Introduction

The US ranks among the highest property-taxed nations in the developed world — a fact that surprises most investors conditioned to think of Europe as the high-tax destination. According to Tax Foundation data, the US extracts approximately 1.81% of its private capital stock through property taxes, compared to a European average of just 0.41%.

This gap has direct consequences for real estate investors evaluating cross-border property purchases. Property tax isn't a one-time closing cost — it's a recurring annual holding expense that impacts rental yield, net cash flow, and long-term ROI.

For investors comparing a $300,000 property in New Jersey (1.88% effective rate) versus Portugal (0.44%), the difference amounts to roughly $4,800 annually — money that either compounds in your portfolio or disappears into local tax coffers.

This article examines how US and European property tax systems are structured, compares annual rates and one-time transaction costs side-by-side, and identifies which European markets offer the most compelling tax efficiency for long-term buy-and-hold investors.

Key Takeaways

- US property tax burden (~1.81% of private capital stock) is over 4x higher than Europe's average (~0.41%)

- US rates vary dramatically by state—from under 0.3% in Hawaii to nearly 2% in New Jersey and Illinois

- Many European countries levy minimal annual property taxes; Malta and Liechtenstein charge zero

- Higher upfront costs in Europe—stamp duty, transfer taxes—mean total cost analysis matters more than annual rate alone

- For long-term investors, lower European annual rates can significantly boost net rental income and overall returns

US vs. Europe Property Tax: Quick Comparison

Annual property tax rates at a glance

United States:

- Range: 0.29% (Hawaii) to 1.88% (New Jersey/Illinois)

- National average: ~1.0-1.2% of assessed value

- Set by counties and municipalities based on local budget needs

Europe (sample countries):

- Malta: 0% annual property tax

- Germany: ~0.23% of private capital stock

- Portugal: ~0.44% of private capital stock

- France: ~1.13% of private capital stock

- UK: ~2.57% of private capital stock (highest in Europe, comparable to high-tax US states)

Source: Tax Foundation 2025 data

Who sets the rate and how

In the US: Property taxes are determined by local governments—counties, cities, school districts—each setting their own rates based on annual budget requirements. Your home is assessed by a local appraisal board, and the tax is calculated as a percentage (mill rate) of that assessed value. Two identical homes in different counties can carry vastly different annual tax bills.

In Europe: Tax structures vary dramatically by country. Some nations set rates nationally; others delegate to municipalities. Assessment methods differ just as much — most countries use a percentage-of-value approach, but Croatia and Greece charge fixed per-square-meter fees regardless of what the property is actually worth.

One-time transaction costs

Annual holding costs tell only part of the story. Entry costs work in the opposite direction:

- US transfer taxes: Range from 0% to 4% depending on state and city, with some high-value markets adding luxury surcharges (New York's mansion tax, LA's Measure ULA)

- European stamp duties and transfer taxes: Commonly 5-10% of purchase price

Examples:

- Greece: 3% transfer tax

- Malta: 5% stamp duty

- Portugal: Progressive IMT transfer tax reaching up to 8% on secondary residences

Europe's lower annual holding costs can be erased by higher entry costs — particularly on shorter hold periods. Investors should model total cost of ownership across their full intended hold, not just day one.

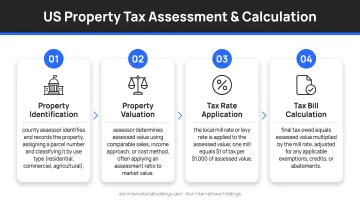

How Property Taxes Work in the US

The fundamentals

US property tax is an annual levy on real property assessed by local government, funding schools, police, fire departments, and roads. According to OECD Revenue Statistics, it accounts for approximately 11% of total US tax revenue — well above the OECD average of 5.1%. Nearly all of it is collected at the state and local level, making this one of the most decentralized tax systems in the developed world.

