Introduction

High-end real estate carries a reputation for wealth preservation and strong returns — yet hard data, particularly for luxury and international segments, is surprisingly difficult to pin down. A Knight Frank study found prime residential values in select global cities outpaced broader market indices by 20–30% over the past decade, yet many investors still face a fundamental question: does the historical record actually justify the premium price tag?

The answer depends heavily on three critical variables: property type, location, and how return is measured. Broad-market housing returns differ sharply from income-generating rental properties, and luxury assets in gateway cities behave differently than mass-market residential stock during downturns. Investors who understand these distinctions make better-grounded decisions — ones built on evidence rather than assumption.

This article examines broad historical real estate ROI benchmarks, how high-end properties have diverged from the average, and what factors have driven durable returns in markets like Portugal, Georgia, and other internationally focused luxury segments.

Key Takeaways

- High-end properties in select markets consistently outperform the 4–7% annual returns seen in broad residential real estate data

- Rental income yield — not capital appreciation — has historically been the more reliable driver of luxury real estate returns

- Location and fundamentals matter more in high-end real estate than any other segment; not all premium properties deliver premium returns

- Tax treatment, legal structures, and exit strategies vary significantly across international markets — understanding these is non-negotiable before committing capital

- In markets like Portugal and Georgia, macroeconomic fundamentals and regulatory clarity are what separate durable returns from speculative exposure

The Historical Record: What Real Estate Returns Tell Us

The long-run data on residential real estate is more compelling than most investors realize — but only when you look beyond price appreciation to total return.

Price Appreciation vs. Total Return

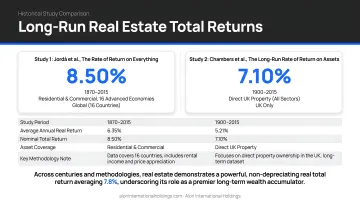

The most commonly cited figure — approximately 4.2% annual nominal return from 1928-2023 — reflects price appreciation only on owner-occupied homes, based on Case-Shiller data compiled by NYU's Aswath Damodaran. This figure explicitly understates total return by excluding rental cash flows entirely.

A more comprehensive view emerges from academic research:

- 560-year study (1465-2024): Paul Schmelzing's SSRN research shows housing delivered 5.9% nominal annual total return, with 5.5% attributed to rental yield and only 0.4% to capital gains

- 145-year cross-country analysis (1870-2015): The Federal Reserve Bank of San Francisco study covering 16 advanced economies found residential real estate returned approximately 7% annually in real (inflation-adjusted) terms — on par with equities but with lower volatility

Private vs. Owner-Occupied Real Estate

That income-driven return advantage becomes even more pronounced in private, institutional-grade real estate. Invesco research tracking the NCREIF Property Index from 1996–2025 shows private real estate (an unleveraged composite) consistently ranked as the highest or second-highest performing asset class over rolling 10-year periods — frequently competitive with or outperforming equities.

The gap comes down to purpose. Institutional-grade properties are actively managed for total return, with income generation as the primary driver. Owner-occupied homes produce no cash flow and are held for shelter, not investment optimization.

The Leverage Amplification Factor

Even modest price appreciation amplifies returns significantly when financing is used. A property purchased with 20% down that appreciates 25% in value delivers a 125% return on invested capital. Carrying costs reduce that figure, but the principle holds.

This leverage dynamic explains why income-generating real estate with conservative financing has historically outpaced owner-occupied housing — provided the underwriting accounts for interest, taxes, and ongoing maintenance.

High-End Real Estate: Why the Numbers Look Different

High-end real estate for investment purposes is defined by several characteristics beyond price point: location within prime or lifestyle markets, structural demand from wealth migration and foreign capital, and asset quality that weathers economic cycles. This is distinct from speculative luxury development in overbuilt markets.

Price Resilience During Downturns

Prime residential markets demonstrate different volatility profiles compared to mass-market housing during economic shocks:

| City | 2008-2009 GFC Decline | 2020 COVID-19 Decline |

|---|---|---|

| London | -16.9% | -2.6% |

| New York | -12.5% | -3.6% |

| Paris | +0.5% | +1.2% |

| Lisbon | Data limited | -5.0% |

Source: Knight Frank, Savills research

Prime properties in gateway cities and lifestyle destinations have historically experienced shallower price declines during recessions compared to broader housing markets, though results vary significantly by city and economic conditions.

Premium Rental Yield Dynamics

High-end properties in tourism-driven or lifestyle markets can generate yields that outpace standard long-term residential rentals:

Lisbon:

- Prime residential gross yield: 3.5-4.8%

- Short-term rental median revenue: €34,000/year

Tbilisi:

- City average gross yield: 8.1% (February 2026)

- Short-term rental gross yield: 10.54%

Tbilisi's 8.1% gross yield reflects frontier market exposure; Lisbon's 3.5-4.8% reflects Eurozone stability. Investors are compensating for that risk differential, not ignoring it.

