True diversification in real estate goes well beyond buying more properties. It requires intentional decisions about asset types, geographies, investment structures, and risk balance—considerations that most investors overlook. This guide explains how to build a resilient real estate portfolio that performs across economic cycles.

Key Takeaways

- Diversification means spreading across property types, locations, risk profiles, and investment vehicles—not just owning more of the same type

- The most resilient portfolios combine residential, commercial, and alternative property types alongside both active and passive investment structures

- Geographic diversification—including international markets—cuts exposure to any single local economy and improves risk-adjusted returns

- Common mistakes include over-concentrating in one asset class, skipping periodic rebalancing, and choosing high-volatility sectors without understanding their risk profiles

- Define clear goals, track asset correlation, and rebalance regularly—that's what separates a deliberate portfolio from a random property collection

How to Diversify Your Real Estate Investment Portfolio

Step 1: Define Your Investment Goals and Risk Tolerance

Diversification strategy is not one-size-fits-all. Investors targeting passive income need a different mix than those seeking appreciation or capital preservation.

Your time horizon, liquidity needs, and acceptable drawdown levels should drive how aggressively you diversify across riskier versus stable asset types. A 35-year-old with steady employment income can afford higher exposure to development projects and emerging markets.

A retiree needing consistent monthly income should emphasize stable, cash-flowing properties with long-term tenants — a fundamentally different allocation.

Key considerations:

- Income vs. appreciation: Multifamily and commercial properties typically deliver steady income; development and value-add plays target appreciation

- Time horizon: Longer timelines allow for illiquid investments like direct ownership or private equity funds

- Liquidity needs: Maintain enough liquid holdings to avoid forced sales during downturns

- Acceptable volatility: Higher-risk sectors like hospitality can amplify returns but require tolerance for significant drawdowns

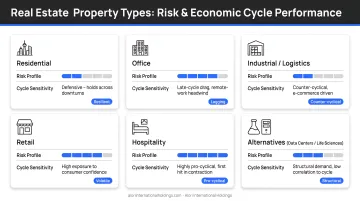

Step 2: Diversify Across Property Types

Different property types perform differently across economic cycles, so mixing them reduces correlation and smooths income streams. Relying on a single asset class leaves you vulnerable to sector-specific disruptions.

Core property types to consider:

- Multifamily: Residential apartments show resilience during downturns as housing demand stays relatively stable

- Industrial/Logistics: E-commerce growth has driven sustained demand for warehouse and distribution space

- Self-storage: Recession-resistant with low operating costs and flexible lease terms

- Medical office: Aging demographics and healthcare demand provide structural support

- Retail: Higher volatility due to e-commerce disruption, but well-located properties with strong tenants remain viable

- Hospitality: Highest volatility; performance closely tied to economic cycles and discretionary travel spending

During the 2008 financial crisis, hospitality properties saw occupancy and revenue plummet, while multifamily and industrial assets showed relative resilience. In 2020, industrial and self-storage sectors outperformed as pandemic-driven behavioral shifts accelerated e-commerce adoption and space utilization needs.

Nested diversification adds another layer of risk management. Within multifamily, you can split exposure between Class A luxury properties and Class B workforce housing, or between short-term vacation rentals and long-term residential leases. Each carries different risk-return profiles.

Step 3: Diversify Across Geographies—Including International Markets

Geographic diversification protects against local economic downturns, regulatory changes, and market saturation. A portfolio concentrated in one city or region can suffer when that market softens due to job losses, natural disasters, or policy shifts.

Domestic Geographic Diversification

Spreading across three domestic tiers reduces exposure to any single regional economy:

- Sun Belt growth markets (Texas, Florida, Arizona) — population-driven demand and business relocation tailwinds

- Established Northeast metros (New York, Boston) — financial and institutional capital density

- Midwest affordability markets (Indianapolis, Columbus) — lower entry costs with stable employment bases

Each region runs on different economic drivers — energy, finance, manufacturing — and cycles at different times.

