Introduction

Most international investors have already been priced out of Western gateway cities. Tbilisi hasn't reached that point yet — and in 2025, it remains one of the few European capital markets where double-digit price growth and sub-$2,000/sqm entry points still coexist.

Georgia's capital continues to attract cross-border capital for specific reasons: rising domestic incomes, sustained foreign investment inflows, and a tightening new-build supply pipeline that is putting upward pressure on both prices and rents.

Understanding where the market is heading — and where the risks sit — requires looking beyond headline numbers. This analysis breaks down the five trends reshaping Tbilisi in 2025: district-level price movements, transaction volume divergence, rental yield compression, supply constraints, and the macro and political drivers that will determine trajectory through 2026.

Key Takeaways

- Residential property prices in Georgia rose 11.5% year-on-year in Q1 2025, with Chughureti and Gldani exceeding 28% annual growth

- Transaction volumes softened despite rising prices — old flat sales fell nearly 30% while new apartment sales held steady

- Rental yields compressed to 9% citywide, down 1.5 percentage points year-on-year as price growth outpaced rent growth

- New construction permits fell 4.5% and completions dropped 22% in Q1 2025, tightening future supply

- Georgia's economy grew 9.4% in 2024, and foreign buyers access non-agricultural real estate on equal terms with citizens

Prices Rising Strongly Across Tbilisi Districts

Georgia's residential property price index rose 11.5% year-on-year in Q1 2025, according to Geostat data. This marks the ninth consecutive quarter of double-digit growth, and crucially, real inflation-adjusted prices grew 7.78% — confirming this is genuine appreciation, not just nominal inflation.

Property type performance diverged meaningfully:

- Flats increased 10.9% year-on-year

- Detached houses jumped 13.5% year-on-year

District-Level Price Movements

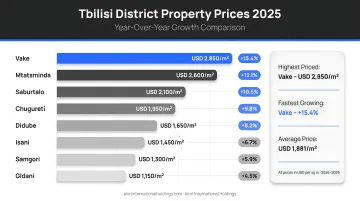

Tbilisi's property market is splitting sharply by location. Chughureti led flat price growth at 28.3% year-on-year, while Gldani posted the strongest detached house gains at 35.9%.

Q1 2025 Tbilisi Prices by District:

| District | Flats ($/sqm) | Flats YoY Growth | Houses ($/sqm) | Houses YoY Growth |

|---|---|---|---|---|

| Mtatsminda | $2,471 | +21.4% | $1,711 | +10.3% |

| Vake | $2,146 | +20.8% | $1,510 | +34.3% |

| Chughureti | $1,626 | +28.3% | $1,078 | +6.8% |

| Saburtalo | $1,568 | +12.0% | $1,302 | +17.2% |

| Samgori | $1,288 | +16.0% | $1,015 | +27.8% |

International Context

Even Mtatsminda's $2,471/sqm commanding position remains a fraction of comparable Western markets. For context, downtown Austin averaged $8,627/sqm in April 2025, while Prague averaged $5,918/sqm in Q4 2024. Outer Tbilisi suburbs like Samgori and Gldani sit well below $1,400/sqm, making them accessible even for middle-income international buyers.

Nine consecutive quarters of double-digit growth reflect three converging structural forces:

- Rising domestic incomes are expanding the local buyer pool beyond expatriates and investors

- Urban migration from Georgia's regions is sustaining housing demand in central and mid-tier districts

- Growing foreign buyer presence is absorbing inventory that would previously have sat longer at lower price points

Tbilisi still trades at a steep discount to Prague and Austin — but at 7.78% real annual appreciation, that discount is eroding faster than most investors expect.

A Market Split — Fewer Transactions, Higher Prices

While prices surge, total transaction volumes in Tbilisi fell approximately 1% year-on-year to around 9,100 units in Q1 2025. More striking: old flat sales plummeted 29.2% year-on-year in January 2025 — the steepest decline since the pandemic period — while new apartment sales rose modestly by 0.5%.

What This Divergence Means

Lower transaction volume alongside higher prices typically signals constrained supply, not weakening demand. The pool of quality, well-priced units is shrinking faster than buyers are stepping back.

