Introduction

Georgia's foreign direct investment reached $1.69 billion in 2025, with U.S. investment surging 121% year-over-year. For American investors evaluating international diversification, that growth rate in a market of Georgia's size warrants serious attention.

This analysis covers what American investors and global capital allocators need to know before entering this market — FDI scale and trajectory, dominant sectors, legal protections for foreign capital, and the risks that require careful navigation.

Georgia's Foreign Investment Landscape: The Big Picture

Strategic Positioning Drives Capital Flows

Georgia sits at the crossroads of Western Asia and Eastern Europe, making it a natural transit and trade hub connecting Europe to Central Asia via the Middle Corridor. This geographic positioning directly drives where and why foreign capital flows into the country, particularly in transport infrastructure and logistics sectors.

Recent FDI Flow Trends Show Maturation

Georgia's FDI totaled $1,688.7 million in 2025, representing a 7.6% increase from the adjusted 2024 figure of $1,569.3 million. While this represents growth, the trajectory shows moderation from the 2022 peak of $2,224.2 million. This doesn't signal decline—rather, it reflects a maturing investment base with total FDI stock reaching 79.8% of GDP in 2023.

FDI Flow Trajectory (2022–2025):

| Year | FDI (USD millions) | Notable |

|---|---|---|

| 2022 | $2,224.2M | Peak year |

| 2023 | $1,928.5M | Moderation begins |

| 2024 | $1,569.3M | Adjustment period |

| 2025 | $1,688.7M | Stabilization with growth |

Reinvested Earnings Signal Long-Term Confidence

82.8% of Georgia's 2025 FDI came from reinvested earnings rather than new equity capital. Existing foreign enterprises are profitable enough to keep money in-country rather than send profits home — a concrete measure of operating confidence.

The flip side: net-new equity investment remains a structural challenge. Georgia is retaining capital well, but still working to attract fresh commitments from investors who haven't yet entered the market.

Economic Growth Stands Out Regionally

Georgia has maintained strong expansion despite regional conflicts. The IMF projects 7.2% growth for 2025. Against regional peers, the numbers tell a clear story:

| Country | 2022 GDP Growth | 2024 GDP Growth |

|---|---|---|

| Georgia | 10.9% | 9.7% |

| Azerbaijan | 4.7% | 4.0% |

This gap held even through the Russia-Ukraine war and post-COVID normalization — periods that compressed growth across the broader region.

International Rankings Provide Credible Benchmarks

Georgia's position in international indexes offers investors useful comparison points:

- Heritage Foundation Economic Freedom Index (2026): Rank 35 globally, Score 69.6 (classified as "Moderately Free")

- Transparency International CPI (2024): Rank 56 out of 180, Score 50

- World Justice Project Rule of Law Index (2025): Rank 52 out of 143, Score 0.58

These rankings place Georgia in the middle tier globally — ahead of many emerging markets, with institutional gaps that investors should factor into due diligence alongside the macroeconomic upside.

Who Is Investing in Georgia — and Why

Top Investor Countries: Understanding the UK Illusion

The 2025 preliminary ranking by FDI inflows reveals an interesting story:

| Rank | Country | 2025 FDI Inflows | Share of Total |

|---|---|---|---|

| 1 | United Kingdom | $334.2M | 19.8% |

| 2 | Turkey | $180.8M | 10.7% |

| 3 | Malta | $173.7M | 10.3% |

| 4 | United States | $158.1M | 9.4% |

| 5 | Azerbaijan | $143.9M | 8.5% |

| 6 | Netherlands | $91.9M | 5.4% |

The UK's dominant position is largely an artifact of corporate domicile effects. Georgia's two largest banks — TBC Bank Group and Bank of Georgia Group — are registered in England and listed on the London Stock Exchange.

Under IMF conventions, capital routed through these entities is attributed to the UK rather than the ultimate beneficial owners. The UK's 19.8% share reflects where the money is registered, not necessarily where it originates.

Azerbaijan's position reflects long-term infrastructure and energy corridor projects connecting the two countries. Turkey's significant presence stems from geographic proximity, cultural ties, and active construction and manufacturing sector investment.

U.S. Investment Surge Reflects Growing Confidence

U.S. FDI into Georgia more than doubled from $71.3 million in 2024 to $158.1 million in 2025, vaulting the U.S. to the fourth-largest investor position. The growth was concentrated in two sectors: real estate and IT. Both reflect the same underlying logic — Georgia offers low taxes, open capital flows, and a legal framework that American investors can navigate with confidence.