How rates are calculated

The process:

- A local appraisal board determines your property's assessed value, typically based on recent comparable sales

- The local government sets a mill rate (tax rate per $1,000 of assessed value) based on budget requirements

- You receive an annual statement showing assessed value × mill rate = tax owed

- If you dispute the valuation, you can file an appeal with comparable sales data and property evidence

Extreme state-level variation

Property tax burdens vary dramatically across states:

Highest rates:

- New Jersey: 1.88% effective rate

- Illinois: 1.88%

- Connecticut: ~1.7%

Lowest rates:

- Hawaii: 0.29%

- Alabama: 0.37%

- Louisiana: ~0.52%

This variation means a $400,000 home in New Jersey costs $7,520 annually in property tax, while the same-priced property in Hawaii costs just $1,160. That $6,360 annual gap adds up significantly over a 10-year hold.

Annual taxes are only part of the picture. US buyers also face one-time transfer taxes at closing, and those costs vary just as widely by location.

One-time purchase costs

Beyond annual taxes, US buyers face transfer taxes at closing:

- California: $1.10 per $1,000 base rate, plus severe local overlays in markets like Los Angeles (Measure ULA adds 4-5.5% on sales over $5.3M)

- New York: 1% mansion tax on purchases above $1M, with NYC adding progressive surcharges up to 2.9% on properties over $2M

- Florida: $0.70 per $100 statewide ($0.60 in Miami-Dade for single-family homes)

Tax implications for rental investors

Rental income from US property carries several tax obligations worth understanding before you invest:

- Rental income is taxed as ordinary income at federal rates of 10-37%, plus applicable state income tax

- Deductible expenses include mortgage interest, property management, maintenance, depreciation, and property taxes themselves

- Foreign owners face FIRPTA withholding — buyers must withhold 15% of sale proceeds when foreign nationals sell US real estate

How Property Taxes Work in Europe

The European approach

Unlike the US's relatively uniform percentage-of-value model, European countries each set their own property tax structures—creating dramatic variation across the continent. According to Tax Foundation analysis, the European average across 27 countries with property taxes is approximately 0.41% of private capital stock, compared to the US at 1.81%.

Country-by-country variation

European property tax burdens range from zero to US-comparable levels:

Highest in Europe:

- UK: ~2.57% (comparable to high-tax US states)

- France: ~1.13%

- Greece: ~1.16%

Mid-range:

- Portugal: ~0.44%

- Spain: ~0.67%

- Netherlands: ~0.46%

Lowest:

- Germany: ~0.23%

- Bulgaria: ~0.19%

- Malta: 0% (no annual property tax)

- Liechtenstein: 0% (no annual property tax)

20 of 27 European countries allow businesses to deduct property taxes from corporate income — reducing the net burden for investors holding through entities.

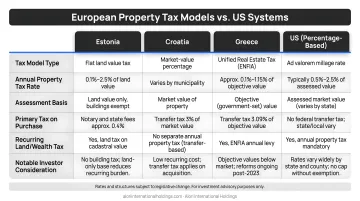

Structural differences from the US

European property taxation operates under distinct models:

- Estonia: Taxes only land value, excluding buildings—creating an efficient, non-distortionary system

- Croatia: Charges €0.60 to €8.00 per square meter of usable area, regardless of property value

- Greece: Uses the ENFIA system with rates of €2 to €16.20 per square meter, adjusted by location and age

- Some countries exempt primary residences: Croatia exempts permanent residents from annual property tax on their primary home

A percentage-of-value system means your tax bill rises with appreciation; a per-square-meter system keeps costs predictable regardless of market swings.

European transaction costs

While annual rates run low, entry costs run high:

- Portugal: Progressive IMT transfer tax reaching 7.5% for properties above €1.1M

- Greece: 3% transfer tax on taxable value

- Malta: 5% stamp duty

- Spain: 6-10% transfer tax in most regions

These upfront costs require careful modeling. A property with 0.4% annual tax but 7% entry cost needs to be held at least 8-10 years to break even against a market with 1% annual tax but 1% entry cost.

Rental income and capital gains taxation

Beyond entry costs, ongoing income and exit taxes shape the total return picture. Rental income is taxed in most European countries, with rates varying widely:

- Portugal: 28% flat rate for non-residents

- Greece: 15-45% progressive rates

- Georgia: 5% flat rate (country-specific)

Capital gains: Treatment varies significantly:

- Greece: Exempting CGT on properties sold before December 2026 under current policy

- Portugal: 28% flat rate for non-residents on 50% of gains

- Georgia: 0% if held over two years

US investors should note that double-taxation treaties with most European countries prevent double taxation on the same income — but treaty terms vary by country, so verifying coverage before investing is essential.

