Introduction

For high-net-worth individuals, real estate has shifted from a status symbol into a core wealth preservation tool. Three pressures are driving this move:

- Domestic saturation in prime U.S. markets, compressing yields and limiting entry points

- Persistent inflation eroding the real value of cash and fixed-income holdings

- Equity volatility exposing concentrated portfolios to sharp, rapid drawdowns

As a result, many HNWIs are reallocating toward tangible assets that offer capital stability across cycles.

The real challenge for HNW investors is knowing which strategies hold up at this level. Too many rely on momentum or lifestyle appeal when selecting markets. Durable positioning requires evaluating markets on macro and demographic fundamentals, sizing allocations against actual liquidity needs, and understanding the legal and tax implications of cross-border ownership.

This guide covers the "why" behind real estate as an HNW wealth tool, the key strategies in practice today, how to evaluate markets rigorously using macroeconomic and demographic indicators, and how to think about allocation and risk in a way that aligns with your liquidity needs and time horizon.

Key Takeaways

- Real estate offers inflation protection, portfolio diversification, and capital preservation that liquid assets cannot replicate.

- Effective HNW strategies include prime location direct ownership, international diversification, income-generating rentals, and legacy asset planning.

- Sound market selection relies on macroeconomic data, structural demand, regulatory stability, and in-country expertise—not price momentum.

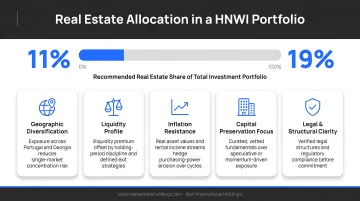

- Allocation depends on liquidity needs, time horizon, and risk profile—HNWIs typically allocate 11–19% of portfolios to real estate.

- Risk management requires accounting for liquidity constraints, legal complexity in foreign markets, and portfolio concentration.

Why Real Estate Remains a Core Wealth Preservation Tool for HNWIs

Real estate functions as a safe haven precisely because it is not correlated to daily market sentiment. Unlike stocks or bonds, physical property operates independently of investor mood swings and algorithmic trading patterns. During periods of uncertainty, prime-location properties have historically maintained or appreciated in value. Global HNWIs maintain a 19% portfolio allocation to real estate as of 2024, reflecting its enduring role as a wealth preservation anchor.

The inflation hedge case for real estate is straightforward: as construction costs, land values, and rental rates rise with inflation, property ownership protects purchasing power in ways that cash and fixed-income instruments cannot. With 5% inflation, the real value of debt can fall by roughly 40% within ten years, creating a structural advantage for leveraged real estate investors. Academic analysis using data from 1990 to 2023 across six countries demonstrates that real estate provides an effective hedge against inflation in the long run, both in crisis and non-crisis periods.

Real estate also delivers a dual-benefit structure unique among asset classes. It generates returns through appreciation and rental income while remaining a tangible, usable asset — one that can be occupied, enjoyed, and leveraged for personal use while simultaneously compounding wealth. Equities and commodities offer no equivalent. That combination of financial return and real utility is what keeps real estate central to serious long-term portfolios.

HNWIs are shifting away from domestic "trophy ZIP codes" toward international markets that offer comparable quality at significantly lower entry prices. European and emerging markets now provide access points well below U.S. equivalents, often with more favorable regulatory frameworks and stronger demographic demand drivers:

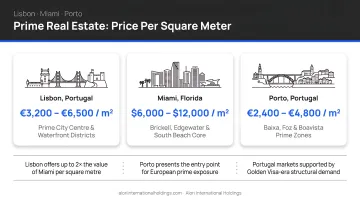

- Lisbon (€13,600/m²) and Miami (€13,400/m²) have reached near price parity, making Lisbon a structurally compelling alternative

- Porto offers a steep discount at €3,940/m², with growing demand from digital nomads and international buyers

- Emerging markets with improving legal infrastructure are attracting capital that previously defaulted to gateway U.S. cities

The data points toward a reallocation — not just a trend, but a structural repricing of where intelligent capital belongs.