Structural Demand Drivers

High-end real estate benefits from demand drivers largely independent of local economic cycles:

- Wealth migration and foreign capital flows

- Citizenship and residency programs

- Remote work trends enabling location flexibility

- Tourism infrastructure expansion

These factors support demand that standard residential markets rarely benefit from. That said, market selection matters. Overbuilt premium segments in speculative markets have historically underperformed. The distinction between genuine structural demand and a marketing-driven luxury label is what separates consistent returns from disappointing ones.

The Two Engines of Luxury Real Estate Returns: Income and Appreciation

Total return in luxury real estate comes from two components: rental income yield (cash flow) and capital appreciation. Academic long-run data shows income yield has been the more reliable and dominant contributor to total return, while capital gains tend to be lumpy and market-cycle dependent.

Understanding Cash-on-Cash Return and Cap Rate

Cash-on-cash return measures annual pre-tax cash flow as a percentage of the total cash invested (including down payment and closing costs). This metric reveals how efficiently invested capital generates income.

Capitalization rate (cap rate) expresses net operating income as a percentage of property value. Savills reports average global prime residential gross yields moved to 3.15% in 2024, though this varies significantly by market.

In emerging luxury markets, yields typically run higher — compensating for regulatory uncertainty and currency risk that more established markets don't carry.

How Leverage Amplifies Both Components

Leverage magnifies both income returns and appreciation gains — but also introduces risk. Consider a property generating 6% cash-on-cash return with 5% annual appreciation:

- Unleveraged: 11% total return

- With 75% financing at 4% interest: 15%+ return on invested equity (assuming positive cash flow after debt service)

This amplification effect explains why disciplined entry pricing matters more in high-end real estate, where liquidity is lower and holding periods are longer. Overpaying by 10-15% can eliminate several years of appreciation gains and significantly reduce total return.

Currency and Inflation Dynamics in International Markets

High-end properties in markets with strong local demand but weaker currencies offer USD-denominated investors an additional return layer when currency appreciates. A property purchased in Georgian Lari that appreciates 8% annually in local terms delivers additional USD return if GEL strengthens against the dollar during the holding period.

Rental income tied to local CPI or market demand adds another layer of protection. In high-inflation environments, rental rates often increase faster than property operating costs — creating positive operating leverage that compounds total return over time.

What Drives Stronger Returns in Select International Markets

Macroeconomic and demographic factors historically underpin above-average real estate returns in international markets:

- Population growth or in-migration creating structural housing demand

- Tourism infrastructure expansion supporting short-term rental markets

- Favorable tax and ownership frameworks for foreign buyers

- Limited supply of high-quality stock in desirable locations

Portugal: Structural Demand Meets European Stability

Portugal demonstrates multiple return drivers aligning simultaneously:

Tourism Growth: In 2025, Portugal recorded 32.5 million guests (19.7 million foreign) and 82.1 million overnight stays, representing 3.0% and 2.2% growth respectively over 2024.

Foreign Buyer Volume: In 2023, buyers with tax residence outside Portugal purchased 8,471 dwellings totaling €3.4 billion. In Lisbon's Urban Rehabilitation Area, foreigners accounted for 33% of residential purchases by volume.

Price Appreciation: The median price of family dwellings in Portugal rose 15.5% year-over-year in Q4 2024. For the prime segment, Lisbon luxury property values grew 4.4% in 2025, with forecasts of 4-5.9% growth for 2026.

Regulatory Note: Following Law 56/2023 in October 2023, real estate purchases no longer qualify for Portugal's Golden Visa program. Investors must treat investment strategy and immigration planning as separate decisions.

Georgia: High-Growth Frontier with Institutional Accessibility

Georgia offers a different value proposition with strong price appreciation and low entry barriers:

Tourism Growth: In 2024, Georgia welcomed 7.4 million international non-resident travelers, a 4.2% increase from 2023.

Foreign Buyer Activity: Foreigners accounted for over 17% of total property transactions in Georgia during 2024, driven by low entry barriers and full freehold ownership rights for non-residents.

Price Appreciation: The Residential Property Price Index for Tbilisi increased 10.4% year-over-year in Q4 2024, with average asking sale prices rising 7% YoY in February 2026.

Legal Framework: Foreigners can buy, register, and sell residential or commercial real estate with full ownership rights. The only restriction applies to agricultural land, which is prohibited for foreign individuals.

