Introduction

Europe's luxury residential real estate market is splitting in two — and the dividing line is reshaping where capital flows.

Trophy assets above €10 million are seeing price corrections in capitals like London and Paris. At the same time, mid-tier luxury properties in emerging cities are posting consistent appreciation. This divergence isn't temporary volatility. It reflects deeper structural shifts: intergenerational wealth transfer, lifestyle migration, and tightening regulatory frameworks that are redrawing the map of where high-net-worth buyers want to be.

For American investors seeking European exposure, this matters. Allocating capital to a prestigious address no longer guarantees returns. Geographic selectivity, disciplined entry pricing, and local market intelligence now determine outcomes — and the gap between investors who understand this and those who don't is widening.

Key Takeaways

- The European luxury residential market is projected to expand from $129 billion in 2024 to over $183 billion by 2033, though performance varies sharply by segment and location

- Ultra-luxury properties (above €10M) face price cuts and longer sales timelines in London and Paris; mid-range markets in Lisbon, Madrid, and Porto remain resilient

- Demand for space, wellness amenities, and remote-work capability is redirecting capital from trophy addresses to lifestyle-driven markets

- Branded residences carry a 38% price premium in Europe (vs. 33% globally), with the pipeline projected to expand 113% by 2032

- EU energy regulations are creating a measurable green premium for certified properties — and a discount for those that fall short

The Bifurcated Market: Trophy Asset Declines vs. Mid-Tier Resilience

The European luxury market no longer moves as a single asset class. Instead, 2025 data reveals a sharp divide: ultra-luxury properties priced above €10 million in established capitals are experiencing volume declines and price adjustments, while properties in the €300,000–€2 million range across growing European cities demonstrate relative resilience or growth.

The Top-End Correction

Transaction volumes at the ultra-luxury tier have contracted significantly. Prime London and Paris postcodes show extended time-on-market figures, with properties lingering 30–40% longer than historical norms. Price reductions have become standard negotiating tools rather than exceptions, particularly for properties lacking modern amenities or sustainability credentials.

This correction stems from ultra-high-net-worth buyer caution driven by geopolitical uncertainty, evolving tax frameworks (including UK non-dom reforms), and rising interest rates that reduced buyer leverage through 2023–2024. These buyers are pausing rather than panic-selling, but the result is a frozen top tier where pricing expectations between sellers and buyers remain misaligned.

Mid-Tier Resilience

The picture is different one tier down. Professionals, entrepreneurs, and families buying in the €300,000–€2 million range are driven by concrete goals — second homes, retirement properties, remote work bases — rather than speculative positioning. They're choosing cities with proven infrastructure and clear legal frameworks.

Several markets are absorbing this demand consistently:

- Lisbon's Chiado and Príncipe Real districts — restored heritage buildings with strong expat infrastructure

- Porto's Ribeira waterfront — competitive pricing relative to Western European capitals

- Madrid's expanding luxury neighborhoods — high-end apartments with improving amenities and international appeal

These buyers prioritize quality of life and long-term utility, which makes their demand more resilient to rate cycles and geopolitical noise.

Investment Implication: The correction in trophy assets does not reflect the entire European luxury market. Mid-tier luxury in high-conviction markets continues to offer solid underlying demand, while selective entry opportunities may emerge at the top end as sellers adjust asking prices and rates normalize.

Emerging European Luxury Markets Challenging Established Hubs

The definition of a European luxury destination is expanding beyond London, Paris, and Monaco. Cities and regions previously considered secondary—Lisbon, Porto, Madrid, Dubrovnik, Budapest—have experienced accelerating HNWI interest, branded development activity, and double-digit price growth over recent years.

Lisbon's Ascent

Lisbon captures this trend. According to Knight Frank's Prime Global Cities Index, Lisbon has posted consistent annual price growth, with neighborhoods like Chiado and Príncipe Real attracting international buyers seeking heritage properties, modern apartments, and lifestyle positioning at €4,000–€7,000 per square meter—significantly below Paris's top-tier arrondissements, where ultra-prime developments exceed €60,000–€70,000 per square meter.

