Introduction

Deploying real estate capital effectively has become genuinely difficult. Domestic U.S. markets are crowded, cap rates have compressed, and property in major metros now carries equity-like volatility with bond-like yields. For investors accustomed to real estate as a stabilizing force, that's a problem worth solving.

The core tension facing today's HNW investor is clear: domestic U.S. markets have become crowded and overpriced in many metros, while rising correlation with broader economic volatility has eroded real estate's traditional stabilization role. This reality is pushing sophisticated capital toward a more deliberate, globally diversified approach.

This guide covers the investment vehicles available to HNWIs, the case for international diversification, how to evaluate markets before committing capital, and the structural considerations — tax, legal, and exit planning — that shape long-term outcomes.

Why Real Estate Is a Cornerstone of HNW Wealth Strategy

Real estate occupies a unique position in a high-net-worth portfolio because it delivers three functions simultaneously:

- Inflation protection through tangible asset ownership

- Recurring income through rents

- Long-term capital appreciation over market cycles

Most equities or fixed income instruments deliver only one or two of these benefits. That structural combination is what makes property a distinct allocation — not just an alternative.

Portfolio Stabilization Through Low Correlation

Real estate's low correlation with public markets provides genuine portfolio stabilization. During the 2008 financial crisis, private real estate funds recorded smaller drawdowns than equity markets — a pattern widely documented by institutional data providers — demonstrating the asset class's defensive characteristics during periods of equity market stress. This diversification benefit becomes particularly valuable for portfolios concentrated in liquid securities.

Generational Wealth Transfer

Unlike financial assets, physical property can be passed to heirs with clear title, used personally, and repositioned across market cycles. This positions real estate as a practical tool in legacy planning for families with multi-generational investment horizons. Property held in appropriately structured entities can transfer outside of probate, reduce estate tax exposure, and provide heirs with both income and appreciation potential.

The Main Real Estate Investment Vehicles for HNWIs

Direct Property Ownership

Owning residential, commercial, or industrial properties directly gives HNWIs the highest level of control—over tenant selection, property improvements, financing structures, and exit timing. This control comes with responsibility: direct ownership demands active oversight or a reliable property management layer to handle day-to-day operations.

Cash flow quality depends heavily on three factors:

- Entry price relative to replacement cost and market fundamentals

- Location-specific demand drivers (employment growth, infrastructure, demographics)

- Loan structure and leverage ratio

REITs and Listed Real Estate Funds

Publicly traded REITs offer real estate exposure with stock-like liquidity, making them useful for HNWIs who want sector-specific exposure—logistics, healthcare, data centers, multi-family—without managing assets directly.

The trade-off: REIT prices move with market sentiment and often diverge from underlying property values. When equity markets sell off, REIT share prices can drop sharply even when the underlying properties continue generating stable cash flows.

Non-traded and private real estate funds represent a middle ground. These vehicles offer:

- Access to institutional-quality deals unavailable to individual investors

- Professional management and diversification across properties

- Potentially higher yields than public REITs

- Longer hold periods (typically 5–10 years) with limited liquidity

- Accredited investor requirements in virtually all cases

Private Equity Real Estate and Syndications

Private equity real estate and syndication structures allow HNWIs to co-invest alongside other accredited investors in large-scale acquisitions—apartment complexes, commercial portfolios, mixed-use developments—that would be inaccessible individually.

Critical evaluation criteria:

- Manager track record across full market cycles

- Fee structures (acquisition fees, asset management fees, promote/waterfall)

- Capital call obligations and timing

- Exit timelines and projected hold periods

- Alignment of interests between sponsors and investors

Tax-Efficient Structuring Tools

The vehicle you choose determines more than just returns—it shapes your tax exposure for years. Strategic investors build tax advantages into acquisition planning from the start, not as afterthoughts:

- 1031 exchanges allow investors to defer gains by rolling proceeds from one property directly into another

- Depreciation allowances generate paper losses that offset rental income, even on properties that are appreciating in value

- Qualified Opportunity Zone funds defer and potentially reduce capital gains taxes on qualifying reinvestments

International Real Estate: The Diversification Strategy Most U.S. Investors Overlook

Most American HNWIs concentrate nearly all real estate exposure domestically, creating unacknowledged country risk. When U.S. housing markets correct, interest rates spike, or regulatory conditions shift, an entirely domestic real estate portfolio absorbs the full impact. International allocation breaks that concentration — and the criteria for doing it well are specific.

