Introduction

After two years of price corrections and investor caution, European real estate is showing clear recovery signals in 2025. Investment volumes are rising, valuations are stabilizing across major markets, and sectors driven by structural undersupply are outperforming expectations.

For American investors looking beyond domestic markets, the window is opening — but the timing matters. This guide breaks down where European markets stand today, which sectors are leading the recovery, and what the data suggests for investors considering entry in 2025.

Key Takeaways

- European real estate investment reached €244.5 billion in 2025, with Q4 posting a 17% year-over-year increase

- Residential and living assets captured €55.6 billion (+14% YoY), overtaking offices as Europe's largest investment sector for the second consecutive year

- Logistics faces near-term softness from trade uncertainty, though structural demand from nearshoring and e-commerce keeps long-term fundamentals intact

- Retail investment surged 11% to €38.8 billion, with retail parks recording near-record vacancy of just 1.2%

- Southern Europe—particularly Portugal, Spain, and Italy—recorded combined investment growth of 19% YoY, attracting rising cross-border capital

Residential & Living: Europe's Highest-Conviction Sector in 2025

European living assets captured €55.6 billion in investment in 2025 — a 14% year-over-year increase that pushed the residential sector ahead of offices for the second consecutive year. This isn't a cyclical blip. It reflects a structural repricing of where institutional capital sees the most durable returns.

Why this sector dominates:

- Record-low vacancy rates combined with rental growth accelerating to 5.2% by year-end 2025

- Chronic supply deficit across major European cities, with new housing supply falling 11% in 2024 and projected to decline another 5% in 2025 and 2026

- Structural undersupply creating sustained rental pricing power for investors entering now

The surge in purpose-built student accommodation (PBSA) illustrates institutional confidence in the living sector. PBSA investment jumped 57% above Q4 2024 levels and 30% above the five-year average, driven by urbanisation, household formation trends, and younger renters delaying home purchases. Each of these forces is demographic in origin, making the demand picture hard to reverse in the near term.

Supply constraints sustain returns:

Most major European cities remain structurally undersupplied in housing. New development has slowed sharply due to:

- Rising construction costs post-pandemic

- Tighter development financing

- Planning constraints and regulatory hurdles

This chronic supply gap is expected to sustain rental growth for investors over the next 3–5 years, creating a rare combination of income stability and appreciation potential.

Policy is beginning to move in investors' favor in select markets. Sweden's Presumption Rent Reform, effective January 2026, allows presumptive rents to fully correspond to general rent development, removing previous caps and improving return viability for new-build developers.

That said, political risk remains real. Rent controls in certain markets can significantly compress residential returns, and monitoring regulatory direction is as important as tracking supply fundamentals.

Logistics & Industrial: Structural Demand Beyond the Soft Patch

European logistics is navigating a cyclical soft patch in 2025, with vacancy exceeding 5% for the first time in over ten years. Trade tariff uncertainty and tenant caution have created near-term headwinds. Yet framing this as a structural break would miss the deeper opportunity.

Key context: Vacancy remains well below the long-term historical average, and current weakness reflects cyclical tenant behavior rather than fundamental demand erosion.

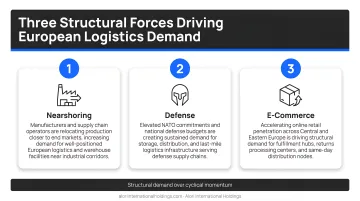

Three structural forces are building beneath that surface:

- Defense spending commitments across Europe rising toward higher GDP targets by 2030, requiring substantial new logistics infrastructure

- Nearshoring and supply chain reshoring driven by geopolitical tensions, pulling manufacturing and distribution closer to end markets

- E-commerce volumes expected to return to positive annual growth after a post-pandemic lull

On the supply side, new logistics construction fell to just 3.8% of total stock by mid-2025 — the lowest level since 2013. That constraint sets up supply-demand tightening and rental reversion as demand normalizes over the next 12–24 months.

ESG requirements are widening the gap between assets. 37% of occupiers now mandate green clauses across their portfolios, demanding net-zero-ready facilities with on-site energy generation. Modern, sustainable assets command rental premiums — obsolete stock faces increasing vacancy risk.

