Introduction

Portugal's reputation as a tax-friendly European haven for expats has undergone a dramatic transformation. The country's celebrated Non-Habitual Resident (NHR) regime—which for over a decade offered generous tax breaks to foreign professionals, retirees, and investors—closed to new applicants on January 1, 2024. In its place stands IFICI (Tax Incentive for Scientific Research and Innovation), a narrower program that exchanges the broad appeal of the original NHR for targeted benefits aimed squarely at tech, research, and innovation professionals.

For expats considering Portugal in 2025, this shift creates both confusion and opportunity. Investors and retirees who relied on outdated NHR information now face progressive tax rates reaching 48%, while qualified professionals in scientific and technology sectors can still secure a 20% flat rate for a decade.

The stakes are high. Establishing Portuguese tax residency means Portugal taxes your worldwide income—not just what you earn locally—making residency status the single most consequential financial decision in your relocation plan.

This guide covers the practical details you need before making any move:

- Who qualifies as a Portuguese tax resident

- What IFICI actually offers—and who it excludes

- How Americans handle dual tax obligations

- What property investors need to know about Portugal's multi-layered tax system

Whether you're a software engineer targeting Lisbon, a retiree weighing the numbers, or an investor evaluating Portuguese real estate, the sections below give you a clear framework before you commit.

TLDR: Key Facts About Portugal Tax Incentives for Expats in 2025

- The original NHR regime closed to new applicants January 1, 2024; existing holders keep benefits for their full 10-year term

- IFICI (NHR 2.0) offers a 20% flat tax on Portuguese income, limited to professionals in scientific research, tech, innovation, and related high-value sectors

- Portugal taxes residents on worldwide income at progressive rates of 12.5% to 48%, plus solidarity surcharges up to 5%

- Americans must still file US taxes abroad; the Foreign Tax Credit and Foreign Earned Income Exclusion ($130,000 for 2025) both help prevent double taxation

- Property investors face layered taxes: IMT at purchase, annual IMI property tax, AIMI wealth tax above €600,000, and capital gains tax on sale

How Tax Residency Works in Portugal

The Two Primary Tests

Portugal uses a straightforward dual-test framework to determine tax residency under Article 16 of the Personal Income Tax Code (CIRS). You become a Portuguese tax resident if you meet either:

- The 183-Day Rule: Spending more than 183 days in Portugal (consecutive or non-consecutive) within any 12-month period that starts or ends in the tax year

- The Habitual Residence Test: Maintaining a dwelling in Portugal under circumstances indicating you intend to occupy it as your primary residence as of December 31

Triggering either test has one immediate consequence: Portugal will tax your worldwide income, not just Portuguese-source earnings. That includes:

- Foreign dividends and interest

- Rental income from properties abroad

- Capital gains on overseas assets

- Pensions and employment income, regardless of where earned

Additional Triggers and Partial-Year Rules

Beyond the primary tests, residency can also be triggered if you serve the Portuguese state abroad or work as a crew member on Portuguese-operated ships or aircraft — relevant primarily for diplomats, civil servants, and maritime or aviation professionals.

Portugal also applies partial-year residency rules: you become a resident from your first day of presence and cease residency on your last day. If you exceed 183 days and later earn Portuguese-source income after departing, Portugal may treat you as a full-year resident — unless that income is taxed at comparable rates in another EU/EEA state. For expats relocating mid-year, this makes arrival date and income timing critical to avoid unintended full-year tax liability.

Portugal's Tax Incentives for Expats in 2025: The IFICI (NHR 2.0) Explained

What IFICI Offers

The Tax Incentive for Scientific Research and Innovation (IFICI), formalized through Ministerial Decree No. 352/2024/1 effective December 2024, is Portugal's official NHR successor. The program delivers two core benefits:

- 20% flat tax rate on qualifying Portuguese employment or self-employment income (Categories A and B)

- Tax exemption on foreign-source income (dividends, interest, capital gains, rental income) provided that income is taxable in its source country

These benefits last for 10 consecutive years.