What Makes a Market Investment-Grade

Genuine investment-grade foreign markets exhibit specific characteristics beyond headline growth rates:

Demand fundamentals — demographics (urbanization, household formation), tourism growth, and employment expansion — determine whether rental income and appreciation are structurally supported, not cyclically inflated.

Legal and transactional clarity includes:

- Clear foreign ownership laws and property registration

- Capital repatriation rules

- Contract enforcement mechanisms

Stability indicators worth evaluating:

- Currency convertibility and historical volatility

- Price performance across prior economic downturns

- Depth of both local and international buyer pools

High-Conviction Markets: Portugal and Georgia

Portugal offers EU legal stability, a growing tourism economy, favorable residency pathways, and strong rental demand in Lisbon and Porto.

Georgia (the country) offers low entry prices, a flat-tax regime, straightforward foreign ownership laws, and rapid infrastructure development. The nation's strategic position between Europe and Asia, combined with investor-friendly policies, has attracted increasing American capital.

Firms like Alori International Holdings specialize in identifying and curating opportunities in these vetted markets. That means vetted deal flow, verified legal structures, and on-the-ground pricing benchmarks — not just desk research.

The Lifestyle Migration Dimension

Many HNWIs evaluate international property not purely as financial investments but as part of a broader residency or relocation strategy. The investment case and the lifestyle case often reinforce each other, particularly in markets with residency-by-investment programs or favorable tax treatment for foreign-income earners. Portugal's Golden Visa pathway is a clear example — qualifying property purchases can unlock EU residency while generating rental yield.

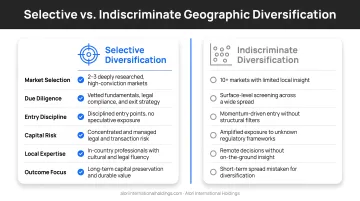

Selective vs. Indiscriminate Diversification

Geographic diversification only works when it comes with operational depth. Investing in fewer, better-understood markets — where local relationships, off-market deal flow, and regulatory knowledge are established — produces fundamentally different outcomes than spreading capital thinly across unfamiliar regions chasing yield.

The core distinction:

- Selective diversification: fewer markets, deeper expertise, established local networks

- Indiscriminate diversification: broad geographic spread, limited in-country knowledge, higher execution risk

Geographic diversification without operational depth creates new risks rather than reducing them.

What to Evaluate Before Investing in International Real Estate

Legal Ownership Structures

Research whether the target country permits direct foreign property ownership or requires ownership through a local entity or trust structure. Failing to structure the purchase correctly creates title, inheritance, or repatriation problems down the line.

Local legal counsel with real estate expertise is essential. Generic international law firms without in-country specialists routinely miss jurisdiction-specific requirements that directly affect ownership rights.

Currency Exposure and Financing

International property purchases introduce currency risk. When the dollar strengthens, foreign asset values in USD terms decline, and vice versa. This works both ways—dollar weakness increases the USD value of foreign holdings.

Financing considerations:

- Most foreign lenders won't extend mortgages to non-residents on standard terms

- All-cash or cross-collateralized financing is common

- Model returns in both home currency and USD to understand true performance

Exit Liquidity and Buyer Pool Depth

Thin exit liquidity is one of the most underestimated risks in international real estate. Some markets — Lisbon and Tbilisi among them — carry deep pools of both local and foreign buyers. Others have limited resale demand that extends holding periods and weakens your pricing position when it's time to exit.

Map your exit before you buy: identify the likely buyer profile, the realistic holding period, and the conditions under which you'd sell.

In-Market Intelligence vs. Remote Investing

The single largest risk in international real estate is making decisions without reliable on-the-ground knowledge. This affects:

- Pricing accuracy and negotiation leverage

- Legal verification and title clarity

- Contractor quality and construction oversight

- Rental market realism and property management

- Micro-location selection within broader markets

Investors should either build local relationships themselves or work with a firm that has established in-country infrastructure. Alori International Holdings, for example, combines global investment strategy with local execution in Portugal and Georgia to bridge this gap.

Tax Considerations and Structural Advantages

Domestic Tax Tools

Three tools reduce the tax burden on domestic investment properties:

- Depreciation generates paper losses that offset rental income, even on appreciating assets — residential rental property uses a 27.5-year recovery period, creating annual deductions that reduce taxable income.

- Mortgage interest deductibility lowers the after-tax cost of leverage on investment properties.

- 1031 exchanges defer capital gains taxes indefinitely by rolling sale proceeds into another qualifying property.

