Introduction

Many American investors approach international real estate by chasing headlines, selecting destinations based on lifestyle appeal, or following peer recommendations—and this reactive approach produces poor outcomes. Without a defined strategy guiding market selection, legal structuring, and risk management, even promising properties in high-growth markets can become costly mistakes. Successful cross-border investing comes down to executing a disciplined framework before committing a single dollar—not simply picking a popular destination.

That framework demands structured decision-making across market selection, ownership setup, currency exposure, due diligence, and exit planning — all coordinated before acquisition. This guide presents the strategic principles designed specifically for American investors building durable, cross-border wealth in the $150,000–$600,000 range.

Key Takeaways:

- Define your goal first — capital appreciation, rental income, or residency each demands a different strategy

- Evaluate markets on macroeconomic data and regulatory environments, not headlines

- A 10–15% currency fluctuation can materially affect total returns — understand exposure before entry

- Verify legal title, zoning, and exit liquidity before committing capital

- Set your exit strategy and rental approach at acquisition, not when you're ready to sell

Start With a Clear Investment Goal

International real estate attracts capital for three primary reasons: capital appreciation, rental income, and lifestyle or residency benefits. Each motivation demands distinct strategies across market selection, property type, and hold period.

The three motivations break down differently in practice:

- Appreciation seekers target emerging markets with strong GDP growth and urbanization trends, typically holding for 5–10 years

- Rental income buyers focus on established tourism hubs or expat-dense cities with proven occupancy rates and legal short-term rental frameworks

- Lifestyle and residency buyers accept lower financial returns in exchange for visa eligibility or seasonal access

Mixing these motivations creates one of the most costly errors for first-time international buyers. Purchasing a vacation property in a scenic coastal town while expecting investment-grade cash flow rarely works—lifestyle markets command premium pricing that compresses yields, while high-yield markets often lack the infrastructure or stability desirable for personal use. Pursuing both at once usually means fully achieving neither.

That clarity doesn't stop at strategy — it shapes your legal and tax structure from day one. An investor seeking rental income may benefit from direct personal ownership to simplify U.S. tax reporting. Appreciation-focused buyers holding property long-term might require a local entity structure for estate planning or capital gains optimization.

Residency-motivated purchases often trigger specific entity requirements tied to visa programs. These structural decisions cascade into every subsequent choice — financing, legal setup, exit planning — making goal clarity the essential first step in any international investment framework.

How to Select High-Conviction International Markets

A "popular" destination is not the same as a "high-conviction" market. Popularity reflects momentum and media attention; high conviction reflects data, demographics, and fundamentals that support durable long-term value regardless of short-term sentiment. Investors who mistake the former for the latter often buy at cycle peaks in regulatory environments they don't understand, only to face liquidity challenges when trends reverse.

High-conviction markets share specific macroeconomic indicators that support sustained property demand:

- GDP growth trajectory: Markets with consistent 3–5% annual growth outperform stagnant developed economies for appreciation — absolute GDP size matters less than direction

- Inflation stability: Volatile inflation erodes real returns even when nominal rents rise

- Foreign investment inflows: Signal international confidence and available capital

- Currency track record: How a currency has performed against the USD determines whether exit proceeds hold value when repatriated

Demographic signals are equally telling. Look for:

- Urbanization rates: Population moving into cities where housing supply can't keep pace

- Age cohort growth (25–45 year olds): The primary driver of rental demand and first-time buyer markets

- Rental housing shortfall: The gap between available units and household formation creates pricing power for landlords

- Expat and migration inflows: Indicate whether international demand will supplement local buyer activity

Regulatory and legal environments must be underwriting criteria, not afterthoughts. Before committing capital, verify:

- Foreign ownership rules: Whether you can hold property directly or need a local entity

- Repatriation of capital: Whether rental income and sale proceeds can move offshore

- Property rights enforcement: The practical ability to defend ownership in court — not just what the law says, but how courts function