Portugal's EU regulatory frameworks, historically favorable residency programs, and lifestyle quality continue drawing global capital. Strong tourism underpins rental demand, with the Algarve averaging 300+ days of sunshine annually.

American investor interest remains strong despite 2023 reforms removing real estate from Golden Visa eligibility. Forty percent of high-net-worth Americans plan to purchase property abroad within the next year, with Portugal consistently ranking as a primary destination.

Why Emerging Markets Are Gaining Traction

Several structural factors support this shift:

- EU frameworks offer clear legal processes for foreign ownership and title registration

- Sustained international visitor growth supports short-term rental yields of 5–10% annually in cities like Lisbon and Porto

- Climate, safety, and lower cost of living attract remote workers and lifestyle migrants at scale

- Entry prices in the $150,000–$600,000 range create buyer pools that established hubs simply can't match

Investment Implication: Emerging markets offer stronger ROI potential but require deeper local due diligence on legal frameworks, title clarity, and exit strategies. Alori International Holdings focuses specifically on markets like Portugal, pairing macroeconomic analysis with in-country professionals who understand local regulations, transaction processes, and realistic exit timelines.

Post-Pandemic Lifestyle Priorities Reshaping Buyer Demand

The pandemic permanently shifted luxury buyer preferences. Space, privacy, wellness amenities, outdoor areas, and home-office capability are no longer premium features—they're baseline expectations. This evolution has expanded the definition of a desirable luxury property beyond city-center prestige addresses.

Remote Work Unlocks Secondary Markets

Remote work flexibility has enabled affluent buyers—especially internationally mobile professionals—to consider resort areas and secondary cities they previously would have used only for vacation properties. Coastal and alpine markets are now year-round residential destinations rather than seasonal retreats.

Demand growth is visible across locations like the Algarve, Costa del Sol, and Alpine resort communities. These markets support full-time or extended residence through:

- Established tourism infrastructure with year-round services

- Quality healthcare accessible to international residents

- Reliable internet infrastructure suited to remote professionals

- Lifestyle amenities that rival major urban centers

Properties offering private pools, landscaped gardens, and outdoor entertaining space command clear premiums over comparable urban apartments lacking these features.

The traditional hierarchy placing urban centers above resort destinations is shifting. Buyers now evaluate properties on functional utility—can this support my lifestyle year-round?—as much as on address prestige.

Branded Residences and Generational Wealth Transfer Driving New Demand

Two interconnected trends are reshaping demand: the explosive growth of branded residences and the intergenerational wealth transfer from Baby Boomers to Gen X and Millennials.

The Branded Residence Premium

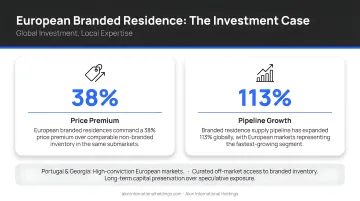

Branded residences—properties developed in partnership with luxury hotel groups—are commanding significant price premiums over non-branded equivalents. According to Savills, Europe's average brand premium has surged to 38%, outpacing the global average of 33%. In established cities, branded schemes achieve premiums of approximately 30%, while resort markets see 39% premiums.

Paris offers the most dramatic example. Historically deemed "the impossible city" for branded developments due to heritage restrictions, Paris is finally seeing its first true branded scheme: the Maybourne Residences Saint-Germain, priced at €60,000 to €70,000 per square meter. In London, The Whiteley (Six Senses) has achieved £3,650 per square foot, with developers attributing as much as 20% of that premium directly to the brand affiliation.

The European pipeline is set for rapid expansion: from 141 completed schemes at the end of 2025 to over 300 by 2032—a 113% increase.

Generational Wealth Transfer

A major intergenerational wealth transfer is reshaping the buyer pool across European luxury markets. This incoming generation is less tied to traditional prestige addresses and more motivated by:

- Design quality and architectural distinctiveness

- Wellness integration (spas, fitness, air quality standards)

- Sustainability credentials and energy efficiency

- Flexibility in use — part-time residence, rental potential, or eventual resale

Younger HNWIs want hotel-grade services and verifiable ESG standards, not just a prestigious postcode. That's precisely why branded residences are outperforming conventional luxury stock — and why their European pipeline is expanding so aggressively.