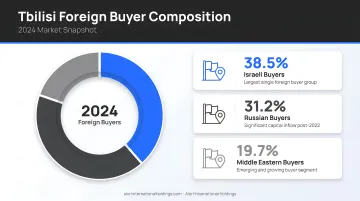

Buyer composition is shifting:

- Russian buyers dropped from 7% to 2% of total sales in 2024

- Israeli buyers rose from 4% to 12% of sales, accounting for 11% of all apartment purchases in early 2025

- Middle Eastern and Polish buyers are emerging as top contributors to foreign demand

Foreign investors — particularly from Israel, the Middle East, and Russia — increasingly favor short-term rental plays over direct ownership, reflecting both political uncertainty and higher entry prices. That preference shows up directly in which units move fastest.

The 50–75 sqm Segment Dominates

Apartments ranging from 50 to 75 sqm represented 44% of total sales in March 2025. This size band reflects who's driving the market: young professionals, domestic first-time buyers, and income-focused investors targeting small units with strong rental yields.

Rental Yields Softening as Investor Strategies Evolve

Gross rental yields in Tbilisi averaged 9.0% in Q1 2025, according to TBC Capital — down 1.5 percentage points year-on-year. The national average dropped to 7.53%, as prices rose faster than rents and asking rents fell in dollar terms.

District-Level Yield Variation

Q1 2025 Gross Rental Yields by District:

- Didi Dighomi: 7.38% – 10.18%

- Isani: 7.12% – 8.76%

- Saburtalo: 5.89% – 6.85%

- Vake: 5.00% – 5.65%

Higher-yield zones like Didi Dighomi and Isani attract income-focused investors willing to trade location prestige for current cash flow. Lower-yield areas like Vake and Saburtalo appeal to capital-appreciation buyers betting on long-term value growth in established premium districts.

Short-Term vs. Long-Term Rental Dynamics

Pre-2022, short-term yields of 12–18% were achievable in tourist-heavy areas. That market has normalized since the 2022–2023 demand spike driven by geopolitical displacement.

In 2025, Tbilisi recorded an average daily rate of $41, 63% occupancy, and $9,628 average annual revenue per listing — solid returns, but well below the peak years.

Monthly rents in dollar terms have pulled back from their 2022–2023 highs toward pre-conflict levels. In March 2025, the average asking rent in Tbilisi was $10.6 per sqm monthly.

For American investors, those numbers still look compelling in a global context. Gross yields in major European markets tell the story:

- Madrid: 5.04%

- Berlin: 3.88%

- Lisbon: 3.82%

Investors accustomed to 4–6% yields in US gateway cities are looking at double that in Tbilisi — with structural demand still intact.

The Mortgage Rate Factor

GEL-denominated mortgage rates averaged 13.28% in March 2025, up from 11.46% a year prior, despite the National Bank of Georgia holding its policy rate at 8.0%. This primarily affects domestic buyer financing — most foreign investors transact in cash or use USD-denominated instruments, insulating them from local credit tightening.

Supply Constraints and Shifting Foreign Capital

The Supply Picture

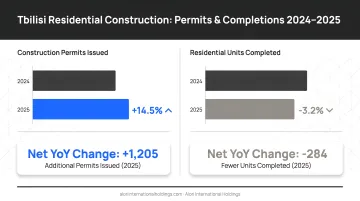

2024 saw strong residential construction growth: permits up 6.3% year-on-year and completions up 12.1%. But Q1 2025 reversed sharply — permits fell 4.5% and completions plummeted 22.5% year-on-year. That drop points to a tighter inventory cycle ahead — one that should support prices, particularly for new-build apartments in central districts.

Approximately 81% of Tbilisi's apartment stock was built before 1991. This aging housing stock creates a structural two-tier market:

- Newer builds command significant premiums

- Post-1991 construction carries less legal complexity on title

- Higher-income tenants strongly prefer modern builds with proper insulation, elevators, and parking

Tightening supply amplifies the demand dynamics already reshaping who is buying in Tbilisi.

The Shifting Foreign Buyer Profile

Russians historically represented the largest foreign buyer segment. The Russia-Ukraine war has pushed that capital toward diversification, and a new mix of nationalities is filling the gap:

- Israeli buyers grew over 40% in 2024, now capturing 11–12% of total sales

- Middle Eastern and Gulf buyers are prioritizing turnkey, rental-ready units

- Polish buyers are emerging as a top contributor to foreign demand

- American and Western buyers remain underpenetrated — representing one of the more asymmetric entry points in the market for internationally focused investors