- Political stability: The foundation for predictable rule of law across a multi-year hold

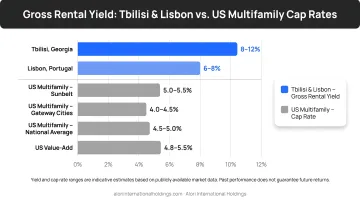

Portugal and Georgia exemplify high-conviction markets combining these fundamentals. Portugal offers transparent ownership laws, strong tourism growth, and established expat communities, while Georgia demonstrates 7.42% gross rental yields with improving regulatory frameworks and strategic positioning between Europe and Asia. Alori International Holdings focuses specifically on these markets by integrating macroeconomic analysis with in-country expertise, identifying where data and local insight support durable investment decisions rather than speculation.

Markets driven primarily by foreign buyer enthusiasm rather than structural demand present significant risks. When prices rise faster than local incomes, rental yields, or GDP growth, you're buying momentum—not fundamentals. Entering unfamiliar regulatory environments at cycle peaks compounds risk, as regulatory changes often follow speculative price surges. High-conviction investing means waiting for markets where price, fundamentals, and regulatory clarity align, even if that means passing on today's trending destinations.

Understanding Legal Structures and Ownership Options

American investors acquiring international property typically choose from three ownership structures: direct personal ownership, foreign LLC or local legal entity, or offshore holding structure. Each carries distinct trade-offs across liability protection, taxation, and estate planning that must be evaluated within both U.S. and foreign legal frameworks.

Here's how each option compares in practice:

- Direct personal ownership — simplest structure; no liability shield, but avoids entity-triggered reporting requirements

- Foreign LLC or local legal entity — liability separation and cleaner estate planning, with added U.S. reporting complexity

- Offshore holding structure — maximum privacy and asset protection, highest compliance cost and regulatory burden

Direct personal ownership in your individual name is often the simplest and most tax-efficient route for Americans. It typically avoids foreign account reporting requirements that entity ownership triggers, and allows straightforward mortgage interest and depreciation deductions on U.S. tax returns. However, direct ownership provides no liability protection — if a tenant is injured, your personal assets are exposed. Some countries also prohibit foreign individuals from holding property directly, making entity structures unavoidable regardless of preference.

Foreign LLC or local legal entity structures provide liability separation and can simplify estate planning by allowing shares to transfer rather than property titles. In some jurisdictions, entities offer favorable tax treatment or enable access to local financing.

The trade-off is U.S. reporting complexity — entity ownership triggers forms like the 5471 (foreign corporation ownership) and may add state-level fees or franchise taxes. Coordinating U.S. and foreign legal advisors up front avoids structures that quietly create tax inefficiencies on both sides.

Offshore holding structures — entities in jurisdictions like BVI, Cayman Islands, or Panama — offer the strongest privacy and asset protection. For most investors in the $150,000–$600,000 range, though, the math rarely works out. Strict U.S. reporting requirements, elevated compliance costs, and potential tax complications tend to offset any financial benefit. These structures make sense in specific high-complexity scenarios, not as a default.

Qualified attorneys in both the U.S. and the target country are essential — not a nice-to-have. A structure that optimizes tax treatment in one jurisdiction often creates significant complications in another.

A Portuguese entity that reduces capital gains tax locally may trigger U.S. controlled foreign corporation rules. An ownership structure that simplifies inheritance in Georgia may complicate Medicaid planning stateside. Coordinated legal guidance resolves these conflicts before they become expensive to unwind.

Currency Risk and Financing Strategies

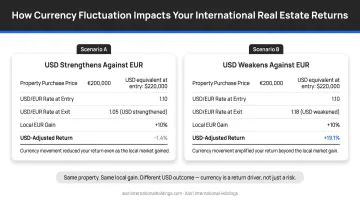

Currency fluctuations directly affect total returns at both acquisition and exit. When purchasing property denominated in euros or Georgian lari, USD strength determines your purchasing power—a stronger dollar buys more foreign real estate. At exit, currency movements affect repatriation value—selling a Portuguese property for €400,000 yields different USD proceeds depending on whether EUR/USD sits at 1.05 or 1.20. A realistic 10–15% currency shift between purchase and sale can materially alter net returns when converting proceeds back to dollars.