Retail's Comeback and the Office Market Divide

Retail has delivered one of 2025's strongest performances, with investment volumes reaching €38.8 billion, an 11% year-over-year increase. Retail parks and warehousing formats recorded near-record low vacancy of just 1.2%, making them a go-to allocation for institutional investors seeking stable income.

The office market presents a sharp bifurcation. Prime, green-certified offices in central business districts of major European cities recorded rental growth of 7.2% year-over-year with low vacancy in the best locations. However, secondary and non-compliant office stock faces growing obsolescence risk as tenants consolidate into higher-quality space.

That divergence is accelerating across three clear dimensions:

- Prime CBD assets with ESG credentials attract strong tenant demand

- Secondary buildings struggle with rising vacancy

- The gap between these categories continues to widen

Those headline numbers, however, don't tell the full story. Net office absorption turned negative across Europe's major cities in mid-2025, largely driven by Liberation Day uncertainty and tenant rationalization.

The supply side is shifting in prime locations' favor. Completions are forecast to fall to 3.1 million sqm in 2026 — the lowest annual level since 2017 — setting up a tighter supply-demand balance in core markets within 12–24 months.

What's Driving the European Real Estate Shift in 2025

Several overlapping forces are reshaping European real estate at once — monetary policy, supply constraints, cross-border capital, and demographic shifts. Each one operates independently, but together they're compressing timelines and widening return gaps between markets. Investors who understand the underlying drivers, not just the surface trends, can position earlier and more deliberately.

ECB Monetary Policy

The ECB lowered the deposit facility rate to 2.00% in June 2025, down from a 4.00% peak in September 2023. Lower debt costs improved property yield spreads, making real estate income returns more attractive relative to bonds — particularly for core assets.

Chronic Supply Constraint

Supply constraint is the single most important driver of rental growth across performing sectors. Construction costs surged post-pandemic, development financing tightened, and new supply across residential, logistics, and prime office is running well below long-term averages. This structural gap insulates rental growth even when economic demand softens.

Cross-Border Capital Flows

Cross-border capital held a 45% share of total European investment activity in 2025. North American investors led inflows, with capital reaching $21.63 billion in H2 2024 — a 10% year-over-year increase. That sustained flow reflects Europe's appeal to global investors looking to reduce concentration in US markets.

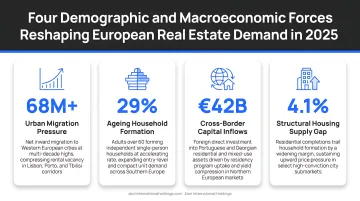

Demographic and Lifestyle Forces

- Ageing populations driving demand for senior living and healthcare real estate

- Urbanization and smaller household sizes increasing housing demand even in flat-population markets

- Growing cohort of remote workers and lifestyle migrants from the US choosing European cities, supporting both residential rental demand and hospitality assets

Southern Europe in Focus: Where International Capital Is Flowing

Southern Europe has emerged as one of the most dynamic sub-regions of the European market. Italy, Spain, and Portugal recorded combined investment volumes of €27.4 billion in 2025, a 19% year-over-year increase. Portugal stands out particularly, with investment growth exceeding 11% and earlier forecasts projecting gains above 20%—well above most core European markets.

Why Southern Europe attracts international capital:

- Strong tourism fundamentals driving hospitality and retail performance

- Persistent shortage of quality residential supply in major cities and coastal markets

- Attractive entry pricing relative to Northern European capitals

- Improving regulatory frameworks and transparent legal structures

For investors screening international markets, these factors carry real weight. Markets with structural supply shortages, improving legal frameworks, and below-peer pricing tend to hold value through cycles — and often outperform when sentiment catches up to fundamentals.

Alori International Holdings applies this kind of market-selection discipline in Portugal, combining macroeconomic analysis with on-the-ground expertise to identify opportunities where asset quality and local knowledge drive outcomes.

