Yet here's the challenge: Europe comprises 44+ countries, each with distinct regulatory frameworks, tax regimes, and yield environments. Finding the right city requires more than a Google search—it demands data, local intelligence, and clear entry criteria. This guide presents a curated shortlist of the best European cities for property investment, explains the criteria used to select them, and shows American investors where to deploy $150K–$600K for rental income and long-term capital growth.

Key Takeaways

- Europe's residential real estate market is valued at $2.9 trillion in 2026, projected to reach $3.86 trillion by 2031—a CAGR of 5.88%

- Strong investment cities balance rental yield (ideally 5%+), price growth trajectory, and sound economic fundamentals

- Top markets: Lisbon, Barcelona, Warsaw, Riga, Tbilisi, and Bucharest

- Established markets like Lisbon and Barcelona offer stability; emerging ones like Riga, Warsaw, and Tbilisi deliver higher yields at greater risk

- For American investors: entry price, foreign ownership rules, tax treaties, and exit strategy are as critical as gross yield

Why European Cities Are Attracting Global Property Investors

International capital is returning to European residential real estate, driven by monetary easing and chronic housing shortages that protect asset values.

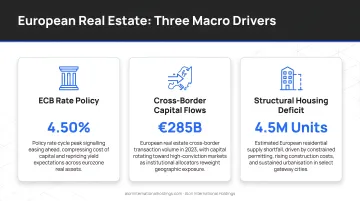

The ECB has entered a sustained rate-cutting cycle, lowering borrowing costs to 2.25% effective April 2025. That easing environment has revived cross-border investment, with capital flows to Europe rising 10% year-over-year to $21.63 billion in H2 2024. Underlying that demand: the European housing shortage has reached approximately 9.6 million homes—roughly 3.5% of current stock—and is expected to worsen as permit levels for new construction continue declining.

For US-based investors, the case goes beyond macro conditions. European property offers several advantages that domestic markets currently don't:

- Euro-denominated assets provide USD diversification when US valuations are stretched

- Rental yields in emerging Eastern European capitals frequently outpace comparable American markets

- Select countries offer residency or tax incentive programs, adding lifestyle value on top of financial returns

These fundamentals are being amplified by geopolitical change. The post-2022 reshuffling of European capital, Schengen expansion (Romania and Bulgaria achieved full membership in January 2025), and evolving EU membership trajectories are changing which markets attract the most institutional and individual investor attention.

What to Look for Before Investing in a European City

Not all European cities offer the same investment fundamentals. Five core criteria guided the selection of cities in this guide:

The Five Core Investment Criteria

- Gross rental yield: Annual rental income as a percentage of purchase price, indicating cash flow potential

- Average price per square meter: Entry cost that determines capital requirement and how accessible a market is to outside buyers

- Year-on-year price growth: Capital appreciation trajectory reflecting demand strength and market momentum

- Foreign ownership regulations: Legal restrictions (or lack thereof) on non-EU or non-resident buyers

- Tax environment: Property tax, rental income tax, and capital gains treatment that shape net returns

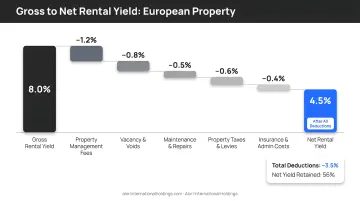

Gross vs. Net Rental Yield: The Math That Matters

High gross yields can be significantly eroded by local income tax, vacancy rates, management fees, and transaction costs. Net yields — what you actually earn — typically run 1.5% to 3% lower than the headline figure.

Gross rental yield is calculated as: (Median Monthly Rent × 12) ÷ Median Purchase Price × 100. Common deductions that close that gap include:

- Income tax on rental earnings (ranges from 5% flat in Georgia to 20%+ in Portugal)

- Property management and agency fees (typically 8–12% of rental income)

- Maintenance, repairs, and insurance premiums

- Vacancy periods (often 1–2 months annually in seasonal markets)

- Local property taxes (IMI in Portugal, IBI in Spain)

Example: A Lisbon apartment generating €1,500 monthly rent on a €300,000 purchase price shows a 6% gross yield. After 28% Portuguese income tax on rental income, 10% management fees, 0.4% IMI property tax, and one month of vacancy, net yield drops to approximately 3.2% — nearly half the headline figure.

