Introduction

U.S. mortgage rates remain stubbornly elevated at 6.46%, and the median new home price has climbed to $400,500 — pushing the price-to-income ratio to a record 5.0, well above the pre-pandemic 4.1. The math is forcing a strategic shift. American investors are increasingly looking beyond their borders, moving capital into international markets where the dollar stretches further, entry points are lower, and demand is building before prices catch up.

That opportunity isn't evenly distributed. The most compelling emerging markets share a specific combination: affordable entry prices, rising demand, and structural tailwinds — infrastructure investment, demographic migration, and regulatory frameworks built to attract foreign capital. Getting there early, before prices reflect those fundamentals, is what separates opportunistic diversification from reactive repositioning.

This article examines five international real estate markets showing the strongest signals for 2026: Portugal, the Republic of Georgia, Mexico, Poland, and Vietnam. We'll explore what's driving their growth, what investors should know before entering, and why domestic U.S. real estate constraints are pushing capital overseas.

Key Takeaways

- USD strength and cross-border capital flows are reshaping which emerging markets offer real entry-point value in 2026

- Portugal, Georgia, Mexico, Poland, and Vietnam offer affordable entry points with structural demand drivers

- Domestic U.S. affordability headwinds have made international diversification a mainstream strategy, not a niche one

- Acting before a market gets widely recognized is where the strongest risk-adjusted returns are captured

- Local expertise and vetted legal structures matter more than market research alone

What Makes a Real Estate Market "Emerging" in 2026?

An emerging real estate market is one where demand fundamentals are building ahead of widely recognized price appreciation. These markets feature affordable entry, limited investor awareness, and identifiable structural catalysts—population inflows, employment growth, infrastructure investment—that precede the repricing phase.

Hot markets reflect demand already priced in — competition is fierce and prices have already adjusted. Emerging markets represent the window before that repricing occurs, offering the strongest risk-adjusted opportunity for long-term capital.

Five signals identify true emerging markets:

- Sustained population or expat in-migration creating rental demand

- Job market diversification beyond single industries

- Rising but still-affordable rental yields (typically 6–10% gross)

- New infrastructure or regulatory frameworks attracting foreign capital

- Growing but under-saturated developer pipeline

These signals matter, but they only tell part of the story — how a market is classified by institutional standards determines whether serious capital can actually flow in.

Institutional research firms like JLL evaluate markets based on transparency, regulatory enforcement, and liquidity rather than geography alone. Their 2024 Global Real Estate Transparency Index scores 256 indicators across 89 countries, placing markets into five tiers from Highly Transparent to Opaque. Poland and Portugal rank as Transparent markets, with strong data availability and regulatory maturity. Mexico and Vietnam sit in the Semi-Transparent tier, improving steadily as nearshoring and manufacturing investment drive institutional interest.

Top 5 Emerging International Real Estate Markets to Watch in 2026

U.S. domestic research organizations track American cities closely, but the most compelling price-to-growth opportunities in 2026 are cross-border. These five markets combine structural demand, favorable regulatory environments, and currency advantages for USD holders.

Portugal

Portugal remains a top international destination despite significant policy changes. The Non-Habitual Residency (NHR) regime ended in 2023, replaced by the more restrictive IFICI framework offering a 20% flat tax only for highly qualified professionals in R&D, tech, and higher education. The real estate route to the Golden Visa was also suspended in 2023—foreign investors now must invest €500,000 in qualifying investment funds to access residency.

Despite these changes, Portugal's housing market continues exceptional price growth. By November 2025, median asking prices hit €5,914/sqm in Lisbon and €3,908/sqm in Porto. This remains competitive against Paris (€10,620/sqm) and Amsterdam (€7,100/sqm), offering relative value among Western European capitals.

Why Portugal remains structurally undersupplied:

- Historical annual completions averaged only 15,000 units despite growing demand

- Historic property stock limitations restrict new development

- Foreign resident population reached 1.7 million in December 2023, with Brazilians forming the largest community (484,596)

- Short-term rental income yields averaged 4.32% nationally in November 2025

Entry points between $150,000 and $500,000 exist primarily in secondary cities, coastal towns outside the Algarve's Golden Triangle, and off-plan developments offering pre-construction pricing. Investors should focus on markets with tourism infrastructure and expat communities rather than chasing Lisbon's already-elevated prices.