Bilateral Investment Treaty Provides Critical Protections

The U.S.-Georgia Bilateral Investment Treaty (BIT), which entered into force on August 17, 1997, provides American investors with substantial legal protections:

- National treatment: U.S. investors receive the same treatment as Georgian nationals

- Most-favored-nation status: U.S. investors can't be treated less favorably than investors from other countries

- Free transfer of funds: Guaranteed rights to convert and repatriate income after taxes

- International arbitration access: Disputes can be resolved through ICSID or UNCITRAL rather than relying solely on Georgian courts

That last point carries real weight. International arbitration means American investors aren't dependent on Georgian domestic courts to resolve disputes — a meaningful safeguard in any emerging market.

Key Sectors Driving Foreign Investment in Georgia

Finance and Insurance Dominates by Structure

Financial services accounted for $607.0 million in 2025 FDI, representing 35.9% of total flows. This dominance stems largely from the structural factor mentioned earlier: Georgia's largest financial institutions are legally registered outside the country, meaning their operational reinvestment is counted as FDI rather than domestic investment.

Real Estate: Consistent Capital from Global Buyers

Real estate drew $185.7 million in 2025 FDI, representing 11.0% of total flows. While sector-specific breakdowns by investor country aren't published, the overall doubling of U.S. investment coincided with strong growth in real estate FDI — suggesting significant American capital allocation to Georgian property markets.

That capital is concentrated in specific locations. Residential and commercial property in Tbilisi's premium districts (Vake, Saburtalo, Vera) and Batumi's coastal developments continue to attract global investors seeking rental yields of 6–10% annually and capital appreciation at entry prices well below Western Europe.

For American investors, navigating Georgia's property market requires local knowledge of legal structures, developer track records, and viable exit strategies. Alori International Holdings focuses specifically on this: curating vetted Georgian property opportunities with verified legal structures and defined exit strategies, bridging global capital with in-country expertise.

Transport and Logistics Benefit from Middle Corridor Growth

Transport sector FDI jumped from $105.2 million in 2024 to $166.1 million in 2025, representing 9.8% of total flows. This surge reflects Georgia's role as a critical link in the Middle Corridor (Trans-Caspian International Transport Route), which has seen cargo volumes quadruple since 2022 as companies bypass Russian routes following geopolitical tensions.

The EU has actively mapped investment needs to rebuild trade routes to Central Asia via the South Caucasus, positioning Georgia as a structural beneficiary of long-term infrastructure investment with predictable, sustained demand characteristics.

Information Technology: Strong Growth Driven by Tax Incentives

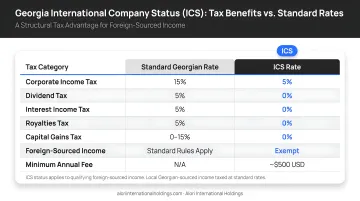

IT and communications FDI grew from $65.1 million in 2024 to $115.2 million in 2025, representing 6.8% of total flows. This growth reflects Georgia's competitive advantages for technology firms. The International Company Status (ICS) program offers qualifying IT firms a notably favorable tax structure:

- 5% corporate profit tax (vs. standard 15%)

- 0% dividend tax

- 5% payroll tax (reduced from standard rates)

These rates are dramatically lower than standard Georgian taxes, making ICS status a primary draw for international tech firms establishing regional operations.

Georgia's Investment Framework: Legal Protections and Incentives

Core Legal Protections Create Investor Confidence

Georgia's legal framework for foreign investment includes three fundamental protections:

Equal treatment under law: Georgian and foreign businesses operate under the same rules, with no restrictions on foreign ownership of non-agricultural property.

Unrestricted repatriation: Investors can move post-tax income out of the country without restrictions or delays.

Ten-year grandfather clause: The law shields existing investments from adverse legislative changes for a decade — meaningful protection against unexpected policy shifts.

Business Registration Offers Exceptional Efficiency

Business registration takes 1-2 business days through the National Agency of Public Registry at Public Service Halls, according to Enterprise Georgia. That speed reflects a broader philosophy of low friction for foreign capital — one that extends directly into the tax structure.

Georgia's tax system features six clearly defined types:

- 15% corporate profit tax on distributed earnings only (retained earnings taxed at 0%)

- 5% dividend tax for shareholders

- 18% VAT (standard rate)

- 0%, 5%, and 12% import tariffs (nearly 90% of goods qualify for zero rate)

Free Industrial Zones in Poti and Kutaisi extend these advantages further — businesses operating within them are exempt from corporate income tax, VAT, and import/export duties, making them particularly attractive for manufacturing and trade-oriented investment.