Introduction

Portugal has become one of Europe's most active destinations for cross-border property investment, with American investors representing a growing share of cross-border property buyers. Capital appreciation and rental yields draw investors in — but capital gains tax (CGT) is often what determines the actual return at exit.

Portugal's CGT framework is not a single flat rate. It shifts based on residency status, asset type, holding period, and whether reinvestment conditions are met. A non-resident selling a Lisbon apartment faces fundamentally different tax treatment than a resident disposing of an inherited property held since 1985. A retiree reinvesting proceeds into a qualifying pension product faces a different calculation still.

This article breaks down how CGT is structured in Portugal, what rates apply to whom, which exemptions are available, and what strategies investors can use to protect their returns before they finalize a purchase or plan an exit.

Key Takeaways

- Portugal's standard CGT rate is 28%, but residents pay tax on only 50% of real estate gains at progressive rates (13–48%)

- Since January 2023, non-residents are taxed on the same 50% inclusion basis as residents on Portuguese real estate gains

- Primary residence sales may qualify for full CGT exemption if proceeds are reinvested in another qualifying home within 36 months

- US investors must navigate the US-Portugal tax treaty, which includes credit mechanisms to prevent double taxation on the same gain

- Crypto held over one year is tax-exempt; securities held for 8+ years qualify for a 30% exclusion

What Is Capital Gains Tax in Portugal?

Capital Gains Tax in Portugal, known as mais-valias, is a tax on profit realized from the disposal of capital assets. It is governed under Portugal's Personal Income Tax Code (Código do IRS), specifically Articles 10 (defining capital gains), 43 (calculation and inclusion rules), and 51 (deductible expenses). The Autoridade Tributária e Aduaneira (AT) administers these rules.

When CGT Is Triggered

A CGT event occurs at the moment of sale or transfer of an asset. Portugal's tax year runs January to December. Filings (Modelo 3) are due between April 1 and June 30 of the following year. Missing this window triggers penalties and interest charges, so factoring the reporting calendar into your exit timeline matters.

Worldwide vs. Portuguese-Sourced Income

Your residency status determines the scope of your tax exposure:

- Tax residents are taxed on worldwide income — gains from assets anywhere in the world fall under Portuguese CGT.

- Non-residents are taxed only on Portuguese-sourced assets, such as property in Portugal or shares in Portuguese companies.

For American investors acquiring Portuguese property, establishing or maintaining the right residency classification before a sale can meaningfully affect your final tax bill.

CGT Rates by Residency Status: What Applies to You

The same asset can attract different effective tax rates depending solely on the seller's residency classification. Where you establish residency before a sale directly shapes your effective tax rate.

Tax Residents

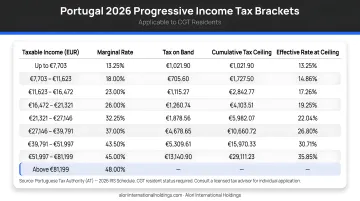

Residents are taxed on 50% of the net real estate gain, which is then added to total annual income and taxed at Portugal's progressive income tax rates. For 2026, these rates range from 12.50% to 48%:

| Taxable Income (€) | Marginal Tax Rate |

|---|---|

| Up to 8,342 | 12.50% |

| 8,342–12,587 | 15.70% |

| 12,587–17,838 | 21.20% |

| 17,838–23,089 | 24.10% |

| 23,089–29,397 | 31.10% |

| 29,397–43,090 | 34.90% |

| 43,090–46,566 | 43.10% |

| 46,566–86,634 | 44.60% |

| Over 86,634 | 48.00% |

Election option: If total income exceeds €86,634, taxpayers may elect a flat 28% rate instead of progressive rates. For lower earners, the progressive route is typically more favorable.

Non-Residents

The January 2023 rule change (Lei n.º 24-D/2022) significantly changed how non-residents are taxed. Previously, non-residents paid a flat 28% on the full gain. Now, they are taxed on the same 50% inclusion basis as residents, subject to progressive rates.

Critical nuance: Even though only Portuguese property is taxed, the non-resident's worldwide income determines the applicable marginal rate. A high-earning US investor may face Portugal's top 48% rate on the taxable portion of their gain — even with no other Portuguese income.

Non-Habitual Residents (NHR)

NHR status does not grant automatic exemption from CGT on Portuguese assets. While NHR holders may benefit from exemptions on certain foreign-sourced income under applicable double tax treaties, Portuguese property gains remain taxable under standard rules. The NHR 2.0 reforms (IFICI regime) introduced in 2024 have limited impact on CGT treatment for domestic real estate.

US Investors: The Tax Treaty Dimension

The US-Portugal Double Taxation Agreement (DTA), signed in 1994, determines how gains are allocated between the two countries. Under Article 14, Portugal retains primary taxing rights over immovable property located within its borders — meaning Portuguese real estate gains are taxed in Portugal first.

