Introduction

Portugal remains one of the most compelling destinations for American property investors in 2025—stable market, accessible pricing, and rental yields typically between 5–10% annually. But the tax landscape just became more complex. A new law enacted in December 2025 introduces a flat 7.5% property transfer tax (IMT) for all non-resident buyers, replacing the progressive scale that previously allowed many mid-market buyers to pay 2–4% or less.

That shift has real consequences for buyers in the $150,000–$600,000 range—and understanding it before you sign anything is non-negotiable. This guide walks through every tax you'll face from purchase through sale, how to structure rental income efficiently, and which exemptions can help you sidestep the new flat rate entirely.

TLDR: Key Takeaways for Non-Resident Buyers in 2025

- A flat 7.5% IMT now applies to all non-resident residential purchases — up from the previous 0–8% progressive scale

- The 7.5% rate can be avoided by becoming a tax resident within two years or renting long-term at moderate rents (€2,300/month or below)

- Annual IMI (property tax) runs 0.3–0.5% for urban properties; AIMI wealth tax applies above €600,000 in total property value

- Non-residents pay 25% tax on rental income and 28% on capital gains from sale

- The US-Portugal tax treaty prevents double taxation through foreign tax credits on your US return

The Full Tax Picture: What Non-Residents Pay on Portuguese Property

Residency status matters for some taxes but not all. Spending 183+ days per year in Portugal makes you a tax resident, which lowers your rental income and capital gains tax rates. Either way, you owe Portuguese taxes on all property-related transactions regardless of where you live.

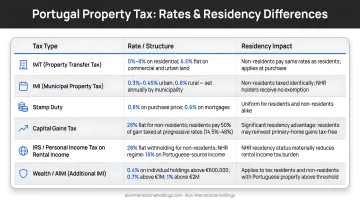

Summary of Portugal Property Taxes:

| Tax Type | Rate | When It Applies | Resident vs. Non-Resident Difference |

|---|---|---|---|

| IMT (Transfer Tax) | 7.5% flat | At purchase | Non-residents pay flat rate; residents use progressive scale |

| Stamp Duty | 0.8% | At purchase | No difference |

| IMI (Annual Property Tax) | 0.3–0.5% urban / 0.8% rural | Annually | No difference |

| AIMI (Wealth Tax) | 0.7–1.5% | Annually on properties >€600K | No difference |

| Rental Income Tax | 25% flat | On rental income | Residents pay 14.5–48% progressive |

| Capital Gains Tax | 28% flat | On property sale | Residents pay progressive rate on 50% of gain |

NIF: Your First Step Before Any Purchase

You must obtain a NIF (Número de Identificação Fiscal) before completing any property transaction. Non-EU citizens, including Americans, apply through a Portuguese tax representative — typically a lawyer, accountant, or a trusted local contact with Portuguese residency or citizenship.

Regional Variations: Madeira and the Azores

Portugal's tax structure is largely uniform across the mainland. The exceptions are Madeira and the Azores, which offer approximately 30% reductions on IMI rates and more favorable IMT brackets — worth factoring in if you're evaluating those markets.

Tax Year and Filing Deadlines

The tax year runs January 1–December 31. Annual returns are filed April 1–June 30 the following year through the Portuguese Tax Authority's online portal (Portal das Finanças).

Property Purchase Taxes: IMT, Stamp Duty, and the 2025 Legislative Change

IMT (Property Transfer Tax)

IMT (Imposto Municipal sobre a Transmissão Onerosa de Imóveis) is a one-time tax paid before signing the final deed.

For Non-Residents (2025 onward):

- Flat 7.5% rate on all residential property purchases

- Rural properties: 5%

- Commercial properties: 6.5%

For Residents (Progressive Scale Still Applies):

| Property Value | IMT Rate |

|---|---|

| Up to €97,064 | 0% |

| €97,064 – €137,997 | 2% |

| €137,997 – €190,159 | 5% |

| €190,159 – €317,500 | 7% |

| €317,500 – €632,839 | 8% |

| Over €632,839 | 6% on portion above |

Stamp Duty

A flat 0.8% applies to the transaction value and is collected at the notary. If you use a mortgage, additional stamp duty applies to the loan:

- 0.6% for repayment terms over 5 years

- 0.5% for shorter terms

The 2025 Legislative Change: Flat 7.5% IMT for Non-Residents

Portugal's "Construir Portugal" housing package (Law 73-A/2025, December 2025) established this flat 7.5% rate, which now applies to all non-resident residential purchases.