Who Qualifies for IFICI

Eligibility requires three conditions:

- New tax residency in Portugal (you become a Portuguese resident)

- No Portuguese tax residency in the prior 5 years

- Income from approved activities, including:

- Scientific research and R&D roles

- Higher education teaching positions

- Technology and innovation company employment

- Certified startup positions

- Highly qualified roles in investment-aided companies

- Export-oriented businesses (companies with 50%+ of turnover from exports)

The Azores and Madeira autonomous regions have authority to define their own qualifying activity lists, potentially expanding opportunities in those jurisdictions.

Critical Differences from Original NHR

IFICI's most significant limitation: it applies only to active income (employment or self-employment), not passive income. The original NHR taxed foreign pensions at a flat 10%; IFICI exposes that same income to progressive rates reaching 48%. That's a dramatic reversal for retirees and passive investors who built plans around the old regime.

Registration Deadlines and Process

New residents must register for IFICI by January 15 of the year following their first year of residency. A transitional provision allowed individuals who became residents in 2024 to register by March 15, 2025.

Late registration is costly. Key implications:

- Benefits start only from the year of registration — not your residency year

- A 2024 resident who registers in 2026 loses an entire year of the 10-year window

- Missing the deadline by even one year permanently shrinks your benefit period

Understanding the deadlines helps clarify who should actively pursue IFICI — and who should look elsewhere.

Who Benefits, Who Doesn't

Strong fit for IFICI:

- Software engineers and tech professionals relocating to Lisbon or Porto

- Academic researchers and university faculty

- R&D professionals in pharmaceutical, biotech, or engineering sectors

- Startup founders and employees in certified Portuguese startups

- Export-focused consultants and service providers

Poor fit for IFICI:

- Retirees living on pensions (now taxed at progressive rates up to 48%)

- Passive investors relying on dividends and capital gains

- Remote workers whose employers aren't classified in qualifying sectors

- Digital nomads without formal Portuguese employment

For property investors moving to Portugal, IFICI's value depends entirely on your income profile. Active earners in qualifying sectors can pair property ownership with meaningful tax savings. Retirees and passive investors, however, will face Portugal's standard progressive rates regardless of how they structure their real estate holdings — making the choice of program (or alternative structure) a critical part of any relocation plan.

Portugal's 2025 Income Tax Rates for Expats

Progressive Tax Brackets for Residents

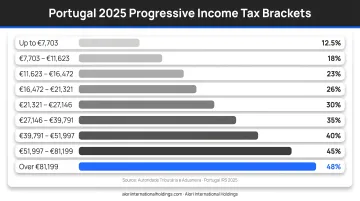

Portugal taxes residents on worldwide income using progressive brackets for Mainland Portugal in 2025:

| Taxable Income (€) | Marginal Rate |

|---|---|

| Up to €8,342 | 12.50% |

| €8,342 – €12,587 | 15.70% |

| €12,587 – €17,838 | 21.20% |

| €17,838 – €23,089 | 24.10% |

| €23,089 – €29,397 | 31.10% |

| €29,397 – €43,090 | 34.90% |

| €43,090 – €46,566 | 43.10% |

| €46,566 – €86,634 | 44.60% |

| Above €86,634 | 48.00% |

Solidarity Surcharge: An additional 2.5% applies to income between €80,000 and €250,000, and 5% applies above €250,000. This means effective top rates can reach 53% for the highest earners.

Non-Resident Taxation

Non-residents face simpler flat rates on Portuguese-source income:

- Employment and business income: 25%

- Dividends and interest: 28%

- Capital gains: 28%

Unlike residents, non-residents cannot elect into the progressive bracket system or claim standard deductions — the flat rates above are the final tax.

Investment Income and Rental Rates

That's an 80% reduction compared to the standard rate for leases beyond 20 years. Short-term vacation rentals receive no such discount, which meaningfully shifts the after-tax yield math for property investors weighing rental strategies.

American Expats in Portugal: US Tax Obligations and How to Avoid Double Taxation

The Citizenship Tax Trap

The United States taxes its citizens on worldwide income regardless of where they live—a practice shared by only Eritrea globally. If you're an American living in Lisbon, you must file US tax returns every year, even if you haven't set foot in the US for decades. This stands in stark contrast to most other nationalities who stop filing home-country returns once they establish foreign residency.