Legal Structure and Exit Strategy: The Overlooked Essentials

Yield math only tells part of the story. Before committing capital, work through three structural checks that due diligence checklists frequently skip:

- Freehold ownership rights: Foreigners should be able to own the property outright — not just the unit, but the underlying land where relevant

- Rental income repatriation: No restrictions should exist on transferring earnings back to your home country; verify this before signing

- Resale market liquidity: A defined secondary market with documented transaction volume confirms you can exit when the time comes

Best European Cities for Property Investment

These cities were selected based on yield strength, price growth momentum, foreign investor accessibility, and structural demand drivers—not short-term speculation. Each entry covers entry pricing, gross rental yields, regulatory context, and the key variable that separates it from comparable markets.

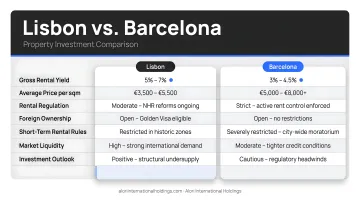

Lisbon, Portugal

Lisbon remains one of Europe's most internationally active property markets, benefiting from sustained price appreciation, strong demand from expats and digital nomads, and historically investor-friendly tax programs. The city combines Atlantic-facing climate, EU membership, English-language accessibility, and transparent legal processes for foreign buyers.

Average asking prices reached €6,082/sqm in March 2026, though median transaction prices registered lower at €1,951/sqm in Q1 2025, marking an 18.7% year-over-year increase. This divergence reflects the "expat premium"—foreign buyers in Greater Lisbon pay 61.9% more than domestic buyers on average.

Lisbon's rental fundamentals:

- Strong short- and long-term rental demand driven by tourism and tech sector growth

- EU legal framework with no foreign ownership restrictions

- Relatively transparent conveyancing process with established title registry systems

- English widely spoken in professional and service sectors

- Established resale market with high transaction volumes

Portugal's Non-Habitual Resident (NHR) tax program has been replaced by the more restrictive IFICI regime, which offers a 20% flat income tax rate but only for highly qualified professionals in research, innovation, and certified startups. Portugal's regulatory environment has grown more complex as a result — Alori International Holdings maintains in-market presence in Portugal specifically to help investors identify opportunities with vetted legal structures and defined exit strategies in this shifting landscape.

| Metric | Figure |

|---|---|

| Average Entry Price | €6,082/sqm (asking); €1,951/sqm (transaction) |

| Gross Rental Yield | 4.33% |

| Key Investor Advantage | EU membership, transparent legal process, strong international demand, residency pathways via investment funds |

Barcelona, Spain

Barcelona serves as Spain's second-largest economy and a global hub for tech, tourism, and international business. The city ranks among the top European cities for quality of life and maintains sustained appeal to foreign buyers despite tightening rental regulations.

Average asking prices reached €4,989/sqm at the end of Q3 2025, marking a 9.4% year-over-year increase. Gross rental yields average 7.17%, well above Portugal's compressed returns.

Barcelona's yield vs. regulation tradeoff:

- Mediterranean lifestyle premium with year-round demand

- Strong expat and student rental demand from multinational employers and international universities

- Spain's GDP growth projected at 2.9% in 2025, significantly outpacing the eurozone average

- Relatively competitive mortgage rates for foreign buyers through established Spanish banks

Critical regulatory context: Barcelona enforces strict rental regulations under Spain's 2023 Housing Law, imposing rent caps in "stressed residential areas" and limiting new contract rents to the previous rent plus a maximum 10% increase.

The city has also imposed a total moratorium on new tourist apartment licenses and plans to extinguish all 10,000 existing HUT licenses by November 2028. These restrictions eliminate short-term rental strategies but reinforce long-term rental demand.

| Metric | Figure |

|---|---|

| Average Entry Price | €4,989/sqm |

| Gross Rental Yield | 7.17% |

| Key Investor Advantage | Tourism-driven demand, economic growth above EU average, established expat rental market |

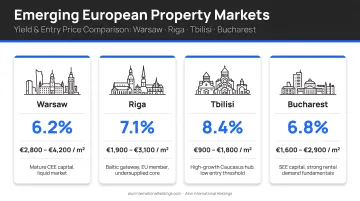

Warsaw, Poland

Warsaw has built a strong case as Central Europe's primary business and tech destination, with rental yields climbing faster than most EU capitals and transaction volumes up sharply over the past two years.