Strategic Exemptions

You can avoid the 7.5% rate if:

- You become a Portuguese tax resident within two years of purchase

- You place the property on the long-term rental market within six months at rents within the moderate ceiling (€2,300/month) and keep it rented for at least 36 months within the first five years

If you paid the flat 7.5% rate but later qualify for an exemption, Portugal's Tax Authority (Autoridade Tributária) refunds the difference.

Impact on American Investors

Buyers purchasing properties in the €140,000–€370,000 range face the sharpest increase — this is where the progressive scale previously delivered the lowest effective rates. Whether you purchase before or after establishing Portuguese tax residency now directly determines how much IMT you owe.

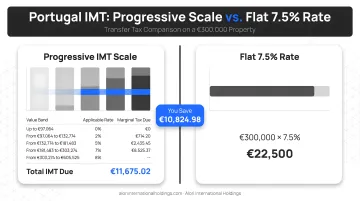

Example: €300,000 Property Purchase

Under Previous Progressive Scale (Residents):

- First €97,064: 0% = €0

- Next €40,933 (€97,064–€137,997): 2% = €819

- Next €52,162 (€137,997–€190,159): 5% = €2,608

- Remaining €109,841 (€190,159–€300,000): 7% = €7,689

- Total IMT: €11,116 (3.7% effective rate)

Under New Flat Rate (Non-Residents):

- Total IMT: €22,500 (7.5%)

Difference: €11,384 additional tax

Annual Property Taxes: IMI and the AIMI Wealth Tax

IMI (Annual Property Tax)

IMI (Imposto Municipal sobre Imóveis) is Portugal's annual municipal property tax, comparable to US property tax.

Rates:

- Urban properties: 0.3–0.5% of the official taxable value (VPT)

- Rural properties: 0.8%

Each municipality sets its own rate within the urban band. Lisbon currently charges 0.45% and Porto 0.42% for most urban properties.

Payment Process: The Portuguese Tax Authority sends a payment notice by April 30 each year.

| Total IMI Due | Payment Schedule |

|---|---|

| Under €100 | Single payment by May 31 |

| €100–€500 | Two installments (May 31, August 31) |

| Over €500 | Three installments (May 31, August 31, November 30) |

Payments can be made through the Finance Portal, ATM, or in-person at a tax office.

AIMI (Wealth Tax)

AIMI (Adicional Imposto Municipal sobre Imóveis) applies on the value of Portuguese property above €600,000 per individual.

Rates for Individuals:

| Property Value Band | AIMI Rate |

|---|---|

| €600K–€1M | 0.7% |

| €1M–€2M | 1.0% |

| Above €2M | 1.5% |

Couples filing jointly benefit from a €1.2M threshold before AIMI applies.

The rates differ significantly for legal entities, particularly for offshore structures.

For Legal Entities:

- Standard legal entities: 0.4%

- Companies holding property in favorable tax jurisdictions: 7.5%

IMI Exemptions

Two exemptions are worth knowing about before you buy.

A 3-year temporary exemption applies to properties purchased as a primary residence or for rental, provided:

- The property's taxable value is under €125,000

- The buyer's taxable income in the prior year did not exceed €153,300

A reconstruction exemption covers owners whose properties undergo municipal-funded reconstruction, granting a 3–5 year IMI waiver.

Rental Income and Capital Gains Tax for Non-Residents

Rental Income Tax

Non-residents: Flat 28% on all rental income, regardless of total income.

Residents: Progressive income tax (14.5–48%).

Deductible Expenses: Utility bills, maintenance, and repair costs with receipts can reduce the taxable rental income base.

Rental Contract Registration: Stamp duty of 10% of annual rent is owed by landlords on rental contracts registered for more than one month. Rental contracts exceeding one month must be registered with the Portuguese Tax Authority.

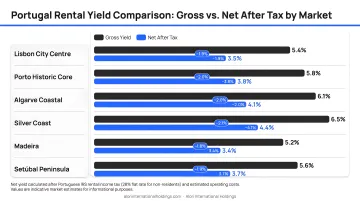

Net Rental Yields by Market:

| Market | Gross Yield | Net Yield (after 28% tax) |

|---|---|---|

| Santarém / smaller Algarve towns | 6–8% | 4.3–5.8% |

| Lisbon city center | 4–5% | 2.9–3.6% |

Secondary markets consistently outperform Lisbon on net yield — a relevant factor for non-residents optimizing after-tax returns.