Consider an American investor purchasing a €300,000 Lisbon apartment when EUR/USD trades at 1.10 ($330,000 USD equivalent). Five years later, they sell for €360,000—a solid 20% appreciation in euro terms. If EUR/USD has weakened to 0.95, the sale proceeds convert to $342,000 USD, delivering only 3.6% total return in dollar terms over five years. Currency movement, not property performance, often determines how much you actually take home.

The financing landscape for international buyers differs fundamentally from U.S. domestic markets. The 30-year fixed mortgage is largely a U.S.-specific product; most foreign markets offer variable-rate or shorter-term loans (5–15 years), often with higher deposits (30–50%) and stricter income documentation for foreign buyers.

As a result, many American investors fund international purchases through alternative sources:

- Liquid assets or cash reserves

- Securities-backed loans collateralized by U.S. investment portfolios

- Home equity lines drawn from domestic properties

Developer financing programs have emerged as practical alternatives, particularly for off-plan properties in markets like Georgia and Portugal. These typically feature 0% interest installment plans extending up to 48 months with 10–30% down payments, allowing staggered capital deployment across construction timelines. This approach eliminates currency conversion all at once and provides time to optimize exchange rates across multiple payment tranches.

Knowing your financing path before committing shapes how you enter a deal. Cash buyers can wait for favorable exchange rates; developer payment plans spread currency risk across multiple conversion dates rather than concentrating it in a single transaction—a structural advantage worth building into your initial underwriting.

Building Your Due Diligence Framework

International due diligence requires a multi-layer approach covering legal, physical, and market dimensions that are significantly harder to verify remotely than in domestic markets. Three core legal checks anchor this layer:

- Title verification confirms the seller owns the property free of disputes

- Encumbrance checks reveal hidden liens or mortgages that could survive the sale

- Zoning and rental legality confirmation ensures the property can be used as intended—critical when banking on short-term rental income

Property condition assessment protects against structural defects, deferred maintenance, or building code violations that don't appear in listing photos. Local pricing benchmarks prevent overpayment by comparing the asking price to recent comparable sales in the same neighborhood—data often unavailable or unreliable in markets with limited public records. Each layer requires local expertise because verification standards, public record accessibility, and legal precedents vary dramatically across jurisdictions.

Who You Need on the Ground

Three professionals are essential to transaction integrity in any international deal:

- Licensed local attorneys verify title structures, review purchase contracts for unfavorable terms, and handle proper registration post-closing

- In-market real estate advisors provide accurate pricing benchmarks, identify neighborhood-level demand patterns, and assess developer credibility where track records aren't publicly searchable

- Independent appraisers deliver objective property valuations when seller-provided comps can't be trusted

Exit liquidity must be verified before entry. Before committing capital, confirm three things:

- Resale market activity — high transaction volume signals buyers will exist when you're ready to sell

- Buyer profile — local purchasers, foreign investors, and expatriates each respond to different demand drivers

- Long-term demand fit — your property type and price point should hold relevance across a projected 5–10 year hold period, not just today's conditions

That verification burden is real — and it compounds when you're working across unfamiliar jurisdictions. Alori International Holdings pre-vets properties for legal structure, title integrity, and defined exit strategy, so investors can rely on established frameworks rather than independently verifying every element from abroad.

Understanding local landlord-tenant laws, short-term rental restrictions, and required property management infrastructure is critical before committing to rental income strategies. Regulations vary sharply by city and country—Lisbon has implemented strict Alojamento Local containment zones capping short-term rental density at 5% in historic areas, while Tbilisi operates with minimal regulation requiring only basic tax declarations. Buying a property assuming rental income without verifying legal operability creates stranded capital.