International Tax Implications for U.S. Investors

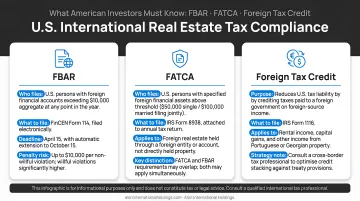

Cross-border investing adds a layer of compliance that domestic-only investors never encounter. American citizens owe U.S. tax on worldwide income regardless of where property is located.

Foreign real estate held directly is not reported on FATCA Form 8938, but foreign bank accounts used to collect rental income trigger reporting requirements.

Key compliance considerations:

| Requirement | Threshold | Purpose |

|---|---|---|

| FBAR (FinCEN Form 114) | Foreign accounts exceeding $10,000 aggregate value | Reports foreign financial accounts |

| FATCA (Form 8938) | $50,000–$600,000 depending on filing status and location | Reports specified foreign financial assets |

| Foreign Tax Credit (Form 1116) | N/A | Offsets double taxation on foreign rental income |

Depreciation on foreign property uses the Alternative Depreciation System (ADS), extending the recovery period to 30 years for residential property compared to 27.5 years for domestic property. This reduces annual tax deductions.

The Foreign Tax Credit allows a carryback of 1 year and carryforward of 10 years for unused credits, providing flexibility in managing international tax obligations.

Trust and Entity Structures for Real Estate Holdings

HNWIs often hold real estate through LLCs, family limited partnerships, or irrevocable trusts to:

- Separate liability from personal assets

- Streamline estate transfer outside probate

- Reduce estate tax exposure through legitimate structuring

- Facilitate fractional ownership among family members

For international holdings — such as properties in Portugal or Georgia — the appropriate structure often requires additional entity layers that align with both U.S. tax obligations and local ownership laws. Getting this right from acquisition, not after the fact, is where structure decisions create or destroy long-term value.

Building a Future-Proof Real Estate Portfolio

Deliberate Portfolio Construction

A well-structured real estate portfolio for a HNWI assigns distinct roles to each holding:

- Income generation — stable, cash-flowing properties in established markets

- Appreciation — growth-oriented assets in emerging or improving locations

- Inflation hedging through tangible assets with pricing power and replacement cost support

- Currency diversification via international holdings across different monetary regimes

Each position serves a purpose. That intentionality separates portfolio construction from opportunistic accumulation.

Liquidity Balance

Because direct real estate and private funds are illiquid, HNWIs should ensure that liquid real estate vehicles (REITs, listed funds) and other liquid assets outside real estate together provide sufficient access to capital for:

- Personal needs and lifestyle expenses

- Market opportunities requiring quick deployment

- Emergency reserves

Illiquid positions should only represent capital that truly has a long time horizon and won't be needed for 5–10 years.

Global Strategy Meets Local Execution

Finding opportunities that hold up at both the macro level and the transaction level — title, legal structure, pricing, rental assumptions, exit paths — is difficult without a partner who operates across both dimensions.

Alori International Holdings is built around this model. The firm offers curated opportunities in Portugal and Georgia, with in-country expertise and defined exit strategies for long-term capital growth. Key differentiators include:

- Selective focus on high-conviction markets with operational depth

- Access to off-market opportunities through local professional networks

- Vetted legal structures, accurate pricing, and clear exit strategies from the outset

Frequently Asked Questions

What are the best real estate investments for high-net-worth individuals?

The strongest HNWI portfolios typically combine direct property ownership, private real estate funds, and international holdings in structurally sound markets. The key is matching each investment type to a specific portfolio role — not pursuing uniform exposure across all categories.

How much of a portfolio should HNWIs allocate to real estate?

Most family offices and wealth managers suggest 15–30% of total investable assets in real estate. The exact split across direct holdings, private funds, and REITs depends on the investor's liquidity needs and time horizon.

What are the risks of international real estate investment for American investors?

Key risks include currency fluctuation, foreign legal frameworks, thinner market liquidity, and U.S. tax reporting obligations on worldwide income. Most are manageable with proper legal structuring and reliable in-market expertise.

What is the difference between direct ownership and REITs for HNW investors?

Direct ownership provides control, tax advantages like depreciation, and stronger appreciation potential but requires active management and significant capital. REITs offer liquidity and professional management but trade at market prices that may diverge from real estate fundamentals and provide less control over individual assets.

How does international real estate help protect against domestic market risk?

International real estate moves on different economic cycles, interest rate regimes, and demand drivers than the U.S. market. When domestic property values or rental incomes decline, internationally diversified holdings can maintain or grow in value, reducing overall portfolio volatility and concentration risk.