Identifying those markets requires more than price comparison. The most sophisticated HNW investors target high-conviction markets — where structural demand, regulatory stability, and demographic fundamentals align for durable long-term performance. They are not chasing trend-driven geographies; they are identifying markets where supply constraints, capital flows, and population dynamics create sustained appreciation potential. 44% of global family offices plan to increase their real estate allocations, signaling institutional confidence in real estate's continued role as a core holding.

Key Strategies HNW Investors Use in Real Estate

Prime Location Direct Ownership

Acquiring property in established, supply-constrained locations—major urban centers, waterfront areas, historically significant districts—remains the bedrock strategy for HNW investors. Scarcity of supply combined with consistent demand creates long-term price resilience. Competition and acquisition costs are higher in these markets, but so is downside protection.

Prime locations carry structural advantages that secondary markets can't replicate:

- Limited land availability prevents oversupply from eroding values

- Infrastructure investment concentrates in established districts

- Demand holds across economic cycles, not just bull markets

- Risk-adjusted returns tend to outperform over full investment cycles

Entry costs are elevated, but that premium buys durability.

International Geographic Diversification

Holding real estate across multiple countries or regions reduces dependence on the economic cycle of a single market. Currency diversification can work in an investor's favor over a long hold period, particularly when U.S. dollar strength fluctuates relative to emerging and European currencies. Certain international markets offer legally favorable entry conditions—residency programs, flat tax regimes, low transaction friction—that amplify returns.

Firms like Alori International Holdings are specifically structured to connect HNW American investors with curated opportunities in selective international markets such as Portugal and Georgia. Rather than speculative market exposure, these platforms offer vetted legal structures, verified developer partnerships, and defined exit strategies. Tbilisi, Georgia, offers gross rental yields averaging 7.42%, outperforming Western European capitals.

Rental Income Generation

High-demand rental markets—particularly undersupplied urban cores or tourist-heavy international destinations—can generate consistent passive income that improves overall portfolio yield. Short-term vacation rental and long-term lease strategies have different risk profiles, occupancy dynamics, and regulatory considerations that must be evaluated before acquisition.

Markets with strong tourism fundamentals or expat populations tend to support higher rental yields. However, regulatory environments vary significantly: some cities impose strict short-term rental licensing requirements, while others maintain more flexible frameworks. Understanding these micro-level regulations is essential to income stability.

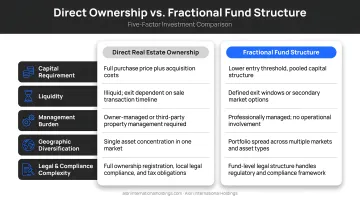

Direct Ownership vs. Fractional and Pooled Structures

Direct ownership provides full control, full cost burden, and personal use capability. Fractional or fund-based structures offer lower entry capital, professional management, and reduced personal involvement—but with limited personal use and decision authority.

| Factor | Direct Ownership | Fractional / Fund |

|---|---|---|

| Entry capital | Higher | Lower |

| Control | Full | Limited |

| Personal use | Yes | Typically no |

| Management burden | High | Minimal |

| Liquidity | Lower | Varies by structure |

Tax, estate planning, and operational implications differ substantially between structures — professional guidance is essential before committing capital.

Legacy and Multi-Generational Asset Planning

Luxury and heritage properties held across generations function both as appreciating assets and family legacy vehicles. Properties with architectural significance, historical provenance, or cultural relevance tend to have lower market turnover and stronger long-term price stability, which makes them well-suited as core holdings in a generational wealth transfer plan.

These assets often appreciate independently of broader market cycles due to their unique characteristics and limited supply. They also provide intangible family continuity benefits that transcend financial returns — combining financial appreciation with the kind of shared ownership that binds family wealth across generations.