Foreign tax credit mechanism: The US allows taxpayers to claim a foreign tax credit under IRC §901 for income taxes paid to Portugal, reducing US tax liability dollar-for-dollar up to the amount of US tax owed on the same income. This prevents the gain from being fully taxed in both countries, though careful planning is required to maximize the credit and avoid timing mismatches.

Which Assets Are Subject to CGT in Portugal?

Not all assets are taxed identically. The rate and method of taxation varies by asset class, and some assets are fully exempt.

Real Estate

Gains on directly owned Portuguese property are subject to the 50% inclusion rule for both residents and non-residents (post-2023). Two rules catch investors by surprise:

- Properties acquired before January 1, 1989 (when the CIRS entered into force) are fully exempt from CGT

- If a property was used for short-term rental income as a business activity (for example, Alojamento Local), 95% of the gain is taxable — unless the owner ceased business activity at least 36 months before the sale. This rule, sometimes called the "85/15 rule," catches many short-term rental operators off guard

Stocks, Securities, and Investment Funds

Gains from shares, bonds, corporate securities, and mutual fund units are taxed at a flat taxed at a flat 28%. However, the 2024 capital markets reform (Lei n.º 31/2024) introduced long-term holding exclusions:

| Holding Period | Exclusion Rate |

|---|---|

| 2–5 years | 10% |

| 5–8 years | 20% |

| 8+ years | 30% |

The exclusions apply to listed securities and open-ended investment fund units. Gains from assets in blacklisted jurisdictions (for example, Gibraltar, Guernsey) are taxed at an aggravated 35% rate.

Crypto Assets

Crypto assets became subject to CGT on January 1, 2023:

- Held less than one year: Taxed at 28%

- Held more than one year: Fully exempt

Exempt and Non-Taxable Assets

The following fall outside CGT scope:

- Personal possessions

- Assets held in qualifying tax-free savings structures

- Inherited property (subject only to 0.8% stamp duty at transfer)

- Pre-1989 assets

Note: Subsequent sale of inherited property does trigger CGT, calculated from the inherited value (the value used for stamp duty purposes).

How to Calculate Your Capital Gains Tax in Portugal

Knowing your CGT exposure before you sell gives you time to plan — whether that means timing the sale, reinvesting proceeds, or structuring the transaction more efficiently. The four steps below walk through how Portugal calculates the tax.

Step 1: Determine Net Gain

Net gain = Sale price − Acquisition cost − Deductible expenses

Acquisition cost includes:

- Original purchase price

- Purchase taxes (IMT, stamp duty)

- Legal fees paid at acquisition

- Notary fees

Deductible expenses include:

- Renovation costs (last 12 years)

- Estate agent fees

- Documented improvement works

Critical requirement: All expenses must be supported by valid invoices containing the property owner's NIF (Tax Identification Number) and clearly linked to the specific property. Generic material purchases without proof of application the AT routinely rejects.

Step 2: Apply the 50% Inclusion Rule (for Real Estate)

Only half the net gain is subject to tax. For properties held more than 24 months, an inflation adjustment (monetary correction coefficient) may further reduce the taxable base.

Step 3: Apply the Correct Rate

- Progressive income tax rates (13–48%) based on total annual income

- Flat 28% election available if total income exceeds €86,634 (the top bracket threshold)

- Mandatory aggregation rule from 2023 for securities held less than 365 days where total income reaches or exceeds €86,634

Worked Example

Scenario:

- Purchase price: €250,000

- Sale price: €400,000

- Documented renovation costs: €20,000

- Holding period: 5 years (resident taxpayer)

Calculation:

- Gross gain: €400,000 − €250,000 = €150,000

- Net gain: €150,000 − €20,000 = €130,000

- Taxable gain (50% inclusion): €130,000 × 50% = €65,000

- Tax due: €65,000 added to annual income, taxed at marginal rates

With €30,000 in other income, the total rises to €95,000, pushing the gain into higher progressive brackets. Here's how the two tax approaches compare:

| Tax Method | Rate Applied | Estimated Tax on €65,000 |

|---|---|---|

| Progressive rates | 35–40% (effective) | €22,750–€26,000 |

| Flat rate election (28%) | 28% flat | €18,200 |

| Potential savings | €4,550–€7,800 |

The flat rate election is available here because total income exceeds €86,634. For many investors in this income range, electing the flat rate produces a meaningfully lower tax bill.

Exemptions and Reliefs That Can Reduce Your CGT

Several exemptions can significantly reduce — or eliminate — your CGT liability in Portugal. Each comes with specific conditions, so understanding the criteria before you sell is essential.