Sustainability and Smart Technology Becoming Luxury Market Differentiators

A "green premium versus brown discount" divide is emerging in European luxury real estate. Properties with high energy ratings and sustainable certifications are commanding price premiums, while energy-inefficient properties face devaluation. The EU's Energy Performance of Buildings Directive (EPBD) acts as a compliance mechanism, with implementation deadlines that require property upgrades or disclosure of poor efficiency.

Smart-home technology, health-oriented design, and eco-conscious construction have become baseline expectations among luxury buyers, particularly younger high-net-worth individuals (HNWIs). Developers are responding across several categories:

- Integrated smart-home platforms with centralized controls

- Wellness amenities including air filtration, circadian lighting, and fitness facilities

- Green certifications (BREEAM, LEED, EU Energy Class A) that support long-term asset value

- Sustainable materials and low-carbon construction methods

Market Effect: Properties lacking these features face growing difficulty achieving premium pricing, while certified sustainable properties increasingly justify higher valuations.

What's Driving These European Luxury Real Estate Trends

Five structural forces — not short-term market cycles — are shaping European luxury real estate demand, and each one reinforces the others.

Global Wealth Growth and Rising HNWI Population

The global HNWI population is projected to expand significantly over the next five years, particularly from Asia (Taiwan, India) and the Middle East. This sustained wealth expansion creates durable demand for European luxury property as a store of value and lifestyle asset. European real estate offers currency diversification, political stability, and lifestyle utility that appeal to globally mobile wealth holders.

Foreign Buyer Demand and Cross-Border Capital Flows

Asian, Middle Eastern, and North American investors view European luxury real estate as a stable, inflation-resistant asset class offering both capital growth and lifestyle benefits. Several factors are amplifying this demand:

- Exchange rate dynamics that favor dollar- and dirham-denominated buyers in euro-priced markets

- Residency programs such as Portugal's historically favorable Golden Visa frameworks

- Investment-friendly regulations in select jurisdictions that reduce transaction friction

For American investors, navigating these markets requires both macroeconomic context and in-country execution. Firms like Alori International Holdings specialize in exactly this — combining global investment strategy with local market expertise to help investors access European opportunities with clarity and reduced transaction risk.

Supply Constraints in Prime Locations

Planning restrictions, heritage preservation laws, and land scarcity in established luxury districts create a structural supply ceiling that supports valuations regardless of broader economic conditions. In protected heritage zones like Lisbon's historic center or Paris's Haussmann boulevards, new supply is essentially impossible — which means renovated existing stock holds long-term value that new construction simply cannot dilute.

Regulatory and Tax Environment Evolution

Shifting wealth tax policies, non-dom tax changes (such as the UK's 2025 reforms), and varying capital gains frameworks across European jurisdictions are influencing where international buyers direct capital. Investors increasingly prioritize markets with stable, transparent, and investor-friendly legal structures.

Interest Rate Normalization and Buyer Recalibration

The rising interest rate environment of 2023–2024 reduced buyer leverage and confidence, creating the current pause at the top of the market. As rates normalize, pent-up demand and recalibrated pricing could create meaningful entry conditions for disciplined investors.

How These Trends Are Impacting Buyers and Investors

Operational Impact on Investment Strategy

Investors can no longer treat European luxury real estate as a monolithic asset class. Outcomes now hinge on three factors:

- Geographic selectivity — not every prime market offers the same demand fundamentals

- Entry price discipline — overpaying in a tightening market compounds risk on exit

- Local regulatory knowledge — tax structures, ownership rules, and residency programs vary sharply by country

Buying into prestige addresses without structural demand analysis carries real downside, particularly as capital flow patterns across European cities continue to diverge.

Business Impact for the Market

The same shift is reshaping how developers, agents, and platforms operate. Developers are prioritizing branded residences, wellness amenities, and sustainability credentials over legacy prestige-address positioning. Emerging city markets — previously overlooked in favor of Paris, London, or Zurich — are attracting serious attention as buyers seek value alongside lifestyle fit.