Republic of Georgia

Georgia offers one of the most liberal foreign ownership frameworks globally. Foreign nationals can purchase freehold residential and commercial property without restrictions—the only exception is agricultural land. The tax environment features a flat 20% personal income tax and a 15% corporate tax based on the Estonian model, taxing only distributed profits.

Tbilisi versus Batumi:

Tbilisi, the capital, saw average sales prices reach $1,152/sqm in H1 2025, with prime districts commanding premiums: Mtatsminda at $2,471/sqm and Vake at $2,146/sqm. The city's appeal lies in its flat tax framework, low cost of living, and rapidly developing tech ecosystem supported by the Georgia Innovation and Technology Agency (GITA), which has assisted over 400 startups.

Batumi, the Black Sea coastal market, averaged $1,234/sqm in H1 2025. Gross rental yields average 7.28%, with some areas reaching 9.96%. Tourism and foreign investment drive this coastal market, where short-term rental demand remains strong.

Georgia's GDP grew 9.4% in 2024, with the IMF forecasting 5.2% growth for 2025. Foreign Direct Investment reached $1.68 billion in 2025. For American investors, the combination of unrestricted foreign ownership, USD purchasing power, and entry prices below $200,000 for quality stock makes Georgia accessible at the lower end of most investment ranges.

Mexico (Riviera Maya and Mexico City)

Mexico offers two distinct opportunities. Mexico City experienced a 39% surge in office net absorption in 2025 due to nearshoring, with the Central Business District capturing 62% of total transactions. Technology, IT, and financial sectors are driving this expansion, creating sustained corporate rental demand and long-term residential appreciation in executive housing markets.

The Riviera Maya corridor (Tulum, Playa del Carmen) captures a different wave: lifestyle migration and digital nomads. In 2025, 18.5 million Americans worked as digital nomads—a 153% increase since 2019. This demographic fuels mid-term rental demand in beach destinations with modern infrastructure.

In Quintana Roo, average prices reached $62,183 MXN per sqm (~$3,480 USD) in 2025. Short-term rental occupancy rates average 51% in Playa del Carmen and 39% in Tulum, generating gross rental yields from 8% to 15% annually.

Critical legal consideration: Foreigners purchasing property within 50km of the coast or 100km of the border must use a fideicomiso (bank trust). A Mexican bank holds legal title as trustee while the foreign buyer is the beneficiary with full rights to use, rent, sell, or inherit. The trust is valid for 50 years and renewable, with setup costs around $2,000-$3,000 USD and annual maintenance fees of $500-$575 USD.

Peso-denominated pricing favors USD buyers. With the exchange rate at 17.86 MXN per USD (April 2026), American investors capture currency arbitrage alongside property appreciation.

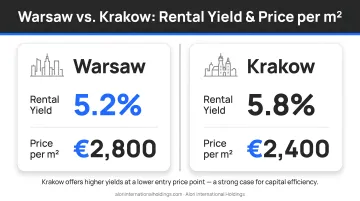

Poland (Warsaw and Kraków)

Poland's case starts with stability. NATO membership and a $5.5 billion investment to connect to the NATO Central Europe Pipeline System (CEPS) provide geopolitical anchoring that few Central European markets can match. The tech sector employs over 480,000 in business services, attracting multinational employers and driving internal migration toward Warsaw and Kraków.

In Q3 2025, Warsaw's secondary market prices averaged PLN 16,405/sqm, while Kraków averaged PLN 14,706/sqm. Gross rental yields averaged 5.92% nationally in Q1 2026, with Warsaw achieving 7.07% and Kraków 5.59%.

Poland's Build-to-Rent (PRS) sector is rapidly institutionalizing. Key indicators:

- Institutional PRS stock exceeded 25,000 units as of late 2025

- Projected to surpass 36,000 units by 2028

- Major operators like Resi4Rent and Vantage Rent are raising market standards and transparency

Poland's property prices per square meter remain well below Western European cities with comparable economic output. GDP is projected to grow 3.3% in 2025 and 3.5% in 2026—among the strongest growth forecasts within the EU—making the price gap harder to justify the longer it persists.