Primary Residence Rollover Relief

Full CGT exemption is available if:

- The property was the taxpayer's primary residence in the 12 months preceding sale

- The full proceeds (net of outstanding mortgage on the sold property) are reinvested in a new primary residence in Portugal or any EU/EEA country with a tax treaty with Portugal

- Reinvestment occurs within 36 months of sale (or within 24 months prior to sale)

- The owner moves in within 6 months of the reinvestment deadline

Post-Brexit note: The UK no longer qualifies.

Retirement-Age Reinvestment Relief

Taxpayers who are retired or aged 65+ can exempt gains from a primary residence sale by reinvesting proceeds into an eligible life insurance policy or pension fund within 6 months. Unlike the rollover relief, partial reinvestment still qualifies — meaning you don't need to commit the full sale amount. This relief can also be combined with the rollover relief, which makes it particularly useful for those downsizing in retirement.

Other Exemptions and Offsets

Beyond the two primary reliefs, several additional rules can reduce your taxable position:

- Assets acquired before January 1989 are fully exempt from CGT

- Capital losses can be offset against gains and carried forward for up to five years

- Double Taxation Agreement (DTA) credits apply when gains are already taxed in another jurisdiction, preventing double taxation

- On jointly owned properties, splitting renovation invoices equally between owners maximizes allowable deductions on each partner's tax return

Taken together, these exemptions reward long-term ownership, retirement planning, and careful documentation — all factors worth structuring for before a sale rather than after.

Tax Planning Strategies for International Property Investors

CGT exposure in Portugal is shaped by decisions made before, during, and after a property is held. The right planning moves — on timing, structure, and treaty use — can meaningfully reduce what you owe.

Timing the Sale Relative to Residency Status

Consider whether selling during the NHR term (when foreign-sourced income may be exempt) or after becoming a full tax resident (when the 50% inclusion rule applies) is more favorable. Exiting Portugal before the sale may also reduce exposure if you return to a lower-tax jurisdiction.

Structuring Investments Through Tax-Efficient Vehicles

Qualifying Portuguese investment funds may offer different tax treatment than direct property ownership. For example, income distributed by Portuguese real estate funds is subject to a 28% withholding tax (or 10% for non-residents under specific conditions), and fund structures may allow for reinvestment without triggering immediate CGT.

Applying DTA Provisions

Confirm whether the source country or Portugal has primary taxation rights under the applicable treaty. For US investors, Article 14 of the US-Portugal DTA gives Portugal primary rights over real estate, but the foreign tax credit mechanism ensures gains are not taxed twice.

Key steps when working with DTA provisions:

- Verify which country holds primary taxation rights under your specific treaty

- Confirm the foreign tax credit mechanism applies to avoid double taxation

- Time the sale to optimize credit utilization across both jurisdictions

- Work with a cross-border tax advisor to ensure credits are claimed correctly

Modeling Exit Economics Before You Buy

CGT implications are most useful when factored in before acquisition, not after. Knowing your likely tax position at exit — based on residency status, holding period, and applicable treaty — lets you evaluate whether projected returns actually hold up net of tax.

Firms like Alori International Holdings build this analysis into the pre-acquisition process, pairing local Portugal market knowledge with defined exit strategies and verified legal structures so investors understand total return potential from the outset.

Frequently Asked Questions

How much is capital gains tax on property in Portugal?

Residents pay CGT on 50% of the net real estate gain at progressive rates (13–48%) or optionally at a flat 28%. Non-residents (post-2023) are taxed on the same 50% basis at progressive rates, with worldwide income used to determine the marginal rate.

Is there any capital gains tax in Portugal?

Yes, Portugal levies CGT on profits from the sale of real estate, shares, securities, investment funds, and crypto held for less than one year. The flat rate is 28% for most investment assets, with real estate subject to the 50% inclusion rule.

Are capital gains taxable for non-residents in Portugal?

Since January 2023, non-residents are taxed on the same basis as residents on Portuguese real estate — 50% of the gain at progressive marginal rates. Shares and securities gains remain subject to the 28% flat rate.

Does Portugal tax US capital gains?

Under the US-Portugal Double Taxation Agreement, Portugal taxes gains on Portuguese-situated assets (like real estate), while foreign tax credit provisions prevent the same gain from being fully taxed twice. A cross-border tax advisor can clarify how this applies to your situation.

What makes you exempt from capital gains tax in Portugal?

Key exemptions include full reinvestment of primary residence proceeds into a qualifying home within 36 months, retirement-age reinvestment into an eligible pension or insurance product, ownership of assets acquired before 1989, and crypto held for more than one year.

What is the 85 15 rule in Portugal?

This rule applies to properties previously used for business or rental income. If a property generated business income (such as short-term rentals), 95% of the capital gain is taxable — not the standard 50% — unless the business activity ceased at least 36 months before the sale. A Portuguese tax advisor can help you navigate this before structuring your exit.