Traditional marketing built on address alone is giving way to narrative-driven pitches centered on tangible lifestyle benefits.

Future Signals: What to Watch in Europe's Luxury Residential Market

The trends identified today are early indicators of structural shifts that will define the market over the next one to three years. Investors who act on them early will have a measurable advantage.

Emerging Market Maturation

Portugal, Spain's secondary cities, and Croatia are moving from "emerging" to "established" luxury designations. Projected price appreciation trajectories suggest the window to enter at relative value may narrow as institutional recognition increases. For investors focused on structural demand over momentum-driven exposure, this shift marks a critical entry window — one that closes as institutional capital follows.

Regulatory and Tax Landscape Shifts

Ongoing EU-level building efficiency regulations (EPBD implementation deadlines), potential changes to golden visa and residency investment program rules, and country-specific wealth tax adjustments will redirect capital flows within Europe. Investors should track regulatory changes in target markets as closely as property fundamentals.

Demographic Demand Surge

Two converging wealth trends will drive outsized demand across European luxury markets through 2025–2028. Millennial and Gen X investors are inheriting Baby Boomer wealth at scale, while Asian HNWI populations continue expanding their European footprint.

The properties drawing the most attention share three characteristics:

- Sustainability credentials — energy efficiency ratings and green certifications

- Lifestyle integration — proximity to cultural, culinary, and outdoor amenities

- Experience value — design quality and location distinctiveness over pure square footage

Conclusion

Europe's luxury residential real estate market is neither in uniform decline nor uniform growth. It is bifurcating by market tier and geography, rewarding investors with the selectivity and local intelligence to separate structural opportunity from speculative exposure.

The six trends covered in this analysis — market bifurcation, emerging market ascent, lifestyle-driven demand, branded residence growth, sustainability premiums, and the generational wealth transfer — share a common thread:

- Each reflects a shift in where value is concentrating, not just that value exists

- Each rewards investors who act on fundamentals rather than momentum

- Each is already in motion, not projected for some future cycle

The correction in ultra-luxury trophy assets does not signal broader market weakness. It reflects a repricing of outdated assumptions — and a clear signal about where the next cycle of appreciation is building. Firms like Alori International Holdings, which combine data-driven market selection with in-country execution, are positioned to identify exactly these kinds of structural shifts before they become consensus.

Frequently Asked Questions

Which European country is best for real estate investment?

Portugal and Spain consistently rank as strong performers for international investors due to legal transparency, lifestyle appeal, and sustained price growth. The best choice depends on your goals—yield, capital growth, or lifestyle. Portugal stands out for its residency programs and strong tourism demand, which supports 5–10% annual rental yields.

Is European luxury real estate a good investment in 2025 and beyond?

The market is growing at a projected CAGR of approximately 3.93% through 2033, though performance varies sharply by segment and location. Mid-tier luxury in emerging cities offers solid fundamentals, while ultra-luxury assets in prime capitals are correcting — potentially creating entry opportunities for patient investors.

How have interest rates and economic conditions affected European luxury property prices?

Rising interest rates reduced buyer leverage and extended transaction timelines in 2024–2025, particularly at the ultra-luxury tier. However, locations with limited supply and genuine demand have held their value and may see a rebound as rates ease over the next 12–24 months.

What is driving demand from international and American investors for European luxury real estate?

European property offers dollar-based investors a combination of inflation resistance, currency diversification, and long-term capital growth that's harder to replicate domestically. Favorable exchange rates, selective residency programs, and transparent legal frameworks make the case even stronger for investors looking beyond US markets.

Are branded residences worth the premium in the European luxury market?

Branded residences command price premiums averaging 38% over comparable non-branded properties in Europe and are outperforming the broader luxury market in transaction volume. They appeal particularly to younger HNWI buyers who prioritize hotel-grade services and hands-off ownership — and typically generate rental yields of 7–12% annually.

What are the biggest risks of investing in European luxury real estate as a foreign buyer?

The primary challenges are regulatory complexity (shifting tax laws, foreign ownership rules, AML compliance), title clarity in emerging markets, and currency risk. Working with advisors who understand local legal structures and have genuine in-country experience reduces these risks substantially.