Define Your Exit and Rental Strategy Before You Buy

Exit strategy must be defined at acquisition, not at disposition. Before closing, nail down:

- Target buyer profile — local purchasers, foreign investors, or expatriates

- Resale timeline — holding 5 years, 10 years, or indefinitely

- Capital gains exposure — projected tax liability in both the host country and with the IRS

- Minimum acceptable return thresholds — the floor below which the deal doesn't pencil

These parameters drive property selection, financing structure, and ownership entity decisions from the start.

Rental income strategies fall into two categories with very different operational profiles:

- Long-term residential — 12-month leases to local tenants or expatriates; minimal furnishing, standard lease contracts, routine tenant screening

- Short-term vacation rentals — tourist-facing platforms like Airbnb; full furnishing, dynamic pricing, frequent cleaning, and active marketing required

Licensing requirements separate these models just as much as operations do. Many jurisdictions have tightened short-term rental rules in recent years, with permits unavailable in historic districts or subject to density caps that effectively close the market to new entrants.

Rental yield expectations must be grounded in actual market data. While Tbilisi averages 7.78% gross rental yields, Lisbon delivers only 3.82% gross—and these are gross figures before taxes, repairs, and management fees. Net yields typically run 1.5–2% lower than gross, meaning realistic net yields in Lisbon sit around 1.8–2.3%. Investors should compare these returns against U.S. alternatives—domestic core multifamily cap rates average 4.75%—to justify the added complexity of international exposure.

U.S. tax obligations follow the property regardless of location — rental income is taxable to U.S. persons no matter where the asset sits. The offsetting deductions are substantial, though:

- Mortgage interest and property management fees

- Depreciation on a 30-year schedule (foreign property)

- Repairs and operating expenses

- Foreign tax credits for taxes paid to the host country

That last item prevents double taxation. A tax advisor with cross-border experience ensures you claim all available deductions while meeting reporting requirements in both jurisdictions.

Properties positioned for short-term rentals in newly restricted zones face expensive operational overhauls when regulations shift. Those purchased purely for appreciation must generate enough gain to cover holding costs if resale timelines stretch. Locking in both the rental model and exit criteria before closing eliminates those mid-ownership surprises.

Frequently Asked Questions

What country is best for real estate investment?

The right market depends on your investment goals, budget, and risk tolerance. Markets with stable fundamentals, transparent ownership laws, and growing demand — such as Portugal or Georgia — tend to attract disciplined long-term capital. Suitability varies based on individual objectives and financial circumstances.

Are international REITs a good investment?

International REITs offer liquid, low-barrier exposure to foreign markets and can be useful diversification tools. They differ from direct ownership in control, tax treatment, and access to off-market opportunities or residency benefits — making them complementary to, not a substitute for, direct investment.

How much money do I need to invest in international real estate?

Entry points vary significantly by market. Some markets offer quality investment properties in the $100,000–$300,000 range, while others start much higher. Investors should also budget for transaction costs (typically 5–10% of purchase price), legal fees, currency conversion spreads, and ongoing property management—adding 15–25% to the base property price.

Do I need to pay taxes in both the U.S. and the foreign country?

U.S. citizens are taxed on worldwide income regardless of where property is located. Foreign taxes paid can often be credited against U.S. tax liability under foreign tax credit rules, reducing or eliminating double taxation — though working with a tax advisor familiar with both jurisdictions is essential.

Can I get a mortgage for international real estate as an American?

Local mortgages abroad are possible in some markets but come with stricter terms — typically 30–50% deposits, 10–15 year durations, and variable rates. Many American buyers instead use cash, securities-backed loans, or home equity lines to avoid navigating foreign lending requirements.

How do I find foreign investors to buy my house?

Sellers can attract international buyers by listing on global property platforms and working with agents experienced in cross-border transactions. Clear title documentation and professional legal representation are critical — foreign buyers demand higher certainty than domestic purchasers before committing.