Capital Gains Tax

When you sell a Portuguese property, a separate tax applies to any gain realized.

Non-residents: Flat 28% on the full capital gain, adjusted for allowable costs.

Residents: Progressive income tax on only 50% of the capital gain.

Deductible Costs:

- Transaction costs at purchase (IMT, stamp duty, notary and legal fees)

- Documented renovation and improvement costs

- Real estate agent commissions at sale

Inflation Adjustment Coefficient: The coeficiente de desvalorização da moeda reduces the taxable gain for properties held over several years. For properties sold in 2025, the applicable coefficients were published in Portaria n.º 382/2025/1 — with longer holding periods qualifying for steeper reductions that can materially lower the effective tax owed.

The US-Portugal Tax Treaty and Practical Steps for American Buyers

US-Portugal Tax Treaty

The US and Portugal have a double taxation treaty (signed September 6, 1994, effective January 1, 1996) that allows American property owners to credit Portuguese taxes paid against their US tax liability. This means income and gains taxed in Portugal are not taxed again at the full US rate — though your overall US liability may still apply to any gap.

Key Treaty Articles:

- Article 6: Rental income from Portuguese property is taxed in Portugal first

- Article 14: Capital gains on property sales are subject to Portuguese CGT rates

- Article 25: US residents claim a foreign tax credit for Portuguese taxes already paid

US Reporting Requirements: Americans must report Portuguese rental income and capital gains on their US federal tax returns. File Form 1116 (Foreign Tax Credit) to claim the credit for Portuguese taxes paid.

Recommendation: Work with a dual-jurisdiction tax advisor before purchasing — ideally one with active Portuguese client experience.

Understanding the treaty is step one. Executing the purchase correctly is step two — and that requires getting the right structures in place early.

Practical First Steps for American Buyers

- Obtain a NIF through a Portuguese tax representative before any purchase activity

- Open a Portuguese bank account (required for the property transaction and tax payments)

- Engage a Portuguese lawyer (advogado) to conduct due diligence on title, permits, and encumbrances

- Budget for total acquisition costs:

- IMT: 7.5% (non-residents)

- Stamp duty: 0.8%

- Notary fees: ~1%

- Legal fees: 1–2%

- Total: approximately 10–11% of purchase price

For American investors who want Portugal property opportunities with legal structures and exit strategies already reviewed, Alori International Holdings works with buyers across the transaction process — from identifying the right asset to managing the tax and compliance side of ownership.

Frequently Asked Questions

Is there an annual property tax in Portugal?

Yes. IMI (Imposto Municipal sobre Imóveis) is paid annually by all property owners, including non-residents, at rates of 0.3–0.5% of the taxable value for urban properties and 0.8% for rural properties. Owners of properties valued above €600,000 may also owe the AIMI wealth tax.

Can I buy property in Portugal if I'm not a resident?

Non-residents, including Americans, can freely purchase property in Portugal with no ownership restrictions. The main requirement is obtaining a NIF (tax identification number) through a Portuguese tax representative before completing the purchase.

What is the proposed 7.5% flat IMT rate and does it apply to me now?

Yes—the 7.5% flat IMT rate for non-resident buyers was enacted in December 2025 under Law 73-A/2025 and is now in force. It replaces the progressive IMT scale for non-resident residential purchases.

What capital gains tax will I pay if I sell my Portuguese property as a non-resident?

Non-residents pay a flat 28% on the full capital gain at the time of sale. Deductible costs (purchase expenses, renovations, legal fees) reduce the taxable gain, and an inflation coefficient may also apply for properties held long-term.

Do American buyers have to pay taxes in both the US and Portugal on the same income?

The US-Portugal tax treaty prevents true double taxation—American investors can claim a foreign tax credit on their US return (Form 1116) for taxes already paid in Portugal. However, reporting obligations exist in both countries, and a dual-jurisdiction tax advisor is recommended.

What exemptions exist that can reduce my property tax burden as a non-resident?

Two key exemptions stand out:

- IMI exemption: A 3-year exemption applies to qualifying properties under €125,000 in taxable value, subject to income limits.

- IMT exemption: The flat 7.5% rate can be avoided by committing to long-term rental under the moderate rent ceiling (€2,300/month) or by establishing Portuguese tax residency within two years of purchase.