Future Signals for European Real Estate

Looking beyond 2025, European investment volumes are forecast to grow 16–18% in 2026, driven by continued pricing normalisation, more consistent institutional capital deployment, and improving macroeconomic conditions. Institutional re-engagement — not speculative momentum — is what's pulling capital back in.

Three emerging areas to watch:

Data centres: AI-driven hyperscaler demand is creating a new institutional asset class. Vacancy is forecast to reach an all-time low of 6.5% by the close of 2026, despite grid capacity challenges with connection lead times stretching to 10 years in established hubs.

Operational real estate niches: Self-storage, cold storage, EV charging, and dark kitchens offer resilient, service-linked income and higher yield potential. European self-storage rental rates grew 5.4% to €312.56 per sqm, attracting institutional bids.

Manage-to-green value-add strategy: Older office and industrial stock upgraded to meet ESG compliance is commanding measurable return premiums — occupiers are walking away from non-certified space, tightening supply for compliant assets.

These opportunities don't exist in isolation. Several structural risks could reshape the outlook over the next 12–24 months.

Key risk signals to monitor:

- French political and fiscal instability, which has pushed that market down several places in global real estate risk rankings

- Potential trade tariff escalation from the US, which could extend the logistics soft patch

- Interest rate uncertainty if fiscal expansion in Europe drives sovereign bond yields higher than expected

Conclusion

The European real estate market in 2025 is defined by a clear hierarchy: sectors with structural supply deficits and durable demand—residential, living, and well-located industrials—are delivering the strongest risk-adjusted returns. Meanwhile, the gap between prime and secondary assets continues to widen across all categories. For investors focused on fundamentals over headlines, that divergence is where the opportunity sits — not in broad exposure to "European real estate," but in selective positioning within the right sub-markets before the recovery fully prices in.

Navigating European real estate successfully requires more than market-level awareness. It demands country-by-country analysis and disciplined market selection that separates momentum investors from conviction investors. As transaction volumes recover and valuations firm through 2026 and 2027, the investors with the clearest entry rationale — not the broadest exposure — will capture the most durable upside.

Key conclusions from 2025 market data:

- Residential and living sectors continue to outperform on supply-demand fundamentals

- Prime assets in undersupplied urban markets are widening their lead over secondary stock

- Country-level selection matters more than regional allocation in the current cycle

- The recovery window is real, but pricing in mispriced sub-markets will narrow as volumes return

Frequently Asked Questions

What is the outlook for 2025 in the European real estate market?

European real estate is in a gradual but broadening recovery, with total investment volumes rising 17% year-over-year in Q4 2025 and valuations stabilising after two years of repricing. Residential, retail, and prime industrial are leading performance, though recovery pace varies by market and sector.

Are house prices dropping in Germany?

Despite pressure from higher financing costs, residential prices rose 3.0% year-over-year in Q4 2025. Structural undersupply in major German cities limits the depth of any price correction, and Germany is still expected to deliver positive total returns over the medium term.

Which European real estate sectors are performing best in 2025?

Top-performing sectors in 2025:

- Residential and living: lowest vacancy rates, 5.2% rental growth

- Retail parks: 1.2% vacancy, strong occupier demand

- Prime offices (CBDs): 7.2% rental growth despite weak overall absorption

Prime logistics assets are also performing well, supported by structural e-commerce demand.

What is driving rental growth across European cities in 2025?

The primary driver is severe supply constraint across all major sectors. New development slowed sharply due to rising construction costs, tighter financing, and planning constraints. Even modest demand growth translates into strong rental increases in well-located assets.

Is Portugal a good place to invest in real estate in 2025?

Portugal ranks among Europe's best-performing markets by investment volume growth (11% YoY), with strong fundamentals across residential, hospitality, and logistics. Pricing remains attractive relative to Western European peers, and growing international investor interest supports continued demand.

What risks should international investors consider in European real estate?

Key risks include:

- Political instability in France, weighing on investor confidence

- US trade tariff escalation, with potential knock-on effects for European logistics and export-linked sectors

- Currency exposure for dollar-based investors operating in euro-denominated markets

- Regulatory variation, particularly rent control policies that can affect residential returns in certain markets