The US-Portugal Income Tax Treaty exists to prevent double taxation, but its practical value for Americans is limited. Article 1's "Saving Clause" explicitly allows the IRS to tax US citizens as if the treaty didn't exist. As a result, Americans must rely on domestic US tax code provisions—not the treaty—to avoid being taxed twice.

Foreign Tax Credit: Your Primary Defense

Income tax is only part of the compliance picture. The US-Portugal Totalization Agreement handles the social security side, preventing Americans from paying into both systems simultaneously. For assignments, the rule is straightforward:

- Assignments under 5 years: Pay US Social Security only

- Assignments 5+ years: Pay Portuguese social security only

Without this agreement, many expats would pay into both systems for years without ever qualifying for benefits from either.

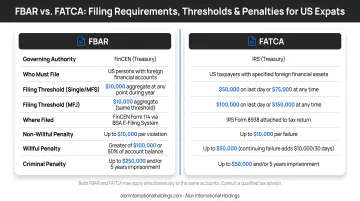

FBAR and FATCA: The Reporting Traps

Americans in Portugal face two separate foreign account reporting requirements with dramatically different thresholds and penalties:

FBAR (FinCEN 114):

- Threshold: Aggregate foreign account balances exceed $10,000 at any point during the calendar year

- Penalties: Up to $10,000 per non-willful violation; willful violations incur the greater of $100,000 or 50% of account balance

- Filing: Separate from your tax return, due April 15 (with automatic extension to October 15)

FATCA (Form 8938):

- Threshold for expats filing jointly: Foreign financial assets exceed $400,000 at year-end or $600,000 at any time during the year

- Penalties: $10,000 initial penalty, up to $50,000 for continued failure after IRS notification

- Filing: Attached to your regular tax return

The $10,000 FBAR threshold is deceptively low. A single bank account, retirement account, or investment account can trigger reporting. The penalties for non-compliance are severe and apply even to innocent mistakes. Missing the FBAR filing while otherwise completing your tax return on time is one of the most common and costly errors American expats make. Treat these as two separate compliance tracks.

Property and Capital Gains Taxes for Expat Investors in Portugal

Purchase Taxes: What You Pay Upfront

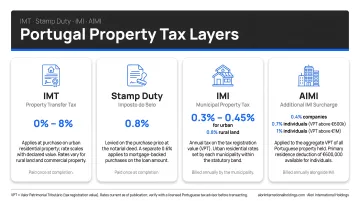

Portuguese property acquisitions trigger two immediate taxes:

IMT (Municipal Property Transfer Tax): Progressive rates apply to urban primary residences, scaling from 0% on the first €106,346 to a flat 7.5% for properties above €1,150,853. Secondary homes face stricter rates starting at 1%, and rural properties are taxed at a flat 5%. These rates are set by Article 17 of the CIMT.

Stamp Duty (Imposto do Selo): A flat 0.8% applies to the higher of the purchase price or Tax Asset Value (VPT). Mortgages trigger an additional 0.6% Stamp Duty for terms of 5 years or more.

For a €400,000 property, expect approximately €12,000–€16,000 in IMT plus €3,200 in Stamp Duty—roughly 4–5% of the purchase price in acquisition taxes alone.

Annual Holding Costs: IMI and AIMI

IMI (Municipal Property Tax): Levied annually on the property's Tax Asset Value (VPT). Municipalities set rates between 0.3% and 0.45% for urban properties; rural properties face 0.8%. For a property with a VPT of €300,000, annual IMI runs €900–€1,350.

AIMI (Additional IMI): A wealth tax on residential real estate portfolios. Individuals receive a €600,000 VPT exemption (€1.2 million for married couples filing jointly), with a 0.7% rate applied to the excess.

Corporate-owned residential properties face a 0.4% AIMI rate from the first euro, with no exemption threshold. This is a meaningful tax penalty for holding Portuguese residential real estate through corporate entities. High-net-worth investors who relied on this structure in the past should review whether it still makes sense for their portfolio.