International Diversification

Adding non-correlated global markets can further improve risk-adjusted returns. KKR research shows that US real estate equity and credit delivered high absolute returns over the last decade, but adding assets from Asia and Europe resulted in better returns per unit of risk. CBRE Investment Management found that while 22 US cities have an average correlation of 0.87 with each other, the correlation drops to 0.50 when compared with 65 non-US cities.

Investors seeking international exposure should target markets with structural demand drivers, sound regulatory frameworks, and accessible entry points. Firms like Alori International Holdings specialize in identifying high-conviction international markets—such as Portugal and Georgia—through data-driven analysis and local in-market expertise. This reduces the research burden and transaction risk for individual investors, offering curated opportunities with verified legal structures and defined exit strategies in the $100,000–$600,000 range.

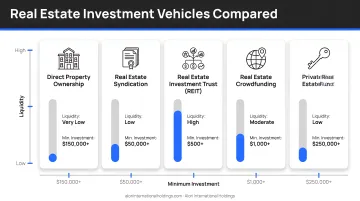

Step 4: Mix Active and Passive Investment Vehicles

Investment structures differ significantly in liquidity, control, minimum investment, and hands-on involvement. Diversifying across structures lets you balance control with capital efficiency.

Investment vehicle comparison:

- Direct property ownership: Maximum control and potential tax benefits, but requires significant capital, hands-on management, and concentrates risk in fewer assets

- REITs (Real Estate Investment Trusts): High liquidity, low minimums, instant diversification across properties, but no control and higher correlation to stock markets

- Real estate crowdfunding platforms: Accessible minimums ($500–$25,000), passive management, but limited liquidity and higher fee structures

- Delaware Statutory Trusts (DSTs): Allow 1031 exchange deferral and passive income, but illiquid with 5–10 year hold periods

- Private equity real estate funds: Institutional-quality diversification with professional management, but high minimums ($50,000–$250,000+) and limited liquidity

Passive vehicles allow investors to achieve diversification across more properties and markets with lower capital minimums. J.P. Morgan Asset Management research suggests that a blend tilted toward private real estate with approximately 20-40% allocated to REITs provides optimal risk-adjusted returns, with REITs offering tactical flexibility and liquidity.

Step 5: Monitor Performance and Rebalance Periodically

Diversification is not a one-time setup. Market movements, property performance changes, and shifts in personal goals require periodic review and rebalancing.

A standard benchmark: review allocation annually and rebalance when any single asset class drifts more than 5–10% from its target weight. When one property type significantly outperforms, it creates unintended concentration — you may be less diversified than you think.

Rebalancing strategies:

- Sell outperforming assets and reinvest in underweighted categories

- Direct new capital to underrepresented property types or geographies

- Use cash flow from mature properties to acquire assets in target sectors

When Does Real Estate Portfolio Diversification Matter Most?

Diversification matters most when economic conditions shift — rising interest rates, local market downturns, or a portfolio already concentrated in one market, property type, or tenant category. These are the moments when spread determines whether a portfolio weathers the cycle or takes a direct hit.

Critical diversification scenarios:

- Single-market concentration — Investors holding only residential properties in one city face amplified risk from local job losses or regulatory changes

- Single-tenant dependence — Relying on one tenant or lease for the majority of rental income creates catastrophic risk if that tenant defaults

- Approaching retirement — Income stability becomes more important than growth, which means shifting toward cash-flowing, lower-volatility assets before the transition — not after

- Scaling up — A $150,000 single-property position and a $1.5M portfolio with zero spread carry the same structural vulnerability; the stakes just get higher

Key Variables That Shape Your Diversification Outcomes

Correlation Between Assets

True diversification requires assets that don't move in sync. Owning multiple properties in the same market or the same property type does not achieve meaningful diversification even if the asset count is high.