What Property Tax Differences Mean for Real Estate Investors

Modeling true cost of ownership

Let's compare a hypothetical $300,000 property across two markets:

Scenario A: High-tax US state (New Jersey at 1.88%)

- Annual property tax: $5,640

- 10-year holding cost: $56,400

- Transfer tax at purchase: ~$1,200 (0.4%)

- Total 10-year tax burden: $57,600

Scenario B: Low-tax European market (Portugal at 0.44%)

- Annual property tax: $1,320

- 10-year holding cost: $13,200

- Transfer tax at purchase: ~$18,000 (6% IMT)

- Total 10-year tax burden: $31,200

Net difference: $26,400 over 10 years, or $2,640 annually—regardless of property appreciation. This $220/month difference flows directly to net cash flow or compounds as reinvested capital.

Impact on rental yield

Lower annual property taxes directly improve net rental yield:

Example: $300,000 property generating $18,000 annual rent (6% gross yield)

US scenario (1.88% property tax):

- Gross rent: $18,000

- Property tax: -$5,640

- Net rent (before other expenses): $12,360

- Property tax consumes 31% of gross rental income

Portugal scenario (0.44% property tax):

- Gross rent: $18,000

- Property tax: -$1,320

- Net rent (before other expenses): $16,680

- Property tax consumes 7% of gross rental income

For investors targeting 5-7% gross rental yields, a 1-2% annual property tax can absorb 15-40% of gross income. Tax efficiency isn't a rounding error—it's one of the largest controllable variables in actual net return.

Transaction cost trade-off and hold period

European markets with low annual rates but higher entry costs favor longer hold periods. The "break-even horizon" concept calculates when lower annual costs outweigh higher upfront transaction costs.

Break-even formula:

(European transfer tax − US transfer tax) ÷ (US annual property tax − European annual property tax) = Years to break even

Using our $300,000 example:

($18,000 − $1,200) ÷ ($5,640 − $1,320) = 3.9 years

After four years, Portugal's lower annual tax fully offsets its higher entry cost. By year 10, the cumulative tax savings exceed $26,000—capital that stays in the investment rather than flowing to the state.

US reporting obligations for international property owners

Before committing capital abroad, American investors need to understand their US reporting obligations. The compliance layer is manageable—but it must be planned for upfront:

FATCA (Form 8938): Direct ownership of foreign real estate is NOT reportable. However, if held through a foreign entity, the entity interest is reportable.

FBAR (FinCEN 114): Foreign bank accounts exceeding $10,000 at any time require reporting. This includes rental collection accounts.

Double-taxation treaties: The US maintains tax treaties with Portugal and most European nations, helping prevent dual taxation on rental income. Consult a cross-border tax professional to structure foreign tax credits and apply treaty provisions correctly.

European Markets with Favorable Property Tax for American Investors

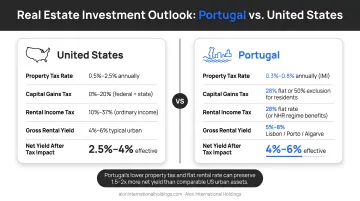

Portugal: Low holding costs, strong fundamentals

| Tax / Cost | Rate |

|---|---|

| Annual property tax (IMI) | 0.3–0.45% (urban residential) |

| Property Transfer Tax (IMT) | Progressive, up to 7.5% for secondary residences above €1.1M |

| AIMI wealth tax | 0.7% on combined property values exceeding €600,000 |

Tax regime changes: Portugal's Non-Habitual Resident (NHR) regime was revoked for new entrants in 2024 and replaced by IFICI, which restricts the 20% flat tax rate strictly to highly qualified professionals, researchers, and startup founders. Broad expat tax holidays are no longer available — model rental income at standard non-resident rates.

Investment markets: Lisbon, Porto, and the Algarve offer strong rental demand driven by tourism growth, with gross rental yields typically in the 5–10% range. Portugal's tourism sector consistently posts record numbers, creating sustained demand for short-term and seasonal rentals.