Vietnam (Da Nang and Ho Chi Minh City)

Vietnam's fundamentals are hard to ignore: a median age of 32.9, GDP growth of 7.52% in H1 2025, and one of Southeast Asia's fastest-expanding middle classes. Manufacturing and technology investment have accelerated as supply chains diversify away from China, with realized Foreign Direct Investment reaching $25.35 billion in 2024.

Foreign ownership operates under defined limits set by Vietnam's Housing Law No. 27/2023/QH15, effective January 1, 2025:

- Ownership duration: 50 years, renewable once for an additional 50 years

- Condominium cap: maximum 30% of units in any single building

- House cap: up to 250 independent houses per ward-level area

Market pricing:

Ho Chi Minh City average apartment prices surged to $4,057/sqm in Q4 2025, with gross rental yields ranging from 3.3% to 4.72%. Da Nang offers significant value at $2,000 to $3,500/sqm for beachfront condos—roughly half the cost of prime HCMC areas. Da Nang's resort-residential market attracts lifestyle investors, while HCMC's commercial core continues to attract corporate rental demand.

The ownership caps and leasehold structure require careful legal navigation, but Vietnam's combination of young demographics, 7%+ GDP growth, and sub-$3,500/sqm beachfront pricing makes it one of Asia's stronger risk-adjusted opportunities for the decade ahead.

What's Driving Capital Into Emerging International Markets

U.S. 30-year mortgage rates at 6.46% and median home prices at $400,500 have created a domestic affordability crisis. The price-to-income ratio hit 5.0, versus 4.1 pre-pandemic. American investors are bypassing domestic borrowing costs entirely, deploying cash reserves internationally where USD purchasing power, lower entry prices, and stronger yield spreads create compelling relative value.

Currency advantage matters: A strong USD versus many emerging market currencies means American buyers acquire hard assets at a relative discount. In April 2026, the USD traded at 1.15 against the EUR, 17.86 against the MXN, 3.64 against the PLN, and 2.68 against the Georgian Lari. Over the past three years, USD appreciation has amplified buying power across these markets.

That currency edge compounds with demographic momentum. Digital nomads, early retirees, and remote workers from high-cost countries are relocating to lower-cost, high-quality-of-life destinations — directly inflating rental demand in markets like Lisbon, Tbilisi, and Tulum ahead of price discovery. With 18.5 million American digital nomads now active, that demand shows no sign of retreating.

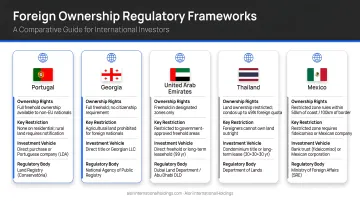

Regulatory arbitrage adds a third layer. Countries are competing for global capital by building favorable foreign investment frameworks, and the policy differences are significant:

- Portugal — fund-based Golden Visa alternative with EU residency pathway

- Georgia — unrestricted freehold ownership and 0% property tax

- Mexico — fideicomiso trust structure enabling foreign ownership in restricted zones

- Poland — institutionalizing private rental sector with growing legal protections

- Vietnam — 50-year renewable leaseholds open to foreign nationals

Investors who map these regulatory environments gain a structural advantage that goes beyond yield calculations.

How to Navigate Entry Into These Markets

The primary risk in emerging international markets is rarely the asset itself — it's the process. Title disputes, undisclosed liabilities, unfamiliar transaction customs, and regulatory frameworks that bear little resemblance to U.S. norms all create systemic exposure. Investors who enter without local legal and transactional support consistently overpay or inherit problems they didn't see coming.

A disciplined entry process covers three layers.

Market-Level Due Diligence

- Macroeconomic fundamentals (GDP growth, FDI flows, inflation)

- Demographic data (population trends, median age, migration patterns)

- Capital flow analysis (cross-border investment volumes, institutional activity)

- Regulatory stability assessment

Property-Level Due Diligence

- Legal title verification through local registries

- Valuation benchmarking against comparable sales

- Rental income modeling based on actual occupancy and average daily rate (ADR) data

- Developer track record and completion history for new developments

Exit Strategy — Before You Buy

- Resale liquidity assessment

- Long-term hold scenarios

- Rental yield sustainability across economic cycles

Having the framework matters. Having someone who can execute it in-market matters more.