Correlation measures how closely two assets move together. The scale works like this:

- 1.0 — Assets move identically; no diversification benefit

- 0.0 — No relationship; meaningful risk reduction

- -1.0 — Assets move in opposite directions; maximum diversification

The lower the correlation between portfolio assets, the more effective your diversification.

Owning five residential rental properties in the same metropolitan area is concentration with more properties, not diversification. They all face the same local economic conditions, regulatory environment, and demand drivers.

Entry Timing and Market Cycles

Markets in different regions or countries may be at different stages of their real estate cycle. A globally diversified investor can capture opportunities unavailable in a single market.

When US coastal markets are peaking with high valuations, Sun Belt markets may be in mid-cycle growth, while certain international markets could be in early recovery. This cycle dispersion lets you buy into growth early rather than chasing prices at their peak — a meaningful edge for long-term capital allocation.

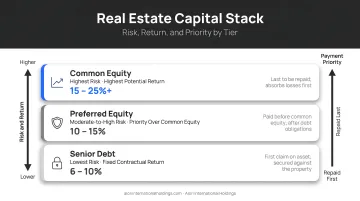

Capital Stack Position

Diversification can also apply to where in the capital structure you participate. Equity ownership, preferred equity, and debt positions each carry distinct risk and return profiles worth understanding before you allocate.

- Equity ownership — Highest upside potential but first to absorb losses

- Preferred equity — Fixed return with priority over common equity, moderate risk

- Debt positions — Lowest risk, priority claim on cash flows and assets, but capped returns

Mixing these positions strengthens portfolio resilience — during downturns, equity values may fall while debt holders keep receiving payments, stabilizing overall returns.

Liquidity Profile of the Portfolio

Some real estate investments offer more accessible liquidity (REITs, crowdfunding), while others are illiquid over longer hold periods (direct ownership, DSTs).

Ensure your portfolio has enough liquidity to meet near-term needs without forcing untimely exits. A portfolio composed entirely of illiquid direct holdings may force you to sell at unfavorable prices when liquidity matters most.

Common Mistakes When Diversifying a Real Estate Portfolio

Over-Concentrating in a Single Market or Asset Class

Owning five residential rental properties in the same metropolitan area is not diversification—it's concentration with more properties. True diversification requires assets with different performance drivers.

Even if you own properties in different neighborhoods, they all face the same local economy, employment market, and regulatory environment. A regional recession affects all five simultaneously.

Chasing High-Yield Sectors Without Understanding Cyclical Risk

Hotel properties, senior care facilities, and oil-and-gas-adjacent real estate have historically underperformed during recessions and carry elevated operational and regulatory risk.

The historical record is clear on this:

- Hospitality properties saw occupancy drops and revenue declines of 50–70% during both the 2008 financial crisis and the 2020 pandemic

- Senior housing facilities carry complex regulatory requirements that can erode returns faster than most investors anticipate

- Oil-and-gas-adjacent assets are highly sensitive to commodity cycles largely outside an investor's control

High yields exist for a reason—they compensate for higher risk. Understand the volatility profile before allocating significant portfolio weight to these sectors.

Neglecting Rebalancing After Strong Performance Periods

When one property type or geography outperforms, it can cause the overall portfolio to drift toward unintended concentration.

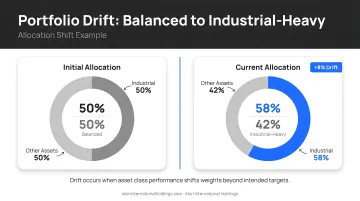

If industrial properties appreciate 40% while retail properties remain flat, your originally balanced 50/50 allocation becomes 58/42 industrial-heavy. This drift means you're taking more industrial exposure than intended, increasing concentration risk.

A practical rule: review your allocation ratios annually, or whenever a single sector moves more than 10–15% relative to the rest of the portfolio. Catching drift early is far cheaper than correcting it after a downturn.

Should International Real Estate Be Part of Your Portfolio?

