constitutionally barred from owning land.

Georgia allows foreigners to purchase non-agricultural land, apartments, and commercial property freely, but strictly prohibits foreign ownership of agricultural land. New Zealand restricts overseas buyers from purchasing residential land to live in without explicit government consent.

Some countries tie property ownership to residency or Golden Visa programs, particularly in Europe. Portugal's Golden Visa now requires €500,000 in qualifying investment funds; real estate no longer qualifies post-2023. Investors should evaluate whether residency access is a goal or a complication. Local legal structures (domestic LLCs, holding companies) are often used to navigate restrictions, but trigger additional US reporting obligations.

Property Market Fundamentals and Political Stability

A property's value ultimately depends on the country's economic health, demographic trends, capital flows, and political stability. Structural demand comes from population growth, urbanization, tourism infrastructure, and foreign investment inflows, not speculative price increases driven by momentum.

Key market indicators for the two most active markets for US buyers in this range:

| Indicator | Portugal | Georgia |

|---|---|---|

| GDP Growth (2024) | 2.1% | 9.7% |

| Inflation (2024) | Moderate | 1.1% |

| Tourist Arrivals (2024) | 31.6 million | High growth |

| Transparency International Rank | 46th (56/100) | 56th (50/100) |

Both scores indicate moderate institutional quality. Governance gaps make local legal counsel essential, not optional.

Financing Options and Currency Risk

Three main financing paths exist for Americans buying overseas:

- US bank or international lender offering overseas mortgage products (rare, limited availability)

- Local bank mortgage in the purchase country (typically 60–70% loan-to-value for non-residents, requiring 30–40% down payments)

- Cash purchase using home equity release or liquid capital

Portuguese banks cap non-resident LTVs at 60–70% with interest rates around 4.7% variable or 3.9% with associated sales. Georgian banks offer similar LTV caps with interest rates of 10.7% for GEL-denominated loans, 7.5% for USD, and 6.4% for EUR. Many high-net-worth buyers pay cash entirely.

Currency risk deserves careful modeling. If the USD weakens against the local currency after purchase, the effective cost of the property rises. Properties purchased in volatile currencies can depreciate in USD terms even when local prices increase. Conversely, dollar strength creates buying opportunities — USD strength against the Euro and Georgian Lari in 2025–2026 improved American purchasing power materially.

Legal Due Diligence and Ownership Structure

Title verification is the single most critical step. Unlike the US, many countries lack centralized multiple listing services or standardized title insurance. Title insurance does not exist in Portugal — buyers rely entirely on the Notarial system (Escritura Pública) and Land Registry verification. Georgia uses the National Agency of Public Registry (NAPR) for centralized registration, processing transactions in one day.

Purchasing property with undisclosed encumbrances, ownership disputes, or unpaid taxes is possible without proper verification. A local, independent attorney — one with no referral relationship to the agent or developer — is essential. Their job is to protect your interest exclusively.

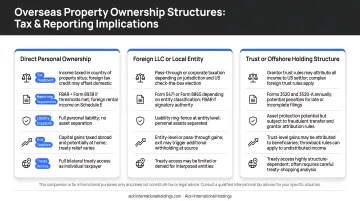

Common ownership structures include personal name, domestic LLC, or foreign holding corporation. Each has implications for local tax treatment and US reporting obligations. Owning a foreign corporation triggers additional IRS forms (5471, 8938), creating compliance burdens that must be managed proactively.

Exit Strategy and Rental Potential

Many buyers enter overseas markets without a defined exit plan, creating illiquidity risk. A viable exit strategy requires:

- Clear resale market with active buyer demand

- Absence of capital controls that restrict repatriation of funds

- Realistic liquidity timeline (typically 6–18 months in developed markets)

Evaluate rental potential as both an income tool and exit-validation mechanism. Key metrics include occupancy rates, legal short-term rental permissions in the specific municipality, property management availability, and whether comparable properties generate consistent yield. Some cities restrict short-term rentals (Airbnb-type), materially affecting rental income projections. Portugal and Georgia generally permit short-term rentals, but municipal regulations vary.

Legal, Tax, and Financial Essentials for US Buyers

The US taxes its citizens on worldwide income. Buying overseas does not remove American tax obligations. Even if a property sits in Portugal or Georgia, the IRS still has a claim on income earned and gains realized. Knowing which forms apply—and when—keeps you compliant without surprises.

IRS Reporting on Rental Income

Rental income from foreign property must be reported on Form 1040, Schedule E. Deductible expenses typically include maintenance, management fees, insurance, and depreciation. The IRS depreciates foreign real estate over 30 years under the Alternative Depreciation System (ADS)—not the 27.5 years used for US residential property—reducing annual deduction amounts. Foreign taxes paid on rental income may qualify for the Foreign Tax Credit via Form 1116.

Capital Gains on Sale

Sale of foreign property triggers US capital gains tax reporting via Form 8949 and Schedule D. Owners who lived in and owned the property for at least two of the previous five years may exclude up to $250,000 in gains ($500,000 married filing jointly). Pure investment properties face full capital gains rates. Local transfer taxes—typically 1–10% of sale price—are a separate obligation in the purchase country. Portugal's Municipal Property Transfer Tax (IMT) scales up to 7.5% for non-primary residences valued over €1,150,853.