Capital Gains Taxation: The 50% Rule

Following EU anti-discrimination rulings, both residents and non-residents are now taxed on only 50% of capital gains from Portuguese real estate sales. The included 50% is added to your taxable income and subjected to progressive rates (12.5%–48% for residents) or standard flat rates for non-residents.

Example: You sell a property for €500,000 that you purchased for €350,000, realizing a €150,000 gain. Only €75,000 (50%) is taxable. If you're a resident in the 44.6% bracket, you'll pay approximately €33,450 in tax on the gain—an effective rate of 22.3% on the total gain, not 44.6%.

Primary Residence Exemption

Gains from selling a primary residence are fully exempt if proceeds are reinvested into another primary residence within the EU/EEA. The reinvestment must occur within 36 months after the sale or 24 months prior. This exemption can eliminate capital gains tax entirely for expats upgrading or relocating within Europe.

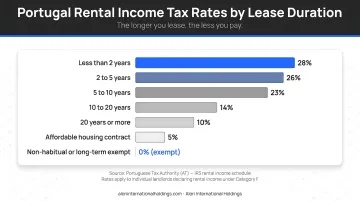

Rental Income Strategy

Not every investor is focused on exit. For those holding Portuguese property for yield, the rental income tax structure rewards lease length directly:

| Lease Duration | Rental Income Tax Rate |

|---|---|

| Under 2 years | 28% |

| 2–5 years | 25% |

| 5–10 years | 15% |

| 10–20 years | 10% |

| Over 20 years | 5% |

The difference between a short-term contract and a 20-year lease is an 80% reduction in the tax rate on rental income—a material shift in net yield for long-term holders.

For investors building accurate return models, the full tax picture matters at every stage. Acquisition costs run 4–5%, annual holding taxes range from 0.3% to 0.7%+ depending on portfolio value, rental income is taxed at 5–25% depending on lease terms, and exit taxation lands at effective rates around 22–24% on gains. Alori International Holdings structures its Portuguese property analysis around each of these layers, so investors understand their real returns before committing capital.

Frequently Asked Questions

What are the tax incentives for expats in Portugal?

Portugal's main expat tax incentive in 2025 is IFICI (NHR 2.0), offering a 20% flat tax on qualifying active income for 10 years. It's available only to professionals in research, innovation, and technology sectors who haven't been Portuguese residents in the prior 5 years. Double taxation treaties provide additional relief for specific income types.

Do American expats pay taxes in Portugal?

Yes. Americans who qualify as Portuguese tax residents (183+ days or primary residence) pay Portuguese taxes on worldwide income at progressive rates up to 48%. US filing obligations continue regardless, but the Foreign Tax Credit and Foreign Earned Income Exclusion ($130,000 for 2025) typically eliminate actual double taxation.

Will Portugal tax my U.S. Social Security?

Under the original NHR regime, foreign pension income (including Social Security) could be tax-exempt. Under IFICI and the standard tax system, foreign pension income is generally subject to Portuguese income tax at progressive rates. US-Portugal tax treaty Article 18 governs this treatment and is worth reviewing with a cross-border tax advisor.

What replaced the NHR regime in Portugal?

IFICI (Tax Incentive for Scientific Research and Innovation), commonly called NHR 2.0, replaced the original NHR regime on January 1, 2024. The key shift: eligibility is now restricted to active income earners in qualifying sectors—tech, R&D, and innovation—rather than the broader professional categories the original regime covered.

What property taxes do expats pay when buying in Portugal?

At purchase, expect IMT (transfer tax, typically 4–7.5%) and Stamp Duty (0.8%). Annual holding costs add:

- IMI: 0.3–0.45% of assessed property value

- AIMI: 0.7% on residential portfolio value above €600,000 (individuals) or €1.2 million (couples)

How can US expats avoid double taxation in Portugal?

Two main tools: the Foreign Tax Credit (Form 1116), which offsets US taxes dollar-for-dollar with Portuguese taxes paid, and the Foreign Earned Income Exclusion (FEIE), which excludes up to $130,000 of foreign-earned income from US taxation in 2025. Since Portuguese rates often exceed US rates, the FTC frequently eliminates remaining US tax liability.