Risk Mitigation Through Selective Market Entry

What Portugal and Georgia share — beyond headline growth numbers — is structural accessibility: defined legal frameworks, transparent ownership rights, and measurable demand drivers. That combination is what separates durable investments from speculative ones.

Alori International Holdings applies this lens across both markets, using data-driven analysis and local expertise to identify entry points where demand, legal clarity, and fundamentals converge.

The practical advantages of this selective approach extend beyond returns:

- Diversification away from domestic market cycles and correlated risks

- Access to legal structures with clear registration processes and defined exit strategies

- Local knowledge that surfaces pitfalls — mispriced assets, opaque titles, illiquid submarkets — before they erode returns

Not every international market offers this combination. Regulatory frameworks, transaction processes, and ownership rights must be verifiable and enforceable. Conducting that due diligence before committing capital is what separates sound international strategy from costly trial and error.

Building a High-Conviction Strategy: What to Look for Before Investing

Historical ROI data provides context, not guarantees. The difference between strong and poor outcomes in high-end real estate often comes down to entry discipline.

Critical Due Diligence Variables

Before committing capital to any market, four variables consistently separate disciplined investors from those who rely on marketing materials:

- Macroeconomic stability: GDP growth, political risk, currency stability, and regulatory consistency matter. Unpredictable policy environments can erase years of appreciation through sudden tax changes or ownership restrictions.

- Foreign ownership rights: Verify full freehold title, transparent property registration, and clear legal recourse. The World Bank Doing Business methodology identifies clear title confirmation and encumbrance checks as non-negotiable steps.

- Realistic rental demand: Base projections on comparable transaction data and actual yields in the specific micro-location — not national averages or developer brochures. A secondary-neighborhood property cannot command prime city-center yields.

- Comparable transaction data: Analyze recent sales prices per square meter, days on market, and buyer profiles. Markets where asking prices and transaction prices diverge significantly signal weak genuine demand.

Entry Discipline and Exit Clarity

Avoiding overpriced or oversupplied markets matters more than finding the "best" market. Overpaying by 15–20% eliminates multiple years of appreciation. Buying into oversupply creates liquidity risk when exit becomes necessary.

Before committing capital, establish:

- Clear exit strategy: Who are likely buyers when you sell? What transaction costs and timelines apply?

- Verified legal title: Obtain recent property registry extracts confirming ownership and checking for liens or encumbrances

- Developer track record: For new construction, verify completion history and financial stability

- Total cost of ownership: Include all taxes, fees, management costs, and currency conversion expenses

That due diligence complexity is precisely where specialist guidance changes outcomes. For investors pursuing international high-end real estate in the $150,000–$600,000 range, working with a firm that integrates global investment strategy with in-country execution — like Alori International Holdings, which vets projects, verifies legal structures, and defines exit strategies before capital is committed — closes the gap between sound strategy and actual results.

Frequently Asked Questions

What is the historical return on real estate investment?

Historical data shows broad ranges depending on asset type. Owner-occupied home price appreciation averaged ~4.2% annually (1928–2023), while income-generating rental properties across 16 countries returned approximately 7% annually in real terms over 145 years (1870–2015). The difference reflects rental income excluded from price-only metrics.

What's a good ROI for real estate?

It depends on asset type and risk profile. Income-generating rental properties in established markets historically delivered 6–7% total real return, while private institutional real estate competed with equities over rolling 10-year periods. For most investors, 6–7% real return in a supply-constrained, income-generating market represents a strong benchmark.

Is 7% real return realistic?

A 7% real (inflation-adjusted) return is at the high end of what historical data supports for real estate overall, but is achievable in income-generating assets in high-demand markets — particularly where leverage is used responsibly and rental yields are strong. Reaching that level consistently requires disciplined market selection focused on structural demand, not speculative appreciation.

How does high-end real estate ROI compare to standard residential property?

High-end real estate has historically shown greater price resilience in downturns and can deliver stronger rental yields in lifestyle and tourism markets. However, it requires more careful market selection — luxury designations in speculative or oversupplied markets can significantly underperform standard residential.

What are the biggest risks to ROI in luxury real estate investments?

Key risks include overpaying at peak market conditions, illiquidity (difficulty exiting quickly), unclear legal title or transaction structures in international markets, and over-reliance on capital appreciation rather than income yield as the primary return driver.

How does international luxury real estate fit into a diversified portfolio?

International high-end real estate historically shows low correlation to domestic stocks and bonds (correlation near 0.06 with US stocks, -0.12 with US bonds for private real estate). It also provides an inflation hedge through rent adjustments and geographic diversification — making it a practical complement to domestic stocks and bonds for investors building long-term, cross-border portfolios.