FBAR and FATCA Thresholds

If a foreign bank account exceeds $10,000 at any time during the calendar year, FinCEN Form 114 (FBAR) must be filed. Form 8938 is required under FATCA if specified foreign assets exceed $200,000 on the last day of the tax year (or $300,000 at any time) for unmarried taxpayers living abroad. Married couples filing jointly abroad face thresholds of $400,000/$600,000. Owning a foreign corporation to hold property triggers further filing obligations.

Estate Planning Implications

A US will or revocable trust generally does not automatically govern foreign property. Many civil law countries—including Portugal, Italy, and Mexico—have forced heirship provisions requiring a percentage of the estate to pass to specified family members regardless of what the will says.

A cross-border estate planning attorney can assess whether a local will, international will, or alternative ownership structure is the right fit for the specific country.

Estate planning is one piece of a larger compliance picture. Three professional engagements should run concurrently throughout any overseas purchase:

- A local attorney in the purchase country to handle title, contracts, and jurisdiction-specific requirements

- A US tax advisor experienced with international property to manage IRS reporting and foreign tax credits

- A financial advisor who can model currency exposure, liquidity, and portfolio-level impact

How Alori International Holdings Can Help

Alori International Holdings takes a different approach to overseas real estate than a typical broker or marketplace. Rather than offering a broad menu of international listings, Alori focuses on a small number of high-conviction markets—currently Portugal and Georgia—where macroeconomic indicators, demographic trends, capital flows, and regulatory frameworks have been analyzed to support long-term capital growth.

The firm's integrated model combines global investment strategy with in-country execution through local professionals who understand regulatory nuances, transaction processes, and off-market opportunities. Buyers access vetted projects with verified legal structures and defined exit strategies.

This focus directly addresses the primary risks American buyers face overseas: legal exposure, pricing opacity, and unclear liquidity paths.

Core differentiators for overseas buyers include:

- Disciplined entry points based on structural demand, not momentum

- Curated opportunities with pre-verified legal structures and exit planning built in

- Access to off-market deals through local networks

- Transparent pricing backed by market data, not listing-agent estimates

- Investment structures designed for patient, long-term capital — not short-term flips

For investors weighing overseas property as part of a broader portfolio or lifestyle strategy, Alori offers an initial consultation to walk through current opportunities and market fundamentals. Reach out at info@aloriinternationalholdings.com to get started.

Conclusion

Buying property overseas is achievable and strategically sound for the right investor. Success depends on disciplined market selection, thorough legal and tax preparation, and a clear definition of goals — lifestyle, income, or capital growth — before committing.

The goal is not to find the most talked-about overseas market, but the one where fundamentals align with your timeline, risk tolerance, and return expectations. Overseas property is a long-term asset. The investors who do the work upfront — on legal structure, market selection, and exit strategy — are the ones positioned to hold through cycles and exit on their terms.

A firm like Alori International Holdings takes exactly this approach: fewer markets, deeper conviction, and vetted opportunities in places like Portugal and Georgia where the fundamentals have been stress-tested rather than assumed.

The checklist for getting this right is consistent across every market:

- Define your goal (yield, growth, residency, or lifestyle) before selecting a location

- Verify legal ownership structures and foreign buyer restrictions early

- Engage a local attorney independent of the seller

- Understand tax obligations in both the host country and your home country

- Build in a realistic exit strategy before you buy

Frequently Asked Questions

Can US citizens buy property overseas?

Yes, US citizens can purchase property in most countries. However, some countries impose foreign ownership restrictions, require permits, or limit the types of property foreigners can hold—making country-specific legal research essential before committing.

Is it hard to buy a house overseas?

The process is more complex than a domestic US purchase due to unfamiliar legal systems, fragmented listing markets, and language barriers. With the right local attorney, a knowledgeable US advisor, and a clear understanding of the target country's rules, it's entirely manageable.

What US taxes and reporting requirements apply to buying property overseas?

Rental income must be reported on Schedule E, capital gains on sale reported via Form 8949, foreign bank accounts over $10,000 require FBAR filing, and FATCA thresholds may require Form 8938. The purchase itself does not need to be declared to the IRS.

Is it worth investing in overseas property?

Overseas property can be an effective tool for portfolio diversification, inflation protection, and passive income. Returns depend on selecting markets based on structural fundamentals, understanding the legal and tax framework upfront, and having a defined exit strategy before you buy.

What is the best country for US citizens to buy property?

The right market depends on your goals, budget, and risk tolerance — there is no universal answer. That said, countries like Portugal and Georgia have attracted growing US buyer interest due to favorable property rights, residency programs, and strong long-term fundamentals.

Can an LLC buy property in another country?

In many countries, foreigners use a local LLC or domestic holding structure to purchase property — particularly where direct foreign ownership is restricted. Owning a foreign corporation triggers additional US reporting requirements, so professional legal and tax advice is essential before choosing this structure.