Markets outside the US operate on different economic cycles, regulatory environments, and supply-demand dynamics. KKR's research demonstrates that adding broad exposure to real estate diversified by region historically reduced portfolio volatility, allowing investors to achieve the same returns for lower levels of risk. CBRE Investment Management modeling shows that increasing real assets allocation to 25-30% (including global listed and private real estate) provides left tail-risk mitigation, reducing adverse 10-year returns from -1.4% to -0.2%.

Key considerations before entering international markets:

- Macroeconomic indicators — GDP growth, inflation trends, employment rates, infrastructure development

- Demographic trends — Population growth, urbanization rates, aging demographics, tourism patterns

- Capital flow patterns — Foreign direct investment trends, expat migration, international buyer activity

- Regulatory frameworks — Foreign ownership laws, property rights protections, tax treatment, residency pathways

- Local transaction processes — Title verification standards, escrow procedures, legal documentation requirements

- Currency dynamics — Exchange rate volatility, hedging options, long-term convergence patterns

Accurately evaluating all of these factors is where most individual investors run into trouble. The primary barrier to international diversification isn't access to capital — it's access to reliable local knowledge. Misjudging any one of these variables can increase risk rather than reduce it.

That's where genuine in-country expertise makes the difference. Alori International Holdings takes a selective, data-driven approach to identifying high-conviction international markets, offering vetted projects, verified legal structures, and defined exit strategies for investors in the $100,000–$600,000 range. The firm focuses on two complementary markets: Portugal, an established European market with strong lifestyle and rental fundamentals, and Georgia, a frontier market offering compelling value and structural growth potential.

Conclusion

A truly diversified real estate portfolio requires deliberate decisions across property types, geographies, investment vehicles, and risk profiles—not just owning more properties. The most common failure in real estate diversification is mistaking quantity for spread.

Sustaining that protection over time comes down to three habits:

- Rebalance periodically — strong performance in one sector quietly rebuilds the concentration you worked to eliminate

- Monitor across geographies — domestic and international market cycles rarely move in sync, which is precisely the point

- Stay disciplined at entry — diversification erodes fastest when investors chase momentum rather than fundamentals

For investors looking beyond domestic markets, international real estate — particularly in structurally undersupplied markets like Portugal and Georgia — offers a distinct layer of diversification that domestic holdings alone cannot replicate. The goal isn't more properties. It's the right exposure across the right markets, maintained with intention.

Frequently Asked Questions

How to diversify a real estate portfolio?

Diversification means spreading investments across different property types (residential, commercial, industrial), geographic markets, and investment structures — direct ownership, REITs, and passive vehicles. The goal is ensuring no single market or asset class drives your entire portfolio's performance.

What property types are best for a diversified real estate portfolio?

Multifamily, industrial/logistics, self-storage, and medical properties have held up well across past downturns, while hospitality and senior housing carry higher volatility. The right mix depends on your income goals and how much short-term variability you can absorb.

How much of my investment portfolio should be in real estate?

Allocation varies by investor profile, but institutional recommendations commonly suggest 10–20% for balanced portfolios. Real estate's low correlation to stocks and bonds makes it an effective hedge regardless of exact allocation.

What are the biggest risks of an undiversified real estate portfolio?

Concentration in one market or property type leaves investors exposed to local downturns, sector disruptions, and income gaps. When one position struggles, a diversified portfolio has other assets to absorb the impact — a single-market portfolio does not.

Is international real estate a good way to diversify?

Yes — international markets often move through different economic cycles than domestic ones, which can reduce overall portfolio volatility. That said, navigating foreign legal structures, transaction processes, and currency exposure requires genuine in-country expertise, not just remote research.

When should I rebalance my real estate portfolio?

Most financial advisors recommend an annual portfolio review, with rebalancing triggered when any asset class drifts 5–10% from its target allocation. This prevents unintended concentration from strong performance in one sector.