Value-Add vs. Turnkey Acquisition

The turnkey approach offers immediate occupancy, higher price premium, and lower operational complexity. Value-add acquisitions provide lower entry prices, renovation upside, and higher hands-on management requirements.

Choosing between them comes down to three factors: time horizon, operational bandwidth, and local market conditions. Oversupplied markets favor value-add — there's room to buy below replacement cost and capture renovation upside. In tight markets, turnkey may be the only viable entry point. Investors without renovation infrastructure typically find the premium for turnkey worth paying.

How to Evaluate and Select the Right Market

Macroeconomic screening serves as the first filter. HNW investors should assess a target market's GDP trajectory, employment base, foreign direct investment flows, and inflation environment before evaluating individual assets. These factors determine whether structural demand will persist across a full investment cycle — or simply reflect short-term momentum. Georgia exhibited 9.7% GDP growth in 2024 compared to Portugal's 2.1%, illustrating the wide variance between developed and emerging markets.

Demographic analysis provides the second layer. Population growth, urbanization trends, age distribution, and migration patterns reveal whether long-term rental demand and buyer appetite are increasing or contracting. Markets with rising urbanization, young median age, and positive net migration tend to support durable demand rather than speculative influx.

Legal and regulatory due diligence can make or break returns. Foreign ownership rights, transaction costs, capital repatriation rules, property taxation, and exit mechanics all vary significantly across international markets — and getting any of them wrong is expensive. Working with in-market legal professionals is essential, not optional. Portugal's Golden Visa program officially removed direct real estate acquisition as a qualifying route in October 2023, a regulatory shift that reshaped the market's residency appeal entirely.

Local market intelligence goes beyond data. Macro indicators show what a market is doing broadly, but in-country professionals understand what a spreadsheet can't: neighborhood dynamics, off-market deal flow, developer credibility, and cultural nuances around negotiation. Investors with fewer markets and deeper understanding consistently outperform those with shallow exposure across many.

Exit strategy must be defined before entry. A clear understanding of the likely buyer pool, projected liquidity timeline, and whether rental income covers carry costs during the hold period is essential. Investors who enter without this clarity often face forced sales at unfavorable times, eroding returns even when underlying fundamentals are sound.

Each of these filters maps to a distinct phase of evaluation:

- Macroeconomic screening — GDP trajectory, FDI flows, employment base, inflation

- Demographic analysis — urbanization rate, median age, net migration trends

- Legal due diligence — ownership rights, transaction costs, repatriation rules, tax exposure

- Local intelligence — neighborhood dynamics, off-market access, developer track record

- Exit planning — buyer pool depth, liquidity timeline, carry cost coverage

Managing Risk in High-Net-Worth Real Estate Portfolios

Real estate at scale carries risks that go well beyond market timing. Understanding where each risk originates — and how to size your exposure accordingly — is what separates resilient portfolios from ones that underperform under pressure.

Liquidity Risk

Liquidity risk is the most underestimated factor in HNW real estate. Unlike equities, property cannot be sold in hours — transaction timelines of 3 to 12 months are common. Investors without adequate liquid reserves elsewhere may find themselves in distressed sale situations.

Size real estate positions relative to your overall liquidity buffer, not just total net worth.

International Risk

Cross-border investments introduce their own risk layer. Currency fluctuations can erode returns even when property appreciates in local terms. Legal systems vary significantly across jurisdictions, and geopolitical shifts can alter regulatory frameworks or tax treatment with little warning.

Working with established local partners and vetted legal structures reduces exposure — though no structure eliminates risk entirely.

Key international risk factors:

- Currency volatility reducing USD-equivalent returns

- Legal system differences in contract enforcement and property rights

- Regulatory changes affecting taxation, rental rules, or ownership structures

- Geopolitical events impacting market stability and capital flows

Concentration Risk

Concentration risk is easy to overlook when a portfolio spans multiple properties. Owning several assets in the same city, sector, or economic zone creates the feeling of diversification — not the substance of it.