Average transaction prices for secondary market dwellings reached PLN 16,405/sqm (approximately $4,520) in Q3 2025, with gross rental yields averaging 6.81%. Poland's economy benefits from significant EU structural fund inflows and growing multinational corporate presence.

Why Warsaw appeals to yield-focused investors:

- Strong rental demand from growing young professional and expat populations

- Affordable entry prices compared to Western European capitals (roughly 25–40% lower per sqm than Lisbon or Barcelona)

- Rising property values driven by infrastructure investment and EU fund deployment

- Established legal framework with EU membership protections

Foreign ownership note: Non-EU citizens generally require a permit from the Ministry of Interior to acquire real estate in Poland, but there is a critical exemption—acquiring an "individual living accommodation" (standard apartment) does not require a permit. Land purchases do require authorization.

| Metric | Figure |

|---|---|

| Average Entry Price | ~$4,520/sqm (USD equivalent) |

| Gross Rental Yield | 6.81% |

| Key Investor Advantage | EU structural funds, tech sector growth, yield premium vs. Western Europe, no permit required for apartments |

Riga, Latvia

Riga delivers some of the highest gross rental yields in the EU at entry prices well below €1,000/sqm — a combination that few European markets can match.

Standard apartment transaction prices increased 1.77% year-over-year to €863/sqm in August 2025, while gross rental yields average 8.45%. Top-performing districts including Vecriga (Old Town) deliver yields up to 8.24% for well-positioned 3-bedroom apartments.

What makes Riga compelling:

- Low entry prices relative to yield (under $1,200/sqm)

- EU and Schengen membership providing legal stability and transparent ownership frameworks

- Growing tourism and business travel demand driven by Baltic economic resilience

- No significant restrictions on foreign property ownership for apartments

Foreign ownership framework: Non-EU citizens cannot acquire land property in Latvia, but there are no legal restrictions on purchasing apartments, making urban residential investment fully accessible to international buyers.

| Metric | Figure |

|---|---|

| Average Entry Price | €863/sqm |

| Gross Rental Yield | 8.45% |

| Key Investor Advantage | EU legal framework, low entry cost, top-district yield premium, Schengen access |

Tbilisi, Georgia

Tbilisi represents an emerging European-adjacent market attracting growing international investor attention, particularly from American buyers seeking USD-denominated entry points and a flat 5% tax on rental income.

Transaction prices varied by district in Q1 2025, with Vake averaging $2,146/sqm (+20.8% year-over-year) and Saburtalo at $1,568/sqm (+12.0% YoY). City-wide gross rental yields average 7.78%.

Tbilisi's unique appeal for American investors:

- USD-friendly pricing with transactions commonly denominated in dollars

- Flat 5% tax on residential rental income with no deductions (compared to 20%+ in Western Europe)

- No annual property tax for foreign owners on properties not generating rental income

- Strong short-term rental demand driven by tourism and digital nomad migration

- Straightforward freehold ownership structure with no restrictions on foreign buyers for residential property

- Digital property registration enabling ownership transfer within 24 hours

Georgia's property investment threshold of $100,000+ qualifies foreign buyers for permanent residency, creating a dual value proposition for lifestyle migration and investment. Alori's local expertise and in-market presence in Georgia provide vetted deal access in a market where local intelligence significantly impacts outcomes.

| Metric | Figure |

|---|---|

| Average Entry Price | $1,568–$2,146/sqm (district-dependent) |

| Gross Rental Yield | 7.78% |

| Key Investor Advantage | Flat 5% rental income tax, 0% property tax, no foreign ownership restrictions, USD-denominated pricing, residency pathway |

Bucharest, Romania

Bucharest recorded 16.6% year-over-year asking price growth through December 2025, driven in part by Romania's full Schengen accession in January 2025 and sustained demand from multinational employers entering the market.

Asking prices averaged €2,204/sqm in December 2025, up 16.6% year-over-year, while gross rental yields range from 6.39% for studios to 6.70% for three-room apartments.