Key advantage: Annual holding costs of 0.3–0.45% keep Portugal competitive for buy-and-hold strategies even after the NHR changes — net yield projections should now factor standard non-resident income tax rather than the prior flat rate.

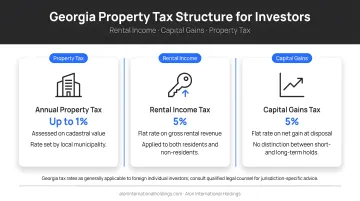

Georgia: Ultra-low tax environment with high yields

| Tax | Rate |

|---|---|

| Annual property tax | 0.05–1% (based on household income; often 0% for foreign investors without Georgian-sourced income) |

| Rental income tax | 5% flat rate on gross residential rental income |

| Capital gains tax | 0% after two years of ownership |

Market performance: Tbilisi delivered average gross rental yields of 9.0% in Q1 2025, with the residential property price index rising 11.53% year-over-year.

Entry pricing: Buy-and-hold opportunities typically fall in the $100,000–$300,000 range, making Georgia accessible for mid-level investors seeking international diversification.

The three-part tax structure above — zero property tax, 5% rental income, and 0% capital gains after two years — compounds meaningfully over a 5–10 year hold, particularly at the $150,000–$300,000 entry points common in Tbilisi.

Note: The US and Georgia do not have a modern bilateral tax treaty; they rely on a 1973 treaty signed with the USSR. Consult a cross-border tax professional for US tax treatment of Georgian rental income.

Alori International Holdings works with American investors navigating acquisition, legal structuring, and market entry in Portugal and Georgia. Reach the team directly at info@aloriinternationalholdings.com to review current opportunities.

Conclusion

The US has notably higher ongoing property taxes than most of Europe—but the right choice for any investor depends on intended hold period, rental strategy, currency exposure, and compliance complexity. A market with 0.4% annual property tax and 7% transfer tax may still outperform a low-transfer-cost US market over a 10-year hold, purely through the compounding effect of lower annual carrying costs.

That compounding dynamic is why property tax belongs in the return model from day one—not just as a purchase-day line item. Investors who account for three recurring variables upfront tend to make sharper entry and exit decisions:

- Annual tax burden — the true carrying cost that compounds across every year of the hold

- Rental income taxation — how the local regime treats yield, including withholding and treaty treatment

- Capital gains treatment — exit tax exposure, holding period thresholds, and any exemptions available

Getting these right from the outset is what separates an accurate return projection from a misleading one.

Frequently Asked Questions

Are property taxes higher in Europe or the USA?

The US property tax burden (measured at ~1.81% of private capital stock) is significantly higher than the European average (~0.41%). The UK is the notable European exception, with rates around 2.57%—comparable to high-tax US states like New Jersey and Illinois.

How high are property taxes in Europe?

European property taxes range from zero (Malta, Liechtenstein) to approximately 2.57% in the UK. Most countries fall well below 1%, with the European average across countries levying the tax sitting at approximately 0.41% of private capital stock.

Do other countries have property taxes like the US?

Most developed countries have some form of property tax, but few match the US in rate or reliance. The US generates approximately 11% of total tax revenue from property taxes versus a 5.1% OECD average, and its decentralized system is more complex than most European equivalents.

What European countries have the lowest property taxes?

Malta and Liechtenstein levy zero annual property tax. Other low-tax countries include Germany (0.23%), Bulgaria (0.19%), and Portugal (0.44%). These countries often offset low annual rates with higher one-time purchase taxes or transaction levies.

How does property tax work for foreign investors in Portugal?

Portugal levies an annual IMI tax of 0.3–0.45% on urban residential property, plus a one-time IMT transfer tax at purchase. Foreign investors pay the same rates as residents, and the US-Portugal double-taxation treaty limits dual taxation on rental income.

What should American investors know before buying property in Europe?

US citizens must report foreign property income to the IRS regardless of where they live. Double-taxation treaties reduce dual-taxation risk. Model total cost of ownership—including annual property tax, rental income tax, transaction costs, and currency exposure—across your full intended hold period before investing.