Alori International Holdings works with American investors across this entire process — from market selection through legal structuring and closing. The firm combines global investment strategy with in-country execution, vetted legal structures, and off-market deal access. The goal is to make international markets genuinely navigable: clear entry points, verified assets, and defined exit paths built around long-term fundamentals rather than speculation.

Future Signals: What to Watch in 2027 and Beyond

Three signals typically mark the moment an emerging market tips into "recognized" status — and the window for outsized returns begins to close:

- Institutional capital inflows — private equity and REITs entering previously fragmented markets

- Mainstream media coverage of price growth, drawing broader retail investor attention

- Rapid new supply pipelines, as developers race to meet suddenly visible demand

These signals are already appearing in select markets. In Mexico, Park Life debuted as the country's first residential-only FIBRA (REIT), targeting housing demand driven by nearshoring. In Poland, the PRS sector drew EUR 108 million (~$118 million) in H2 2025 alone. Global cross-border commercial real estate investment finished 2025 up 25% year-over-year, with JLL projecting further acceleration through 2026 and 2027 as pension systems undergo structural reforms encouraging real asset exposure.

Technologies and data sources to monitor:

- Cross-border transaction data from JLL, CBRE, and Knight Frank

- Expat migration tracking platforms

- Central bank foreign direct investment reports

- Emerging market-specific real estate analytics tools

Tracking these sources over the next 12–18 months will clarify whether the following scenario plays out: if inflation in developed economies stays elevated and U.S. domestic affordability continues to deteriorate, demand from American buyers for international real estate will accelerate. In markets like Portugal and Georgia — still in early-recognition phases — 2026 and 2027 represent the period to establish positions before valuations adjust to reflect their structural fundamentals.

Conclusion

The strongest emerging real estate opportunities in 2026 sit outside domestic U.S. markets — in select international locations where regulatory frameworks, demographic momentum, and USD purchasing power converge into a credible long-term investment case.

Getting the timing right means doing the analytical work before the crowd arrives: reading demographic data, understanding local regulatory conditions, and committing capital with a multi-year horizon. Markets like Portugal and Georgia are at that inflection point now — fundamentals are measurable, entry pricing remains reasonable, and the structural drivers aren't going away.

For investors willing to move past familiar domestic options, 2026 offers a narrow window where the data is visible and the pricing hasn't fully caught up. That gap closes quickly once sentiment shifts.

Frequently Asked Questions

What is an emerging market in real estate?

An emerging real estate market is a geographic area where demand fundamentals—population growth, employment expansion, infrastructure investment—are building ahead of widely recognized price appreciation, giving early investors a window to enter before prices reflect full demand.

What are the top emerging real estate markets?

In 2026, the strongest emerging markets for international investors include Portugal, the Republic of Georgia, Mexico (Riviera Maya and CDMX), Poland, and Vietnam—each offering affordable entry, structural demand drivers, and favorable conditions for USD-holding buyers.

What are the emerging real estate trends?

Key 2026 trends include cross-border capital flows accelerating due to U.S. affordability constraints, demographic migration driving rental demand in lifestyle-friendly destinations, regulatory competition among countries for foreign investment capital, and currency advantages for USD buyers in emerging markets.

Which real estate investment is best for beginners?

For new investors, residential buy-and-hold properties in stable emerging markets offer the most accessible entry point. Look for markets with strong rental demand, clear legal frameworks for foreign ownership, and local expertise available to handle due diligence and legal structuring.

Is it safe to invest in international real estate as an American?

Investing internationally is viable for Americans when approached with proper due diligence. Key considerations include foreign ownership laws, title verification, tax treaty implications, and currency risk — all manageable with the right local legal and investment partners in place.

What are the risks of investing in emerging real estate markets?

Primary risks include:

- Market uncertainty if projected growth stalls

- Longer timelines requiring patience

- Regulatory or legal complexity for foreign buyers

- Currency fluctuation

These risks drop sharply with proper due diligence, local expertise, and clear exit strategies defined before purchase.