The investment case:

- Among the lowest property prices per sqm among EU capitals (roughly 60% below Western European equivalents)

- Rising demand from a growing middle class and inflowing multinational employers

- FDI stock reached €118.2 billion at end-2023, funding ongoing infrastructure improvements

- EU membership providing legal protections comparable to other eurozone markets despite lower price points

- Full Schengen membership as of January 2025, eliminating internal border controls and enhancing business connectivity

Foreign ownership note: Non-EU citizens cannot own land directly in Romania but can utilize a "superficies right" (controlling land for up to 99 years) or form a local company to own buildings on land.

| Metric | Figure |

|---|---|

| Average Entry Price | €2,204/sqm |

| Gross Rental Yield | 6.39–6.70% |

| Key Investor Advantage | EU membership, full Schengen access, low acquisition cost relative to EU peers, strong price growth momentum |

How We Identified These Cities

Each city was assessed against the same framework disciplined institutional investors use for market selection:

- Gross rental yield and price-to-income ratios

- Year-on-year price growth trends

- Foreign ownership accessibility and legal clarity

- Tax burden on rental income

- Structural demand indicators: tourism volume, tech sector presence, and demographic growth

The most common investor mistake is prioritizing gross yield headlines without accounting for total transaction costs, local income tax on rent, vacancy rates, and the absence of a verified exit market. A 7% gross yield can quietly become 3% net after costs in a high-tax jurisdiction. In Portugal, for example, buyers face a planned 7.5% IMT (Property Transfer Tax) on secondary homes starting in 2026, plus 0.8% Stamp Duty — nearly 8.3% in upfront costs before any renovation or furnishing.

This list excludes markets with speculative price growth, unclear legal structures for foreign buyers, or limited exit liquidity. The focus is on long-term capital preservation over short-term arbitrage — the same standard applied to every market Alori International Holdings evaluates.

Conclusion

The best European city for property investment depends on your capital range, risk tolerance, income goals, and timeline. Established markets like Lisbon and Barcelona offer stability, legal clarity, and consistent demand—though yields are compressed by foreign buyer premiums. Emerging markets like Riga, Warsaw, and Tbilisi offer stronger yield upside and lower entry costs, but require more hands-on due diligence and regulatory navigation.

Go beyond surface-level yield comparisons. Before committing capital, evaluate:

- Total cost of ownership — transaction fees, holding costs, and currency exposure

- Legal structure — how title is held and what protections exist for foreign buyers

- Tax exposure — local property taxes, rental income treatment, and capital gains on exit

- Exit strategy — liquidity depth and realistic buyer pool in your target market

Local expertise—not just market data—is often what separates a successful cross-border investment from a costly one.

For investors focused on Portugal and Georgia, Alori International Holdings sources opportunities based on verified legal structures, macroeconomic fundamentals, and defined exit strategies—connecting global capital with in-country professionals who know how transactions actually close.

Frequently Asked Questions

Where is the best place to invest in real estate in Europe?

The top-performing cities by yield and price growth include Riga (8.45% yield), Warsaw (6.81% yield with EU fund support), Tbilisi (7.78% yield with 5% flat tax), and Barcelona (7.17% yield with strong economic growth). "Best" depends on your capital budget ($100K–$600K range), risk profile, and whether you prioritize income generation or capital appreciation.

Is there a European equivalent to Zillow?

No single pan-European platform matches Zillow's scope. The most widely used regional portals include Idealista for Spain and Portugal, Immoweb for Belgium, Rightmove for the UK, Otodom for Poland, and Storia.ro for Romania. For cross-border investors, local agents or curated platforms remain the most reliable way to navigate this fragmentation.

Can Americans buy property in Europe without restrictions?

Most European countries allow foreign nationals to purchase property freehold, though some require specific permits for certain land types such as agricultural land in Poland. Non-EU buyers should verify ownership rules, tax treaty implications, and FATCA reporting requirements with a qualified cross-border tax advisor before purchasing.

What rental yields can investors realistically expect in European cities?

Gross yields range from 5–8%+ in emerging markets like Riga, Warsaw, and Tbilisi to 4–6% in established markets like Lisbon and Barcelona. Net yields after costs and vacancy typically run 1.5–3% lower—making the local tax environment a critical variable in total return calculations.

How much capital do I need to start investing in European real estate?

Entry prices range from under $100,000 in markets like Tbilisi and Bucharest to $300,000+ in Lisbon or Barcelona. The $150,000–$600,000 range covers a solid selection of opportunities across both established and emerging European markets.

What are the biggest risks of investing in European property?

Key risk categories include currency fluctuation (EUR/USD volatility), regulatory changes (rental caps, short-term let restrictions as seen in Barcelona), political or legal uncertainty in non-EU markets, and illiquidity risk in markets with shallow resale demand. Proper due diligence and in-country legal representation mitigate most avoidable risks.