Genuine diversification means exposure across geographies, asset classes, and distinct demand drivers. Selective entry into two or three high-conviction markets consistently outperforms spreading capital thinly across speculative ones.

Portfolio Allocation Frameworks: How Much Real Estate Is Right?

Common portfolio allocation frameworks discussed among HNW investors and wealth advisors provide useful starting points. The Warren Buffett 70/30 rule is frequently cited, though primary sources from 1957 show Buffett was referring to a 70% allocation to general equities and 30% to corporate "work-outs" (mergers/liquidations), not real estate. The 8-4-3 rule is a mutual fund SIP heuristic illustrating that wealth accumulates steadily for 8 years, doubles in the next 4, and grows exponentially in the final 3. The 3-3-3 rule in real estate is a consumer readiness guideline for homebuyers, not an institutional framework.

Authoritative wealth reports from Capgemini, UBS, and Goldman Sachs place average HNWI and family office allocations between 11% and 19% globally as of 2024/2025. So what percentage is right for a given portfolio? That depends on several interconnected factors:

- Liquidity needs — how much capital must remain accessible on short notice

- Time horizon — whether capital is earmarked for 5, 10, or 20+ years

- Income requirements — whether the portfolio needs current yield or prioritizes appreciation

- Property quality and diversification — concentrated single-asset exposure carries different risk than a spread across markets and asset types

Once those factors are mapped, the sizing decision becomes more straightforward. Real estate should be matched against long-horizon capital — money that won't be needed in the near term, since property cannot be liquidated quickly when markets seize up.

Every increase in real estate exposure deserves a stress test against a forced-sale scenario. The goal is a real estate allocation large enough to provide stability and inflation protection, but not so large it creates a liquidity crisis when other assets are also under pressure.

Frequently Asked Questions

What are the 3-3-3, 8-4-3, and Warren Buffett 70/30 rules for wealth creation and portfolio allocation?

These are three separate heuristics, not a unified framework. Buffett's 70/30 referred to his 1957 equity/work-out split, not real estate. The 8-4-3 rule describes mutual fund compounding acceleration over time. The 3-3-3 rule is a homebuyer checklist (3 months savings, 3-year stay, compare 3 homes) — none apply directly to institutional portfolio construction.

How much of a high-net-worth portfolio should be allocated to real estate?

Institutional data from Capgemini, UBS, and Goldman Sachs shows HNWIs and family offices allocate 11-19% to real estate globally. The right allocation depends on your overall liquidity, risk tolerance, and investment horizon rather than a universal rule.

What are the biggest risks of high-net-worth real estate investment?

The top three risks are illiquidity (3-12 month sale timelines — keep at least 6 months of liquid reserves elsewhere), market concentration (owning multiple properties in the same city or sector is not true diversification), and for international holdings, legal and currency complexity. Each requires deliberate structuring before you commit capital, not after.

Is international real estate a good investment for American HNWIs?

For American HNWIs, international real estate offers genuine diversification, inflation protection, and entry into markets with stronger demographic demand at lower price points than comparable U.S. assets. Success comes down to market selection and working with local experts who know the legal and transactional terrain — not just the property itself.

What is the difference between direct ownership and fractional real estate investing for HNWIs?

Direct ownership provides full control, personal use, and direct asset appreciation but requires full capital deployment and hands-on management responsibility. Fractional structures lower entry capital, offer professional management, and reduce operational burden — but limit personal use and decision authority.

How do I know if a real estate market is worth investing in?

Key criteria include macroeconomic stability (GDP growth, FDI flows), demographic demand drivers (population growth, urbanization), legal clarity for foreign investors, structural supply constraints, and a defined exit pathway. If you cannot answer how and to whom you will eventually sell, the market is not ready — regardless of what the growth projections say.